Options trading provides opportunities in a diverse spectrum of strategies, including aggressive speculative position-taking to low volatility income. Among them, the box spread strategy is a peculiar strategy that can be called a mechanical one since it is commonly known as the arbitrage or synthetic loan strategy.

As opposed to more common strategies, including covered calls or straddles, the box spread is not about the market direction. Rather, it is concerned with the development of a risk-free (or close to risk-free) payoff via calls together with puts.

This blog will go in-depth on what a box spread strategy is, how it works, the types of box spreads, why traders use them, the risks and limitations, and their comparisons to other option strategies. This advanced options strategy will be broken down for you, including both the theoretical underpinnings and the real-world applications.

What Is a Box Spread?

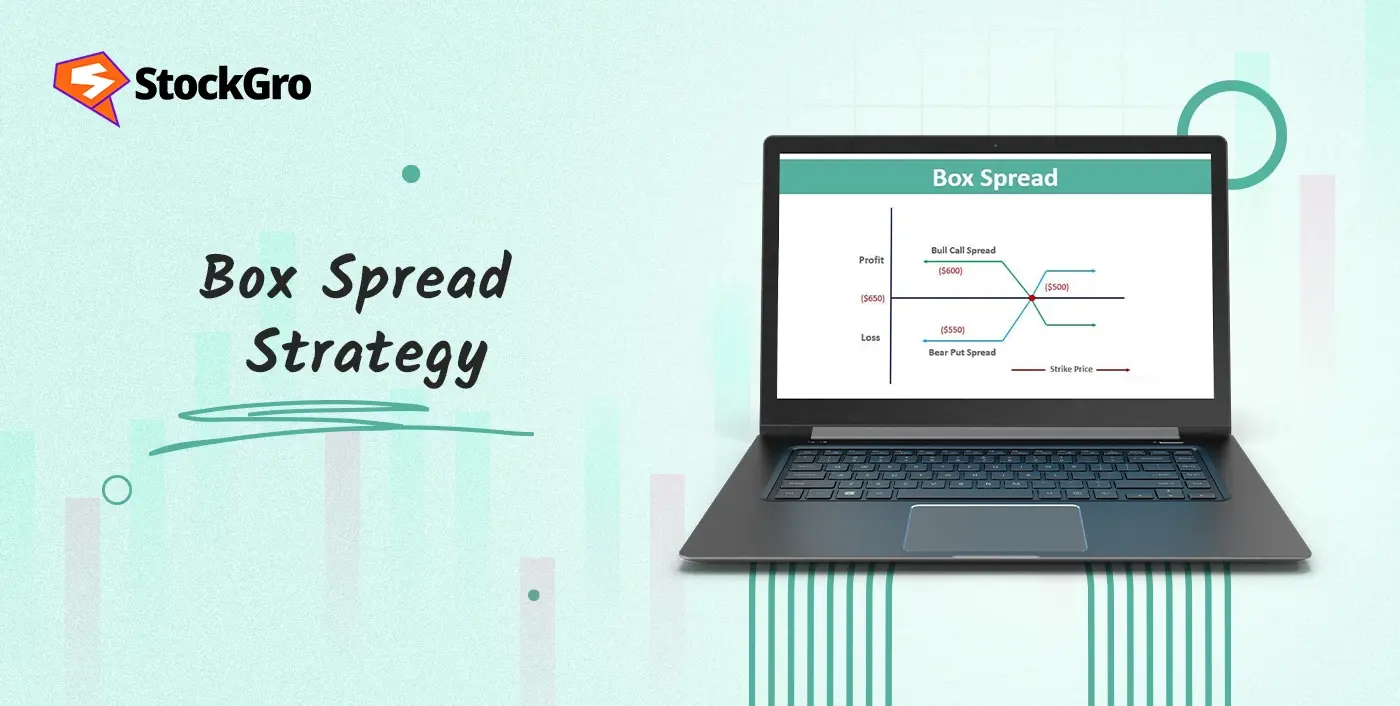

A box spread is an options strategy combining a bull call spread and a bear put spread with the same strikes and expiry to lock in a fixed, risk-free payoff. The outcome is a position which is risk-free at expiry and effectively resembles a fixed-income.

Traders have spoken of it converting options into a synthetic bond. When done in the right way, the payoff is known in advance regardless of the movement of the underlying asset. The only flexibility is the cost to put together the spread when compared to a certain payoff at expiry in options trading.

In essence:

- A long box strategy behaves like lending money (you pay upfront and receive a higher payoff later).

- A short box arbitrage behaves like borrowing money (you receive cash upfront but pay it back at expiration).

The main point is that the options pricing must incorporate interest rates and value of money. Box spreads can take advantage of mispricings.

How a Box Spread Works (Mechanics)

To understand how a box spread strategy works, let’s break it down step by step:

- Bull Call Spread – The bull call spread strategy involves purchasing a call at a lower strike price and then selling a call at a higher strike price. It will result in a payoff in case the underlying increases but is limited to the disparity between the 2 strikes.

- Bear Put Spread – The bear put spread is the practice of purchasing a put at a higher strike, and selling a put at a lower strike. It gives a payoff only in the event that the underlying falls, as well as capping.

- Combining the Two – Combining both of these spreads together based on the same strikes and expiration date, and the result is a fixed payoff equal to the difference between your strikes, irrespective of whether the market rises, falls, or remains sideways.

Suppose an underlying stock is trading at ₹1,000.

A call option with a strike price of ₹1,000 is purchased by you, and a call option with a strike price of ₹1,100 is sold to you.

Simultaneously, you purchase a put option with a strike price of ₹1,100 and sell another put option with a strike price of ₹1,000.

At expiry, there will always be a net payoff of ₹100 (the difference between ₹1,100 and ₹1,000). The actual profit or cost of the trade depends on the premium you pay or receive at the time of entering the strategy. This premium decides whether you are effectively lending money to the market or borrowing from it.

Types of Box Spreads: Long vs. Short Box

There are two main variations of the strategy:

1. Long Box Spread

- Made when you pay for the position in advance.

- At expiration in a long box strategy, you receive a fixed payout equal to the strike difference.

- Since you put money in now and get your money back later, it’s not unlike lending money to the market.

- Profit arises if the total cost of setting up the spread is less than the guaranteed payoff.

2. Short Box Spread

- Created when you receive money upfront by entering the position.

- At expiration in short box arbitrage, you must pay the fixed difference between strike prices.

- This is similar to borrowing money from the market.

- It’s used when the options are overpriced compared to fair value, allowing traders to collect more upfront than they eventually repay.

Why Use a Box Spread? (Use Cases & Benefits)

Traders and institutions use box spreads mainly for arbitrage, financing, and hedging purposes rather than speculation.

- Arbitrage Opportunities

- When box spread options prices deviate from fair value, box spreads can lock in a risk-free profit.

- This is rare in highly liquid markets but can happen in less efficient ones.

- When box spread options prices deviate from fair value, box spreads can lock in a risk-free profit.

- Synthetic Financing

- A long box spread strategy functions like lending money; a short box spread functions like borrowing.

- Traders can replicate loans or investments without involving traditional financing instruments.

- A long box spread strategy functions like lending money; a short box spread functions like borrowing.

- Low-Risk Strategy

- Unlike directional strategies, box spreads don’t depend on whether the market goes up or down.

- The payoff is predetermined, making it a low-volatility play.

- Unlike directional strategies, box spreads don’t depend on whether the market goes up or down.

- Institutional Use

- Hedge funds, market makers, and arbitrage desks use box spreads to exploit pricing inefficiencies and manage capital efficiently.

- Hedge funds, market makers, and arbitrage desks use box spreads to exploit pricing inefficiencies and manage capital efficiently.

Example: Real-World Box Spread Setup

After recovering from its recent lows under 600 rupees, Jubilant Foodworks (JUBLFOOD) is now trading at approximately 646 rupees on the stock chart. For instance, in order to establish a box spread, a trader may purchase a call option at ₹600 and sell it at ₹650, a bull call spread; at the same time, they could purchase a put option at ₹650 and sell it at ₹600, a bear put spread. This technique guarantees a payout of ₹50 (the difference between 650 and 600) at expiry, independent of the price movement on the chart.

The profit or loss is solely determined by the amount of premium paid or received when the trade was initiated. While the chart’s background is useful for pinpointing strike levels near recent support and resistance, the box spread is more of a low-risk arbitrage tool than a directional bet.

Risks & Limitations

Although box spreads appear to be “risk-free,” in reality, there are several risks and limitations:

- Transaction Costs

- You can lose all or almost all of your arbitrage earnings due to commissions and bid-ask spreads.

- Liquidity Risk

- If the options on an underlying asset are illiquid, entering and exiting at fair prices can be difficult.

- If the options on an underlying asset are illiquid, entering and exiting at fair prices can be difficult.

- Execution Risk

- Box spreads involve multiple legs. Delays or slippage during execution can impact profitability.

- Box spreads involve multiple legs. Delays or slippage during execution can impact profitability.

- Counterparty/Settlement Risk

- In rare cases, settlement or counterparty issues can affect payouts.

- In rare cases, settlement or counterparty issues can affect payouts.

- Regulatory Oversight

- Some exchanges and regulators limit the use of box spreads because they effectively replicate loans, raising compliance concerns.

- Some exchanges and regulators limit the use of box spreads because they effectively replicate loans, raising compliance concerns.

- Low Returns

- In efficient markets, arbitrage opportunities are minimal. Efforts may not be worthwhile if the returns are insufficient to cover costs.

Box Spread vs Other Options Strategies

To put box spreads into context, let’s compare them with some commonly used options strategies:

- Versus Covered Call

- Covered calls generate income but expose the trader to downside risk on the stock.

- A box spread strategy has no market-direction risk, only pricing efficiency risk.

- Covered calls generate income but expose the trader to downside risk on the stock.

- Versus Straddle/Strangle

- Straddles bet on volatility. Box spreads ignore volatility – their outcome is fixed.

- Straddles bet on volatility. Box spreads ignore volatility – their outcome is fixed.

- Versus Iron Condor

- Iron condors profit from low volatility but still have directional risk.

- Box spreads provide certainty of payoff.

- Iron condors profit from low volatility but still have directional risk.

- Versus Calendar Spread

- Calendar spreads rely on time decay differences. Box spreads lock in arbitrage unrelated to volatility or time decay.

- Calendar spreads rely on time decay differences. Box spreads lock in arbitrage unrelated to volatility or time decay.

Simply put, when most options strategies are concerned with a view on volatility, direction, or time decay, the box spread is an exception due to its focus on pricing efficiency and synthetic financing.

Conclusion

Box spread is an interesting tool of options application, not as a speculative idea, but as an arbitrage tool and synthetic lending or borrowing. By using the identical strikes and expiration for a bear put spread and a bull call spread, traders can secure a set payout that is directly proportional to the difference in strike prices.

Theoretically, it provides risk-free profits, but practically, factors such as transaction costs, liquidity, and risks of execution limit its widespread application. Institutions and sophisticated traders can use it to take advantage of inefficiencies or in managing financing, but retail traders will generally have limited opportunities and tiny returns.

FAQs

Generally, spreads of the box type are low-profit strategies. Institutional traders frequently use them to close an arbitrage lens and trade due to mis-pricing between option contracts. As they become an arrangement that constructs a riskless payoff position, the profit is generally the difference between the price that a trader pays in establishing a spread position and the risk-free interest rate gain. Although the amount of profits is small, they remain steady in large amounts, with low transaction costs.

A box spread is not identical to an iron condor, but both involve multiple option contracts. An iron condor is a strategy that makes a profit when volatility is low, as the iron condor trader hopes the underlying price naturally stays within a particular range. By comparison, box spread is an arbitrage idea that pays a predetermined amount whether the price rises or drops. The iron condor will depend on time decay and volatility, whereas the box spread will depend on mispricing or interest rate opportunity.

Spreads based upon options trades are sometimes called risk-free arbitrage; however, in practice, that is not exactly true. Although the payoff is fixed hypothetically, the risk factors that traders have to deal with include the risks of execution, liquidity, and trading costs, which reduce the profit possibility. Also, assignment risk or the early exercise occurs in the case of American-style options, and this can affect the strategy. Although payoff is predetermined, practically, box spreads cannot be labeled as risk-free in a real-life trading scenario, but only have low directional risk.

To put on a box spread, a trader will combine a bull call spread with a bear put spread in options with the same strike price and expiration date. An example is to purchase a call with a lower strike price and sell a call with the higher strike (bull call spread). At the same time, purchase the put at the deep in-the-money strike, and sell the put at the deep in-the-money strike (bear put spread). These combined form a fixed position in the box spread.

A box spread is the reverse of an arbitrage position, or standing exposed to market risk. Other traders find a simple naked options strategy (such as selling naked calls or puts) to be the antithesis, since a box spread is risk-free, whereas a naked options position has risk on the unlimited side. In structure, they have no real negative counterpart, with such strategies as speculative directional bets or naked options being the opposites.