While investing in a mutual fund, you have to make a decision whether to invest in a lump sum or do an SIP. Most people think mutual funds are SIPs, but they’re not. Especially, when you try to redeem or check your returns.

In basic terms, one defines what you are investing in, while the other defines the frequency and manner of investing. Think of a mutual fund as a restaurant and SIP as your monthly meal subscription. You can walk into the restaurant anytime and order a big meal at once, or you can subscribe to a monthly plan that delivers smaller portions regularly. The food is the same — the eating style is different.

Mutual Fund

A mutual fund is a shared pool of investor money managed by a professional fund manager. When you invest in a mutual fund, your money goes into a basket of stocks, bonds, or other securities, depending on the type of fund you choose.

For example, if you invest ₹1,00,000 in HDFC Mid-Cap Fund, your money gets spread across mid-sized market capitalization companies such as Max Financial Services, AU Small Finance Bank, Indian bank and others. You do not need to select individual stocks yourself, as the fund manager manages those investment decisions.

You can invest in a mutual fund in two broad ways — as a lump sum (putting in a large amount at once) or as an SIP (putting in smaller amounts at regular intervals). The mutual fund itself is the product. How you put money into it is a decision determined by your income, savings, and goals.

SIP

As noted earlier, SIP, or Systematic Investment Plan, is a method of investing in mutual funds, not a product in itself. It allows you to invest a fixed amount at regular intervals, usually monthly, though some funds also offer weekly or quarterly options.

Thus, when someone says, ‘I have a SIP of ₹5,000 in Axis Bluechip Fund’, what they mean is: every month, ₹5,000 is automatically deducted from their bank account and invested into that fund.

SIPs became popular in India because they make investing accessible, especially for salaried professionals. You do not need a large amount up front. You can start with as little as ₹100 per month on some platforms.

A SIP draws much of its strength from two forces: rupee cost averaging and compounding. By putting in the same sum at set intervals, you tend to accumulate more units during weaker phases and fewer when valuations climb. Over a period, this can help moderate your overall entry cost.

Check with SIP Calculator for your future investment plan

Mutual Fund vs SIP – What is the Difference Between Mutual Fund and SIP

Now that we understand what each one is, let us compare them across the factors that actually matter when you are deciding how to invest.

| Parameter | Mutual Fund | SIP |

| What it is | An investment vehicle that pools money from multiple investors | A method of investing in mutual funds regularly |

| Investment type | One-time lump sum or regular | Regular, fixed-interval investments only |

| Minimum amount | ₹500 to ₹5,000 (lump sum) | As low as ₹100 to ₹500 per month |

| Market timing | Requires careful timing for lump sum | Averages out market fluctuations (rupee cost averaging) |

| Risk level | Higher if invested at market peak | Lower due to spread across market cycles |

| Flexibility | Can invest any time in any amount | Fixed date and fixed amount each period |

| Suited for | Investors with large capital ready to deploy | Salaried individuals, first-time investors |

| Returns | Can be higher if timed correctly | Moderate, consistent over long term |

| Volatility impact | Full exposure at the point of investment | Reduces impact through staggered buying |

| Example | Invest ₹1,00,000 in Mirae Asset Emerging Bluechip Fund at once | Invest ₹5,000/month for 20 months in Axis Bluechip Fund via SIP. Thus, your commitment will be deducted each month |

Investment Method vs. Investment Vehicle

This is the most fundamental difference that most people miss. A mutual fund is an investment vehicle — it is the product you are investing in. A SIP is an investment method — it is the mechanism through which you invest in that product.

You cannot invest in a SIP without a mutual fund. But you can invest in a mutual fund without a SIP. A SIP always leads to a mutual fund, not the other way around.

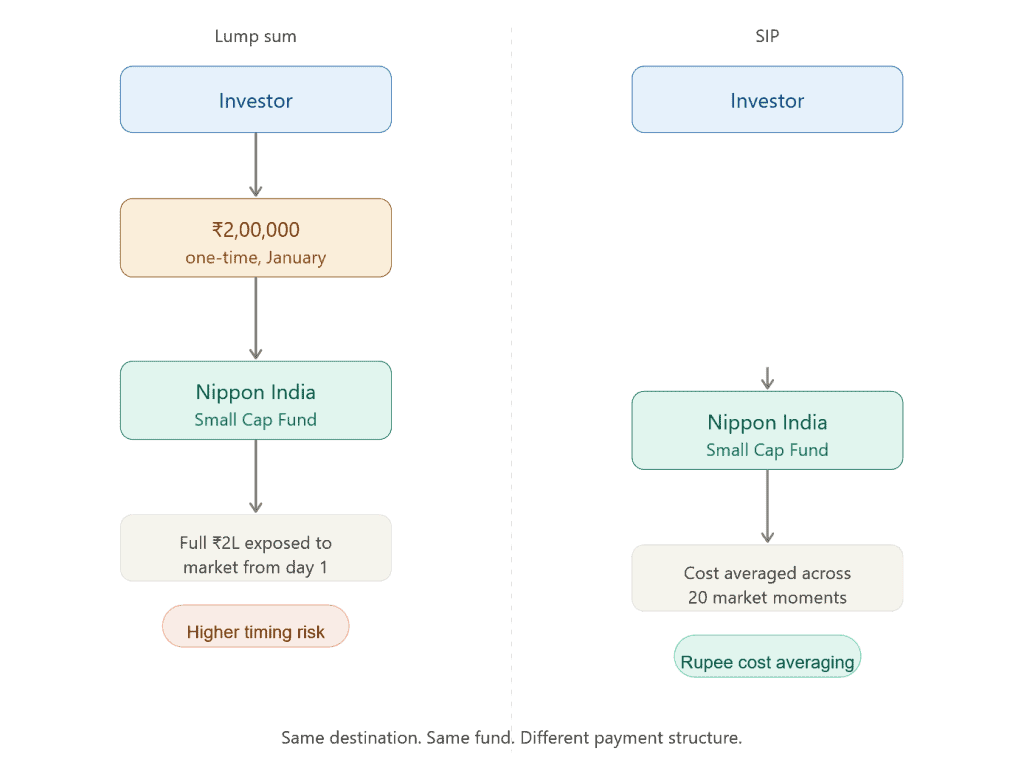

Payment Structure

When you invest in a mutual fund through a lump sum, you put in all your money at once. For instance, you invest ₹2,00,000 in the Nippon India Small Cap Fund in one go in January.

With a SIP, you break that same ₹2,00,000 into smaller, regular amounts. You invest ₹10,000 every month for 20 months into the same fund. The destination is the same — the payment structure is different.

Investment Timing and Strategy

When you invest in a mutual fund as a lump sum, timing matters a great deal. If you invest at a market peak — say, just before a sharp correction, as many did in October 2021 before the mid-cap selloff — your returns can take years to recover.

A SIP removes this burden of timing. Since you are investing consistently over months and years, your cost gets averaged across different market levels. This is especially helpful during uncertain periods, such as the COVID-19 market fall in March 2020, when SIP investors who continued their investments benefited from the sharp recovery.

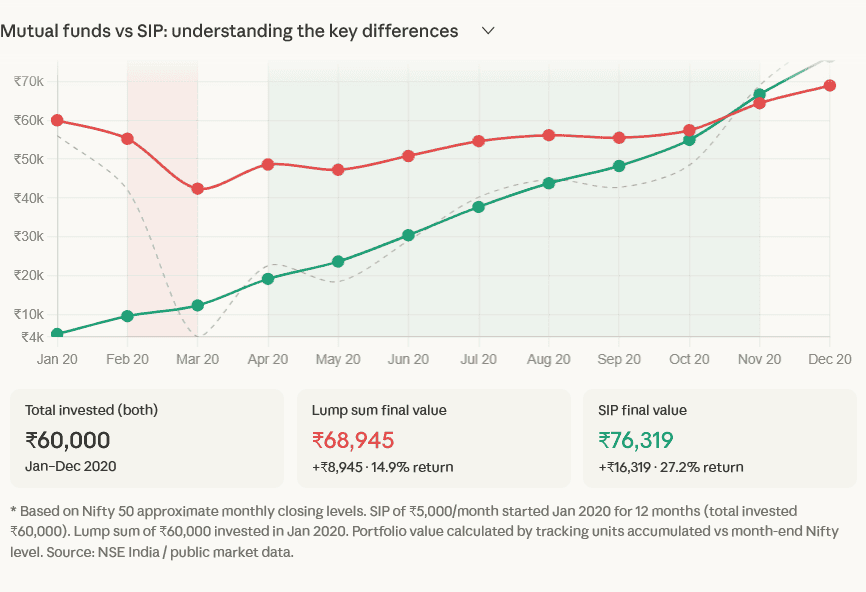

Let us see this with a real example –

* Based on Nifty 50 approximate monthly closing levels. SIP of ₹5,000/month started Jan 2020 for 12 months (total invested ₹60,000). Lump sum of ₹60,000 invested in Jan 2020. Portfolio value calculated by tracking units accumulated vs the month-end Nifty level. Source: NSE India / public market data.

Here’s what the chart shows, based on real Nifty 50 monthly closing levels:

Scenario: ₹60,000 total investment — either all at once in January 2020, or as ₹5,000/month through the year.

What happened to the lump sum investor: Nifty crashed 38% to 7,610 by March 23, 2020. Anyone who put ₹60,000 in January watched it fall to roughly ₹42,000 by March — a ₹18,000 paper loss in just 8 weeks. Even though the market recovered strongly, the investor spent months deep in the red, testing their nerves.

What happened to the SIP investor: The March crash worked in it favour. When ₹5,000 went in at ~8,598 (March closing), it bought far more units than the same amount in January. Those extra units compounded hard as Nifty nearly doubled from the March 2020 bottom within one year.

By December 2020, the SIP portfolio edged out the lump sum — not because timing was lucky, but because the automated monthly buying captured the bottom without the investor having to make any brave decision. Hover over the chart to see month-by-month portfolio values for both approaches.

Risk Mitigation

A lump sum investment carries higher short-term risk because your entire amount is exposed to market movements from day one. If the Sensex drops by 15% right after you invest, your portfolio takes the full hit.

A SIP mitigates this risk by spreading your exposure over time. A 15% market drop after one SIP instalment means only that the instalment is affected. The next one will actually benefit from the lower prices. Over a long period, this averaging reduces the overall impact of market volatility on your portfolio.

Flexibility

Mutual funds — as a product — offer a great deal of flexibility. You can invest any amount at any time, switch between funds, or redeem partially or fully whenever you want (subject to exit loads and lock-in periods).

A SIP, as a mode of investment, has a structured nature. You commit to a fixed amount on a fixed date. However, most platforms today allow you to pause, increase, decrease, or stop your SIP without penalties.

Returns

In theory, a lump sum deployed into a mutual fund at an opportune stage can deliver stronger returns than a SIP across the same horizon, as more capital is put to work from day one and remains exposed for a longer stretch.

Yet real world investing is rarely that precise. Few people are able to judge entry points with dependable accuracy. A SIP may fall short of a perfectly executed bulk deployment, though it can still hold up better than a misplaced one and provide a more even route to building wealth.

Affordability

Not everyone has ₹50,000 or ₹1,00,000 sitting idle to invest at once. That is where SIPs win on pure accessibility. You can start a SIP with as little as ₹100 per month on several platforms.

Mutual funds as a product also have relatively low entry points for lump sum investments — many funds allow you to start with ₹500 or ₹1,000. But the discipline of a SIP, where money goes out automatically on a set date, makes it far easier for regular investors to stay consistent without overthinking it.

Volatility

Market volatility affects lump sum investments directly and immediately. If you invest ₹5,00,000 during a volatile phase, every percentage move up or down in the market hits your entire corpus.

With a SIP, volatility actually works in your favour over the long term. When the market is down, your fixed monthly amount buys more units. When the market recovers, the additional units you accumulated during the dip generate better returns. This is why financial advisors often say: ‘Do not stop your SIPs during a market crash. That is when they work the hardest for you.’

Investment Form

A mutual fund can be invested in through multiple forms — lump sum, SIP, STP (Systematic Transfer Plan), or SWP (Systematic Withdrawal Plan). Each serves a different purpose.

A SIP, specifically, is designed for regular, disciplined, long-term wealth creation. It is the most common and recommended form of investment for retail investors in India, primarily because it removes two of the biggest obstacles to investing: the need for a large initial amount and the temptation to time the market.

Conclusion

Mutual funds and SIPs are often framed as rival choices, but that misses the point. One is the actual investment vehicle, while the other is simply a route to enter it. The more suitable option depends on your income flow, financial aims, and tolerance for volatility.

Those with a sizeable corpus and a fair read of market swings may prefer deploying money in one go. By contrast, salaried earners who want a steadier and more disciplined path may find periodic contributions far more practical.

What truly matters is getting underway. A longer holding period often counts for more than chasing the perfect entry level. Whether you choose staggered contributions or a one-time allocation, the first move carries the most weight.