In a country where value-conscious consumers dominate, Avenue Supermarts has built an empire by redefining how India shops. Through its flagship DMart chain, the company combines aggressive pricing, efficient operations, and deep supplier relationships to capture the modern retail market. As the organized retail sector in India expands rapidly, DMart’s proven “everyday low prices” strategy positions it to remain at the forefront of consumption growth.

But does Avenue Supermarts offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | DMART |

| Industry/Sector | Retailing |

| CMP | 4694.30 |

| Market Cap (₹ Cr.) | 3,05,474 |

| P/E | 112.93 (Vs Industry P/E of 102.20) |

| 52 W High/Low | 5,484.85 / 3,340.00 |

| EPS (TTM) | 41.60 |

| Dividend Yield | 0.00% |

About Avenue Supermarts

Avenue Supermarts, incorporated in 2000 by retail entrepreneur Radhakishan Damani, operates under the DMart brand – a network of large-format value retail stores focused on food, FMCG, apparel, and general merchandise. Headquartered in Mumbai, the company has steadily expanded across India and today commands one of the strongest footholds in organized food and grocery retail, a segment with massive untapped potential in India.

Key business segments

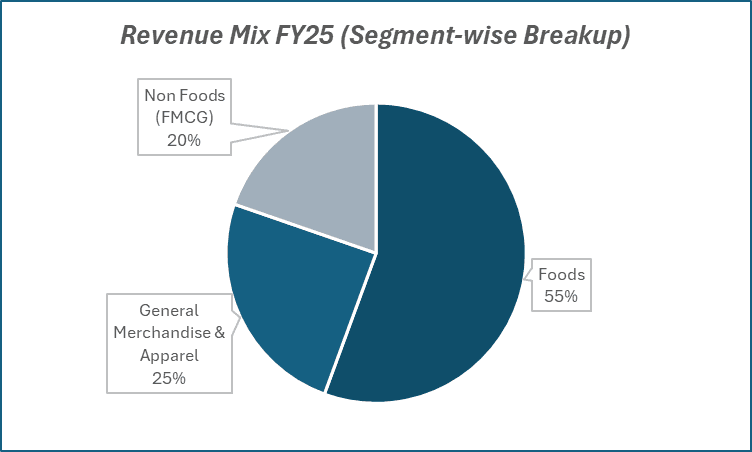

Avenue Supermarts operates primarily in the following key business segments:

- Food & Grocery – Staples, packaged foods, dairy, and household essentials forming the core of DMart’s value proposition.

- FMCG & Personal Care – Leading consumer brands in packaged goods, hygiene, and personal care, offered at competitive prices.

- General Merchandise & Apparel – Apparel, kitchenware, home essentials, and discretionary categories that drive higher-margin growth.

- DMart Ready (E-Commerce) – Online grocery and essentials delivery service in select cities, leveraging DMart’s supply chain efficiency.

Primary growth factors for Avenue Supermarts

Avenue Supermarts key growth drivers:

- Low-Cost Leadership – Everyday low-price strategy ensures customer stickiness and repeat footfall.

- Retail Expansion – Aggressive store rollouts in underpenetrated Tier-2 and Tier-3 cities.

- Rising Disposable Incomes – Increasing shift from unorganized kirana stores to organized retail formats.

- E-Commerce Complement – DMart Ready offers an omni-channel strategy to retain relevance in digital-first urban consumers.

- Operational Efficiency – Tight inventory control and strong supplier terms ensure superior working capital management.

Detailed competition analysis for Avenue Supermarts

Key financial metrics – TTM;

| Company | Revenue(₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E (TTM) |

| Avenue Supermarts | 61648.61 | 4565.12 | 7.41% | 2706.58 | 4.39% | 112.93 |

| Trent Ltd. | 17913.65 | 2984.81 | 16.66% | 1527.79 | 8.53% | 121.54 |

| Vishal Mega Mart | 10716.34 | 1530.18 | 14.28% | 631.97 | 5.90% | 101.76 |

| Arvind Fashions Ltd. | 4772.31 | 619.85 | 12.99% | 45.75 | 0.96% | – |

| Aditya Birla Fashion | 11499.49 | 1312.79 | 11.42% | -628.39 | -5.46% | – |

Key insights on Avenue Supermarts

- Avenue Supermarts has built one of the most profitable models in Indian retail, unlike peers struggling with high costs.

- The food and grocery segment ensures resilience even during economic slowdowns, making DMart a defensive play.

- Store expansion strategy continues to prioritize owned properties over leased, ensuring lower rental liabilities in the long run.

- DMart Ready is still at a nascent scale but provides a strategic hedge against the rapid rise of online grocery players.

- The company enjoys strong brand trust among value-seeking Indian households, ensuring repeat purchases and loyalty.

Recent financial performance of Avenue Supermarts for Q1 FY26

| Metric | Q1 FY25 | Q4 FY25 | Q1 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Revenue (₹ Cr.) | 14069.14 | 14871.86 | 16359.70 | 10.00% | 16.28% |

| EBITDA (₹ Cr.) | 1221.25 | 955.07 | 1299.04 | 36.02% | 6.37% |

| EBITDA Margin (%) | 8.68% | 6.42% | 7.94% | 152 bps | -74 bps |

| PAT (₹ Cr.) | 773.68 | 550.79 | 772.81 | 40.31% | -0.11% |

| PAT Margin (%) | 5.50% | 3.70% | 4.72% | 102 bps | -78 bps |

| Adjusted EPS (₹) | 11.89 | 8.47 | 11.88 | 40.26% | -0.08% |

Avenue Supermarts financial update (Q1 FY26)

Financial performance

- Revenue from operations stood at ₹16,360 crore (up 16.3% YoY); net profit was stable at ₹773 crore (down 0.1% YoY).

- EBITDA margin remained around 7.6% for FY25; PAT margin at 4.5%.

- DMart Ready (e-commerce) grew revenue 20.8% YoY to ₹3,502 crore, though losses widened to ₹247 crore.

Business highlights

- Added 50 new stores in FY25, taking the total count to 415; total retail area expanded by 2 mn sq. ft. to 17.2 mn sq. ft.

- Like-for-Like growth for stores older than 2 years at 8.4% in FY25.

- Bill cuts rose to 35.3 crore (from 30.3 crore in FY24).

- Revenue per sq. ft. stood at ₹33,896; inventory turnover ratio at 13.6x.

- DMart Ready is now operational in 24 cities, with ~65% of deliveries completed within 12 hours and all within 24 hours.

- Store-level metrics remain robust despite rising warehouse rentals and employee costs.

Outlook

- Management remains bullish on brick-and-mortar expansion while scaling up DMart Ready.

- Plans to accelerate store additions, with strong focus on North India (particularly Uttar Pradesh).

- DMart Ready to enhance fulfillment capabilities with the vision of delivering all orders within 6 hours.

Recent Updates on Avenue Supermarts

- Continued expansion into new geographies with focus on Tier-2 cities to capture underserved markets.

- Investment in supply chain and backend logistics to support long-term efficiency and e-commerce expansion.

- Introduced private label products in select categories, enhancing margins and competitive positioning.

- Piloted new digital initiatives within DMart Ready for improved customer experience.

Company valuation insights – Avenue Supermarts

Avenue Supermarts is currently trading at a TTM P/E of 112.9, above the industry average of 102.2, with a 1-year return of -5.4% versus Nifty 50’s -0.6%.

Despite near-term pressures from rising land acquisition costs, wage inflation, and a deteriorating product mix in non-FMCG categories, the company’s long-term growth visibility remains intact. DMart continues to focus on aggressive store expansion (~20% addition annually), with a strong push into North India, particularly Uttar Pradesh, while also deepening penetration in existing clusters.

Its e-commerce venture, DMart Ready, is scaling steadily with ~21% revenue growth in FY25 and a strong customer stickiness, though profitability remains elusive in the near term. Structural challenges persist in apparel, but food and FMCG categories continue to anchor growth. The company’s cluster-based expansion model, value retail proposition, and strong brand recall provide a competitive edge against quick commerce and organized retail peers. Management expects bill cuts to grow at 15–16% CAGR with improving throughput, supporting healthy revenue traction.

We value Avenue Supermarts at 90x FY27E EPS of ₹63 to arrive at a 12-month target price of ₹5,670, implying a 20% upside from current levels. A short-term target of ₹5,100 implies an 8% upside over 3 months, supported by steady sales growth, robust store expansion, and increasing consumer footfalls.

Major risk factors affecting Avenue Supermarts

- High Valuations – Premium multiples leave little margin for execution errors.

- Competition from Online Retail – Aggressive players like Reliance Retail, Amazon, and Flipkart could pressure margins.

- Execution Risks in Expansion – Rapid rollout in new cities carries risks of operational inefficiencies.

- Consumer Slowdown – Inflationary pressures could impact discretionary segments like apparel and general merchandise.

Technical analysis of Avenue Supermarts share

Avenue Supermarts has been trading in a sideways channel but recently broke above the upper trendline, gaining ~7% since confirming the breakout. The move signals renewed bullish momentum and opens the potential for further upside.

The stock trades comfortably above its 50-day, 100-day, and 200-day EMAs, underscoring a well-established upward trend.

Momentum indicators strengthen the bullish setup. The MACD is firmly positive at 139.55, with the MACD line trending above the signal line, indicating sustained upward momentum. The RSI stands at 73.52, reflecting strong buying interest, while relative RSI scores of 0.18 (21-day) and 0.13 (55-day) confirm consistent outperformance versus the broader market.

The ADX at 28.32 indicates a strong trend that could gather further strength if the stock sustains above key resistance.

A breakout above ₹5,100 may set the stage for a rally toward ₹5,670, aligning with the 12-month fundamental target. On the downside, ₹4,200 serves as crucial support, and holding above it will be vital to maintaining the bullish structure.

- RSI: 73.52 (Strong Buying Interest)

- ADX: 28.32 (Strong Trend)

- MACD: 139.55 (Firmly Positive)

- Resistance: ₹5,100

- Support: ₹4,200

Avenue Supermarts stock recommendation

Current Stance: Buy, with a 3-month target of ₹5,100 (~8% upside) and a 12-month target of ₹5,670 (~20% upside).

Why buy now?

Aggressive store expansion with strong North India focus.

Resilient demand in food & FMCG driving steady growth.

DMart Ready scaling up with strong customer stickiness.

Efficient operations and high inventory turnover support margins.

A proven cluster model ensures sustainable growth.

Portfolio fit

Avenue Supermarts is India’s leading value retail chain with a dominant presence in the food and grocery segment, underpinned by cost leadership, efficient operations, and strong brand equity. Its dual focus on cluster-based offline expansion and e-commerce scale-up provides a structural growth runway. For investors, DMart offers a rare combination of steady double-digit revenue growth, high operating efficiency, and long-term market leadership in India’s organized retail space.

If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebAvenue Supermarts: Budget 2025-26 opportunities

- Urban boost: Infra & housing push to aid FMCG and discretionary demand.

- Rural tailwind: Higher rural spending to drive staples and value retail.

- Middle-class boost: Tax reliefs to lift food & grocery consumption.

- Supply chain gains: Logistics & warehousing support to cut costs.

- Digital push: Policy support to accelerate DMart Ready’s growth.

Final thoughts

From being a Mumbai-based retailer to becoming a pan-India consumption powerhouse, Avenue Supermarts has transformed how Indians view organized retail. Its DNA of value pricing, efficient supply chain, and relentless customer focus makes it a structural play on India’s consumption growth. For investors, DMart is more than a retail stock – it is a proxy for India’s rising middle-class aspirations and the inevitable shift from unorganized to organized consumption.