India’s telecom sector has evolved from a hyper-competitive industry to a more consolidated, high-entry-barrier market dominated by a few large players. With rising data consumption, 5G rollout, and increasing digital penetration, telecom is no longer just a utility, it is the backbone of India’s digital economy.

Within this ecosystem, Bharti Hexacom Ltd. provides a unique opportunity to participate in telecom growth through a focused regional play under the strong umbrella of the Airtel group.

But does Bharti Hexacom Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | BHARTIHEXA |

| Industry/Sector | Telecom |

| CMP | 1510.00 |

| Market Cap (₹ Cr.) | 75,500 |

| P/E | 45.14 (Vs Industry P/E of 50.75) |

| 52 W High/Low | 2052.90 / 1260.00 |

| EPS (TTM) | 35.10 |

| Dividend Yield | 0.63% |

About Bharti Hexacom Ltd.

Bharti Hexacom Limited is a telecommunications company that provides mobile and broadband services in select circles in India, primarily Rajasthan and the North-East regions. The company operates under the brand and ecosystem of Bharti Airtel Limited.

Bharti Hexacom delivers wireless voice, data services, and enterprise connectivity solutions, leveraging Airtel’s infrastructure, technology, and brand strength. With increasing smartphone penetration and data usage in its operating regions, the company is well positioned to benefit from telecom growth in underpenetrated markets.

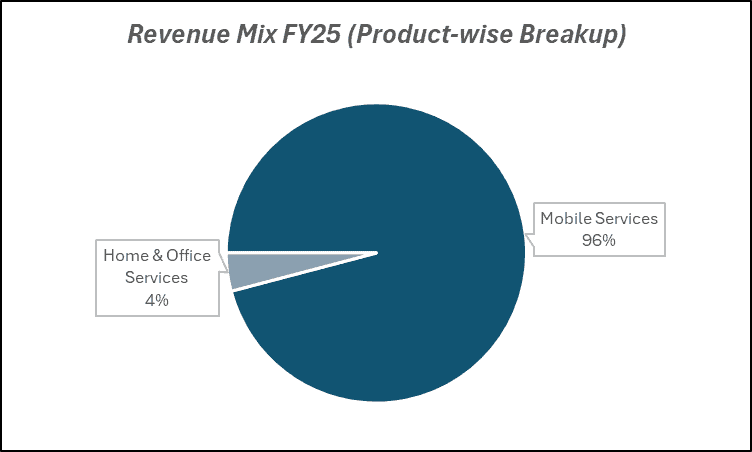

Key business segments

Bharti Hexacom Ltd. operates primarily in the following key business segments:

- Mobile Services: Wireless voice and data services for retail customers.

- Data & Broadband: 4G/5G data services and internet connectivity.

- Enterprise Solutions: Connectivity and communication services for businesses.

- Digital Services: Value-added services including content and digital platforms.

- Infrastructure Utilization: Leveraging telecom network assets across circles.

Primary growth factors for Bharti Hexacom Ltd.

Bharti Hexacom Ltd. key growth drivers:

- Rising Data Consumption: Increasing smartphone usage driving higher ARPU (average revenue per user).

- 5G Rollout & Upgrades: Enhanced data speeds and new use cases boosting demand.

- Operating Leverage in Mature Circles: Incremental revenue growth with relatively stable costs.

- Underpenetrated Markets: Growth potential in Rajasthan and North-East regions.

- Tariff Hikes Potential: Industry-wide pricing discipline supporting revenue growth.

Detailed competition analysis for Bharti Hexacom Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Bharti Hexacom Ltd. | 9229.10 | 4791.00 | 51.91% | 1754.90 | 19.01% | 45.14 |

| Bharti Airtel Ltd. | 203465.80 | 115191.70 | 56.61% | 36713.40 | 18.04% | 30.18 |

| Indus Towers Ltd. | 32119.20 | 17713.50 | 55.15% | 7131.10 | 22.20% | 15.82 |

| Vodafone Idea Ltd. | 44553.70 | 18773.90 | 42.14% | -24586.40 | -55.18% | – |

| TATA Communications Ltd. | 24238.92 | 4660.61 | 19.23% | 1493.30 | 6.16% | 23.23 |

Key insights on Bharti Hexacom Ltd.

- Strong backing and ecosystem support from Bharti Airtel.

- High operating leverage due to established infrastructure.

- Beneficiary of structural growth in data consumption.

- Focused geographic presence allows targeted growth.

- Telecom sector consolidation improves pricing power.

Recent financial performance of Bharti Hexacom Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 2250.70 | 2317.30 | 2359.80 | 1.83% | 4.85% |

| EBITDA (₹ Cr.) | 1151.70 | 1208.10 | 1254.40 | 3.83% | 8.92% |

| EBITDA Margin (%) | 51.17% | 52.13% | 53.16% | 103 bps | 199 bps |

| PAT (₹ Cr.) | 260.90 | 421.20 | 473.70 | 12.46% | 81.56% |

| PAT Margin (%) | 11.59% | 18.18% | 20.07% | 189 bps | 848 bps |

| Adjusted EPS (₹) | 5.22 | 8.42 | 9.47 | 12.47% | 81.42% |

Bharti Hexacom Ltd. financial update (Q3 FY26)

Financial performance

- Revenue grew 5% YoY to ₹2360 Cr in Q3FY26, driven by steady growth in wireless services and improving subscriber mix.

- EBITDA increased ~9% YoY to ₹1254 Cr, with margins expanding 199 bps YoY to 53.2%, supported by operating leverage.

- PAT rose 82% YoY to ₹474 Cr, aided by margin expansion and a lower effective tax rate during the quarter.

- 9MFY26 revenue/EBITDA/PAT grew 11%/20%/59% YoY, reflecting strong profitability momentum.

- Free cash flow improved to ₹660 Cr in Q3, while net debt reduced significantly to ₹2160 Cr, indicating strengthening balance sheet.

Business highlights

- Wireless revenue grew 4% YoY with ARPU improving to ₹253, supported by better subscriber mix and data monetization.

- The home broadband segment remained a key growth driver, with subscriber base, revenue, and EBITDA witnessing strong double-digit growth.

- Overall EBITDA growth (4% QoQ) was led by robust expansion in the home broadband (HBB) segment.

- Capex moderated (7% QoQ) to ₹340 Cr, improving cash flow generation while maintaining network investments.

- Data consumption remained strong, with usage rising to 32GB per user per month, indicating sustained demand tailwinds.

Outlook

- Revenue and EBITDA are expected to grow at 11% and 17% CAGR over FY25-28, driven by tariff hikes and data growth.

- Potential tariff hikes could significantly boost ARPU and profitability going forward.

- Expansion of fixed wireless access (FWA) and home broadband presents a large untapped opportunity in low-penetration circles.

- Strong free cash flow generation and low leverage (0.5x) provide headroom for continued investments in 5G rollout and network expansion.

- Strategic focus on improving market share in underpenetrated regions and scaling digital services could drive long-term growth visibility.

Recent Updates on Bharti Hexacom Ltd.

- Continued rollout of 5G services in operating regions.

- Network expansion and capacity enhancement initiatives.

- Growth in data usage and subscriber additions.

- Strengthening of digital service offerings.

- Improving ARPU trends in line with industry dynamics.

Company valuation insights – Bharti Hexacom Ltd.

Bharti Hexacom is currently trading at an EV/EBITDA of 19.2x, after delivering a modest ~4% return over the last one year, outperforming the NIFTY 50 which declined ~3.3% during the same period. The premium valuation reflects investor confidence in its strong growth positioning within underpenetrated telecom circles, improving return ratios, and increasing visibility on long-term data and broadband monetisation.

The investment case for Bharti Hexacom is supported by its unique positioning as a pure-play on the fast-growing wireless and home broadband (HBB) segments in regions with relatively low data and broadband penetration. The company is witnessing steady ARPU expansion, rising data consumption, and strong traction in home broadband, which is emerging as a key growth driver. Additionally, improving free cash flow generation, low leverage, and disciplined capital allocation provide flexibility to invest in 5G rollout and fixed wireless access (FWA) expansion. With potential tariff hikes, continued market share gains, and increasing digital adoption, Bharti Hexacom is well placed to deliver sustained revenue and EBITDA growth over the medium to long term.

From a valuation perspective, applying a 15x EV/EBITDA multiple to FY28E estimates, we derive a 12-month target price of ₹1,870, implying an upside potential of 24% from current levels. Over the near term, we assign a 6-month target price of ₹1,600, indicating a 6% upside, supported by improving ARPU trends, strong broadband momentum, and continued operating leverage.

Major risk factors affecting Bharti Hexacom Ltd.

- Regulatory Risk: Spectrum costs, government policies, and telecom regulations.

- Competition: Competitive pressure from other telecom operators.

- Capex Intensity: Continuous investment required for network upgrades (4G/5G).

- Tariff Sensitivity: Delays in tariff hikes impacting revenue growth.

- Technology Risk: Rapid evolution of telecom technologies.

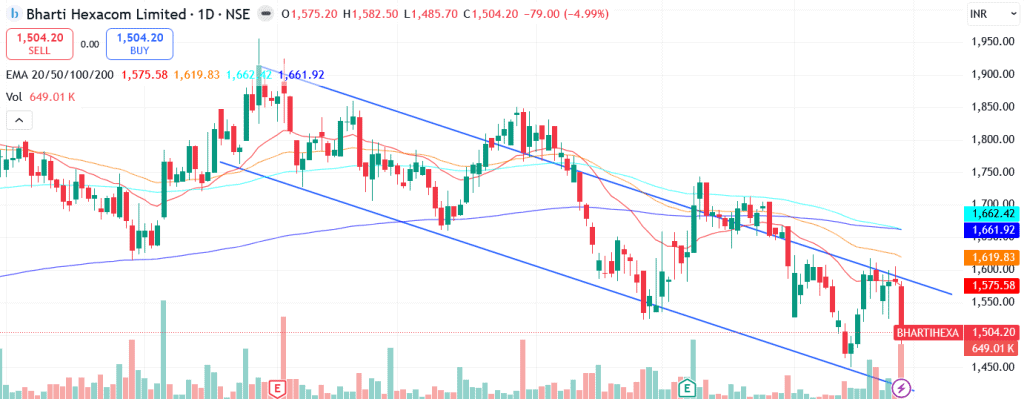

Technical analysis of Bharti Hexacom Ltd. share

Bharti Hexacom is currently in a corrective phase, tracking the broader market weakness, with the stock trending below its key moving averages. However, early signs of base formation are emerging, indicating the possibility of a trend reversal from current levels.

The stock is trading below its 20-, 50-, 100-, and 200-day EMAs, reflecting short-term weakness and a prevailing downtrend. Despite this, improving momentum indicators suggest that the selling pressure may be easing and a reversal could be underway.

Momentum indicators are turning constructive. The MACD at -22.99 remains in negative territory but has crossed above the signal line, indicating a potential bullish reversal and emerging entry opportunity. The RSI at 48.02 reflects moderate buying interest, while the 21-day and 55-day Relative RSI readings at 0.03 and 0.01 suggest early signs of outperformance versus the broader market. Meanwhile, the ADX at 24.70 indicates a strong existing trend, which is currently downward, but the improving momentum signals point toward a possible shift in direction.

A decisive move above ₹1,600 could signal a reversal and open the path toward ₹1,870, aligning with our 12-month fundamental target. On the downside, ₹1,410 remains a crucial support level, below which the current structure could weaken.

- RSI: 48.02 (Decent buying interest)

- ADX: 24.70 (Strong trend; currently downward, potential reversal ahead)

- MACD: -22.99 (Negative; bullish crossover above signal line)

- Resistance: ₹1,600

- Support: ₹1,410

Bharti Hexacom Ltd. stock recommendation

Current Stance: Buy, with a 6-month target of ₹1,600 (6% upside) and a 12-month target of ₹1,870 (24% upside), based on 15x FY28E EV/EBITDA.

Why buy now?

Strong growth visibility in wireless and home broadband (HBB) segments, particularly in underpenetrated circles with rising data consumption.

Improving ARPU trajectory supported by premiumisation, better subscriber mix, and potential tariff hikes.

Home broadband and fixed wireless access (FWA) emerged as key growth drivers, with significant headroom for penetration.

Robust free cash flow generation and low leverage (~0.5x) enabling continued investments in 5G rollout and network expansion.

Backed by the broader Bharti ecosystem, with disciplined capital allocation and strong return ratios driving long-term value creation.

Portfolio fit

Bharti Hexacom offers exposure to India’s long-term digital consumption and telecom growth through its strong presence in underpenetrated circles. With rising data usage, improving ARPU trajectory, and rapid expansion in home broadband and fixed wireless access, the company is well positioned to benefit from increasing internet penetration and digital adoption. Supported by strong free cash flow generation, low leverage, and backing from the Bharti ecosystem, the stock fits well in portfolios seeking a combination of growth, improving profitability, and long-term participation in India’s digital infrastructure story.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebBharti Hexacom Ltd.: Budget 2026-27 opportunities

- Digital India Push: Increased telecom usage driven by digital services adoption.

- Rural Connectivity Initiatives: Expansion of telecom infrastructure in underserved regions.

- 5G Ecosystem Development: Government support for next-gen telecom infrastructure.

- Data Economy Growth: Increased demand for mobile data and broadband services.

- Enterprise Digitization: Rising demand for enterprise connectivity solutions.

Final thoughts

Bharti Hexacom Limited stands at an interesting position within India’s telecom landscape, offering exposure to a structurally growing sector with strong backing from the Airtel ecosystem. With rising data consumption, improving pricing power, and ongoing 5G rollout, the company is well positioned to benefit from India’s digital transformation.

For investors seeking exposure to telecom with a blend of stability and growth, Bharti Hexacom offers a combination of predictable cash flows, operating leverage, and long-term participation in India’s expanding digital economy.