India’s booming e-commerce and consumption-driven economy have unlocked massive opportunities for logistics and supply chain companies. At the center of this transformation is Delhivery, a tech-driven logistics player that has rapidly evolved into one of India’s largest integrated logistics platforms. With its data-driven approach, pan-India network, and scalable asset-light model, Delhivery is positioned as a structural play on India’s digital commerce and supply chain modernization story.

But does Delhivery offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | DElHIVERY |

| Industry/Sector | Logistics & Supply Chain Services |

| CMP | 472.95 |

| Market Cap (₹ Cr.) | 35,320 |

| P/E | 178.03 (Vs Industry P/E of 102.20) |

| 52 W High/Low | 477.75 / 236.53 |

| EPS (TTM) | 2.66 |

| Dividend Yield | 0.00% |

About Delhivery Ltd

Founded as a tech-enabled logistics company, Delhivery is among India’s largest integrated logistics providers offering services across express parcel delivery, freight (PTL, TL), warehousing, supply chain solutions, cross-border express, and various value-added services such as e-commerce returns, payment collections, installation & assembly, and fraud detection. The company serves over countries and territories, catering to e-commerce, manufacturing, and retail sectors with a strong technology-driven approach.

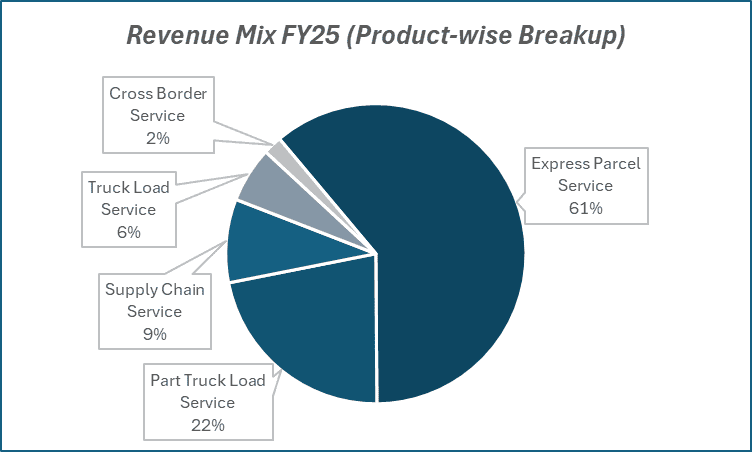

Key business segments

Delhivery Ltd. operates primarily in the following key business segments:

- Parcel & Express Delivery: Core service for B2C deliveries, focusing on e-commerce.

- Freight Services: Includes part truckload (PTL), full truckload (TL), and other freight logistics.

- Warehousing & Supply Chain: Providing storage and end-to-end supply chain solutions.

- Value-Added Services: Reverse logistics, payment collection, installation, assembly.

- Cross-border Logistics: Enabling international shipping and logistics solutions for Indian businesses.

Primary growth factors for Delhivery

Delhivery key growth drivers:

- Strong technology integration enabling efficient delivery logistics and scalability.

- Growing e-commerce ecosystem in India fueling demand for last-mile delivery.

- Expansion in B2B freight and warehousing sectors, leveraging Indian infrastructure growth.

- Improvement in working capital management reducing cycle times (working capital days reduced from 118 to 67.5).

- Pan-India network expansion including rural and semi-urban penetration.

- Growing international cross-border logistics business.

- Partnerships and investments in tech to improve automation and service reliability.

Detailed competition analysis for Delhivery

Key financial metrics – TTM;

| Company | Revenue(₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E (TTM) |

| Delhivery Ltd. | 9,053.60 | 427.58 | 4.72% | 198.12 | 2.19% | 178.03 |

| Blue Dart Express Ltd | 5819.39 | 866.03 | 14.88% | 247.83 | 4.26% | 55.56 |

| Concor Ltd | 8937.52 | 1920.26 | 21.49% | 1258.59 | 14.08% | 32.18 |

| ALlcargo Gati Ltd. | 1609.48 | 61.89 | 3.85% | 14.96 | 0.93% | 51.86 |

Key insights on Delhivery

- Delhivery has built a pan-India integrated platform unmatched by smaller logistics players.

- Strong operating leverage potential as utilization of processing centers and fleet improves with scale.

- The company has achieved sequential improvement in profitability, moving closer toward sustained breakeven margins.

- Expansion into PTL/FTL freight creates a diversified revenue base, reducing e-commerce cyclicality.

- Partnerships with SMEs and D2C brands ensure sticky long-term contracts.

Recent financial performance of Delhivery for Q1 FY26

| Metric | Q1 FY25 | Q4 FY25 | Q1 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Revenue (₹ Cr.) | 2172.30 | 2191.57 | 2294.00 | 4.67% | 5.60% |

| EBITDA (₹ Cr.) | 97.06 | 119.07 | 148.82 | 24.99% | 53.33% |

| EBITDA Margin (%) | 4.47% | 5.43% | 6.49% | 106 bps | 202 bps |

| PAT (₹ Cr.) | 55.58 | 55.64 | 98.61 | 77.23% | 77.42% |

| PAT Margin (%) | 2.56% | 2.54% | 4.30% | 176 bps | 174 bps |

| Adjusted EPS (₹) | 0.74 | 0.97 | 1.22 | 25.77% | 64.86% |

Delhivery financial update (Q1 FY26)

Financial performance

- Revenue from operations stood at ₹2,294 crore (up 5.6% YoY); PAT surged to ₹99 crore (up 77.4% YoY).

- EBITDA rose 53% YoY to ₹149 crore, with margins improving 202 bps YoY to 6.5%; adjusted EBITDA margin expanded 160 bps YoY to 3.3%.

- Service EBITDA stood at ₹298 crore, with margin at 13%. PAT margin expanded by 140 bps YoY to 3.8%.

Business highlights

- Delivered positive operating profit and net profit in FY25 after years of losses.

- Working capital cycle improved from 118 days to 67.5 days, freeing cash.

- Expanded freight and warehousing services to complement express delivery.

- Continued expansion in cross-border logistics solutions.

- Investment in technology to automate operations and improve delivery experience.

Outlook

- Management expects express parcel volumes to sustain strong momentum through Q2 FY26, with segment EBITDA margins in the 16–18% range.

- PTL margins are expected to improve further.

- PAT margin is guided to strengthen through FY26.

- With Ecom Express integration, reach is expected to expand to ~19,200 pin codes, enhancing network scale.

- The company plans to scale its B2B rapid commerce business, supported by operating leverage and expanded infrastructure.

Recent Updates on Delhivery

- Announced capacity expansion in warehousing and fulfillment centers to strengthen supply chain services.

- Introduced new AI-led logistics solutions, improving real-time visibility and predictive analytics for clients.

- Scaling up cross-border services amid India’s rising exports and global trade integration.

- Increasing focus on green logistics, including EV adoption and renewable energy-powered hubs.

Company valuation insights – Delhivery

Delhivery is currently trading at a TTM P/E of 178.0, significantly above the industry average of 102.2, with a 1-year return of 9.8% versus Nifty 50’s -0.6%.

The company’s medium-term growth outlook is supported by strong execution in express parcels (growing ~14% YoY in volumes with EBITDA margins at 16.3%) and steady traction in PTL (17% YoY growth with margin improvement).

The recent acquisition of Ecom Express expands its reach to ~19,200 pin codes and enhances scale benefits, while integration synergies are expected to drive cost efficiencies.

Delhivery’s focus on operating leverage, rapid commerce expansion, and disciplined capital allocation provides a credible path toward sustained profitability. Rising share of high-margin segments, improving service EBITDA (13% in Q1 FY26), and further scale-up in B2B logistics position the company well to strengthen margins and accelerate earnings growth.

We value Delhivery at 60x FY27E EBITDA of ₹9.5 to arrive at a 12-month target price of ₹570, implying a 20% upside from current levels. A short-term target of ₹510 implies a 7% upside over 3 months, supported by sustained express parcel momentum, PTL margin expansion, and Ecom Express integration benefits.

Major risk factors affecting Delhivery

- Sustained profitability is yet to be proven over multiple quarters.

- Economic slowdown or e-commerce disruption could impact delivery volumes.

- High capital investments could pressure cash flow.

- Competitive pressure from large integrators and global logistics players.

- Macro challenges such as fuel price inflation affecting cost structure.

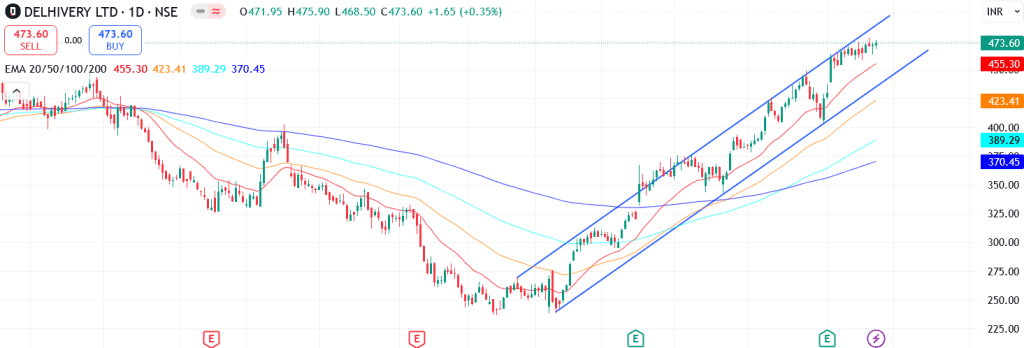

Technical analysis of Delhivery share

Delhivery has been trading within a long-term ascending channel and is currently consolidating near the channel’s upper trendline. A decisive breakout above this level could trigger strong upward momentum.

The stock trades comfortably above its 50-day, 100-day, and 200-day EMAs, underscoring a well-established upward trend.

Momentum indicators largely support the bullish setup. The MACD is firmly positive at 15.70, though the MACD line is just below the signal line, a bullish crossover could confirm renewed upward momentum. The RSI stands at 69.42, indicating strong buying interest, while relative RSI scores of 0.08 (21-day) and 0.28 (55-day) highlight consistent outperformance versus the broader market.

The ADX at 42.63 indicates a strong trend, which could strengthen further if the stock breaks above key resistance.

A breakout above ₹510 could set the stage for a rally toward ₹570, aligning with the 12-month fundamental target. On the downside, ₹430 serves as a crucial support level, and holding above it will be vital to maintaining the bullish structure.

- RSI: 69.42 (Strong Buying Interest)

- ADX: 42.63 (Strong Trend)

- MACD: 15.70 (Firmly Positive)

- Resistance: ₹510

- Support: ₹430

Delhivery stock recommendation

Current Stance: Buy, with a 3-month target of ₹510 (~7% upside) and a 12-month target of ₹570 (~20% upside).

Why buy now?

Express parcel momentum: Strong volume growth (~14% YoY in Q1FY26) with margins improving to 16.3% supports steady profitability.

PTL strength: 17% YoY revenue growth with yield improvement and margin expansion positions PTL as a key growth driver.

Ecom Express acquisition: Expands reach to ~19,200 pin codes, enhancing scale and synergies that will improve efficiency.

Operating leverage: Rising service EBITDA (13% in Q1FY26) and flat corporate overheads as a % of revenue are boosting margin trajectory.

New growth engines: Investments in rapid commerce and B2B solutions provide long-term optionality beyond core express delivery.

Portfolio fit

Delhivery is India’s leading integrated logistics player with a technology-driven platform, pan-India reach, and diversified service lines across express parcels, PTL, FTL, and supply chain solutions. Its structural growth is anchored by e-commerce tailwinds, scale-driven cost efficiencies, and strategic acquisitions like Ecom Express. For investors, Delhivery offers exposure to India’s fastest-growing logistics ecosystem, with improving profitability and strong long-term growth visibility.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebDelhivery: Budget 2025-26 opportunities

- E-commerce & Consumption Boost: Higher government focus on digital commerce, MSME support, and rising consumption to drive parcel volumes and last-mile delivery demand.

- Infra & Logistics Push: Increased allocations to roads, railways, and dedicated freight corridors to improve transit times and reduce logistics costs.

- Rural Connectivity: Expansion of rural infrastructure and digital penetration to accelerate parcel deliveries and broaden reach into underserved markets.

- Export & Trade Facilitation: Simplified customs and new trade agreements to enhance cross-border logistics and strengthen global partnerships.

- Technology & Sustainability Support: Incentives for green logistics, EV adoption, and warehouse automation to drive efficiency and support Delhivery’s premium positioning.

Final thoughts

Delhivery isn’t just a logistics company, it is building the digital backbone of India’s commerce ecosystem. With its unique blend of technology, scale, and operational efficiency, it represents the future of logistics in India. For investors, Delhivery offers a high-growth, high-potential story, albeit with execution risks. As profitability visibility improves, it could transform into one of the most powerful compounding plays in India’s consumption and e-commerce value chain.