India’s pharmaceutical sector continues to be a global powerhouse, driven by cost-efficient manufacturing, strong domestic demand, and increasing export opportunities. Within this space, companies that combine API strength with branded formulations often enjoy better margin control and strategic flexibility.

Ipca Laboratories Ltd. stands out as a vertically integrated pharma player with a strong presence in APIs and formulations across domestic and international markets. With a legacy in anti-malarial drugs and expanding global footprint, the company represents a blend of defensive healthcare demand and export-driven growth.

But does Ipca Laboratories Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | IPCALAB |

| Industry/Sector | Healthcare |

| CMP | 1594.50 |

| Market Cap (₹ Cr.) | 40,453 |

| P/E | 42.42 (Vs Industry P/E of 32.08) |

| 52 W High/Low | 1624.00 / 1168.20 |

| EPS (TTM) | 37.09 |

| Dividend Yield | 0.25% |

About Ipca Laboratories Ltd.

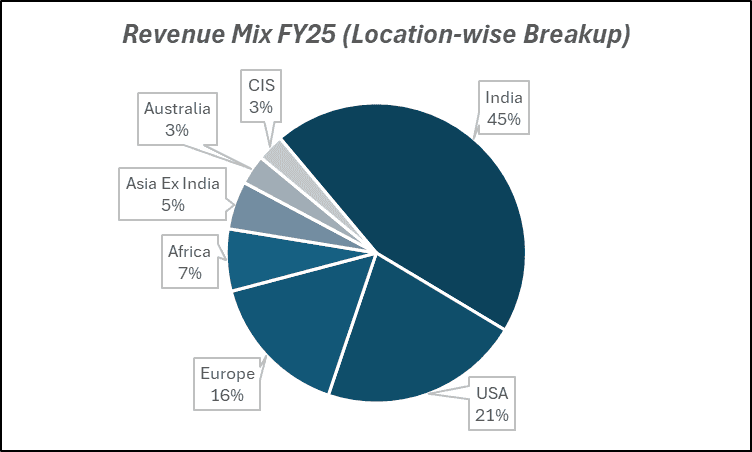

Ipca Laboratories Limited is an integrated pharmaceutical company engaged in the manufacturing and marketing of active pharmaceutical ingredients (APIs) and formulations. Established in 1949 and headquartered in Mumbai, the company has a strong presence across India, the United States, Africa, and other global markets.

Ipca is a leading manufacturer of APIs for several therapeutic categories and is one of the world’s largest producers of certain anti-malarial drugs. Its integrated operations allow it to control costs and maintain quality across the value chain.

Key business segments

Ipca Laboratories Ltd. operates primarily in the following key business segments:

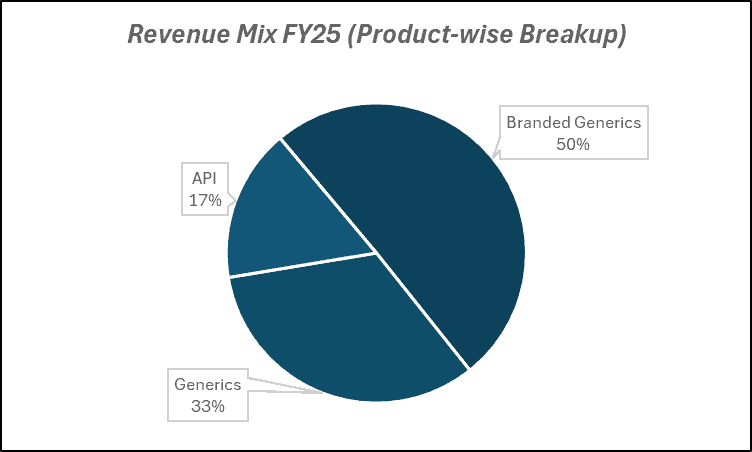

- Domestic Formulations: Branded medicines across therapeutic areas in India.

- International Formulations: Generic formulations for regulated and emerging markets.

- Active Pharmaceutical Ingredients (API): Manufacturing of APIs for internal and external use.

- Institutional Business: Supplies to global health programs and government tenders.

- Contract Manufacturing: Third-party manufacturing for global pharmaceutical companies.

Primary growth factors for Ipca Laboratories Ltd.

Ipca Laboratories Ltd. key growth drivers:

- Strong API Integration: Backward integration supporting cost efficiency and margin stability.

- Domestic Formulations Growth: Rising healthcare demand driving prescription growth in India.

- Export Market Expansion: Increasing presence in regulated and emerging markets.

- Institutional Business Opportunities: Participation in global healthcare programs.

- Operational Efficiency Improvements: Margin recovery through better capacity utilization.

Detailed competition analysis for Ipca Laboratories Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Ipca Laboratories Ltd. | 9504.54 | 1923.55 | 20.24% | 947.75 | 9.97% | 42.42 |

| Alkem Laboratories Ltd. | 14252.70 | 2879.11 | 20.20% | 2424.46 | 17.01% | 26.83 |

| Biocon Ltd. | 16827.40 | 3496.00 | 20.78% | 629.60 | 3.74% | 97.86 |

| Glenmark Pharmaceuticals Ltd. | 16468.13 | 4370.84 | 26.54% | 1065.02 | 6.47% | 57.47 |

| Laurus Labs Ltd. | 6721.63 | 1686.20 | 25.09% | 841.81 | 12.52% | 65.80 |

Key insights on Ipca Laboratories Ltd.

- A vertically integrated business model enhances margin control.

- Strong presence in anti-malarial and chronic therapies.

- Balanced revenue mix between domestic and exports.

- API leadership provides competitive advantage.

- Beneficiary of long-term global demand for generic medicines.

Recent financial performance of Ipca Laboratories Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 2245.37 | 2556.50 | 2392.50 | -6.42% | 6.55% |

| EBITDA (₹ Cr.) | 463.08 | 544.92 | 533.35 | -2.12% | 15.17% |

| EBITDA Margin (%) | 20.62% | 21.32% | 22.29% | 97 bps | 167 bps |

| PAT (₹ Cr.) | 277.33 | 283.50 | 364.05 | 28.41% | 31.27% |

| PAT Margin (%) | 12.35% | 11.09% | 15.22% | 413 bps | 287 bps |

| Adjusted EPS (₹) | 9.78 | 11.14 | 12.86 | 15.44% | 31.49% |

Ipca Laboratories Ltd. financial update (Q3 FY26)

Financial performance

- Revenue grew 6.6% YoY to ₹2,392 Cr in Q3FY26, primarily driven by strong performance in formulations.

- EBITDA increased 15% YoY to ₹533 Cr, with margins expanding 167 bps YoY to 22.3%, supported by gross margin improvement.

- PAT rose 31.3% YoY to ₹364 Cr, with margins at 15.2%, aided by operating leverage and better product mix.

- Gross margins improved to 72.5%, reflecting favorable product mix and cost efficiencies.

- Profitability outpaced revenue growth, indicating improving operating efficiency and margin expansion.

Business highlights

- Domestic formulations grew 12% YoY to ₹984 Cr, remaining the key growth driver for the quarter.

- Branded exports surged 28% YoY, while generic exports grew 21% YoY, indicating strong traction across export segments.

- Institutional exports declined 21% YoY, while API business remained flat, acting as near-term drags.

- Improved product mix (higher share of branded formulations) supported margin expansion despite segmental weakness.

- Unichem business faced short-term pressure, but synergy opportunities (API sourcing, front-end integration) provide medium-term upside.

Outlook

- Management expects 10-11% long-term growth across key segments, led by domestic formulations and exports.

- EBITDA margins likely to expand further, with 300 bps improvement potential driven by operating leverage and mix improvement.

- Export formulations expected to remain a key growth lever, supported by traction in branded generics and regulated markets.

- Pipeline commercialization and Unichem integration are expected to drive medium-term growth and profitability.

- Limited capex requirements and strong operational efficiencies position the company for steady and sustainable growth ahead.

Recent Updates on Ipca Laboratories Ltd.

- Focus on resolving regulatory observations at manufacturing facilities.

- Expansion of API and formulation capacities.

- Strengthening presence in international markets.

- Increasing participation in institutional healthcare programs.

- Operational improvements aimed at margin recovery.

Company valuation insights – Ipca Laboratories Ltd.

Ipca Laboratories is currently trading at an EV/EBITDA of 22.7x, after delivering a return of 8.5% over the last one year, outperforming the NIFTY 50 which declined 3.3% during the same period. The premium valuation reflects investor confidence in its strong domestic formulations franchise, improving margins, and recovery in export segments.

The investment case for Ipca Laboratories is supported by its vertically integrated business model, strong presence in domestic formulations, and diversified export portfolio. The company is witnessing robust growth in domestic formulations, particularly in pain management and chronic therapies, while branded exports continue to gain traction. Margin expansion is being driven by an improving product mix, higher share of branded formulations, and operating leverage. Additionally, synergy benefits from the Unichem acquisition, potential regulatory clearances, and steady growth across key geographies provide strong medium-term visibility. With limited capex requirements and strong manufacturing capabilities, Ipca is well positioned to deliver consistent earnings growth.

From a valuation perspective, applying a 16x EV/EBITDA multiple to FY28E estimates, we derive a 12-month target price of ₹1,980, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹1,700, indicating a 6% upside, supported by continued momentum in domestic formulations, margin expansion, and improving export traction.

Major risk factors affecting Ipca Laboratories Ltd.

- Regulatory Risk: USFDA or other regulatory observations impacting exports.

- Pricing Pressure: Competition in global generics markets.

- Dependence on Key Therapies: Concentration in certain therapeutic segments.

- Currency Risk: Exchange rate fluctuations affecting export revenues.

- Execution Risk: Delays in capacity expansion or compliance improvements.

Technical analysis of Ipca Laboratories Ltd. share

Ipca Laboratories is exhibiting strong relative strength amid the broader market correction, with the stock maintaining an uptrend and recently forming a cup and handle pattern, indicating a potential continuation of bullish momentum. A breakout above the neckline suggests the start of a fresh up move.

The stock is currently trading above its 20-, 50-, 100-, and 200-day EMAs, signalling strong structural alignment across multiple timeframes and confirming a sustained uptrend.

Momentum indicators remain supportive of the bullish view. The MACD at 22.94 is in positive territory and has recently crossed above the signal line, indicating strengthening momentum and a fresh entry opportunity. The RSI at 62.16 reflects healthy buying interest without being overbought, while the 21-day and 55-day Relative RSI readings at 0.18 and 0.25 indicate consistent outperformance versus the broader market. Meanwhile, the ADX at 20.45 suggests the trend is strong and still developing.

A sustained move above ₹1,700 could further accelerate the uptrend and open the path toward ₹1,980, aligning with our 12-month fundamental target. On the downside, ₹1,500 remains a key support level, maintaining the bullish structure.

- RSI: 62.16 (Healthy buying interest)

- ADX: 20.45 (Strong trend; developing)

- MACD: 22.94 (Positive; bullish crossover above signal line)

- Resistance: ₹1,700

- Support: ₹1,500

Ipca Laboratories Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹1,700 (6% upside) and a 12-month target of ₹1,980 (24% upside), based on 16x FY28E EV/EBITDA.

Why buy now?

Strong growth visibility in domestic formulations, driven by leadership in pain management and expanding presence in chronic therapies.

Improving product mix (higher share of branded formulations) supporting sustained margin expansion.

Export business recovery led by branded generics and traction in regulated and emerging markets.

Synergy benefits from Unichem acquisition, including API integration and front-end expansion in key geographies.

Vertically integrated business model and limited capex requirements enabling strong cash flow generation and operating efficiency.

Portfolio fit

Ipca Laboratories offers exposure to India’s pharmaceutical growth with a mix of domestic strength and export recovery, making it suitable for portfolios seeking steady earnings growth and margin expansion.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebIpca Laboratories Ltd.: Budget 2026-27 opportunities

- PLI Scheme for Pharma: Incentives for domestic API and formulation manufacturing.

- Healthcare Spending Increase: Boost in domestic demand for medicines.

- Export Promotion Policies: Strengthening India’s position as a global pharma hub.

- API Self-Reliance Push: Reduced dependence on imports supporting domestic manufacturers.

- Public Health Programs Expansion: Increased demand for institutional supply of medicines.

Final thoughts

Ipca Laboratories Limited stands at a crucial juncture, balancing its strong API-driven foundation with opportunities in domestic formulations and global markets. With improving operational efficiency, potential resolution of regulatory concerns, and steady demand across healthcare segments, the company is positioning itself for sustainable growth.

For investors seeking exposure to the pharmaceutical sector with a mix of defensive demand, integration advantages, and turnaround potential, Ipca offers a blend of stability and growth optionality.