Electricity is the backbone of modern economies, powering everything from industry and infrastructure to homes and digital connectivity. In this landscape, Voltamp Transformers Ltd has emerged as one of India’s leading transformer manufacturers, catering to sectors such as power generation, transmission & distribution, and industrial users. With a robust product portfolio spanning distribution, power, and specialty transformers, Voltamp plays a critical role in strengthening India’s grid reliability and supporting the ongoing power sector expansion. Yet, as with all capital goods businesses, demand cycles, raw material costs, and competitive intensity remain key challenges.

But does Voltamp Transformers offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | VOLTAMP |

| Industry/Sector | Heavy Electrical Equipment |

| CMP | 7312 |

| Market Cap (₹ Cr.) | 10,580 |

| P/E( TTM) | 23.00 (Vs Industry P/E of 70.22) |

| 52 W High/Low | 14,280 / 6,051 |

| EPS (TTM) | 321.75 |

About Voltamp Transformers Ltd.

Voltamp Transformers Limited is a company that manufactures oil filled power and distribution transformers, resin impregnated dry type transformers, and cast resin dry type transformers. They cater to government projects, refineries, fertilizer plants, and various industries both in India and internationally. Their product range includes oil-filled transformers, cast resin transformers, sub-stations, and induction furnaces.

Key business segments

Voltamp Transformers Ltd. operates primarily in the following key business segments:

- Power Transformers – Up to 160 MVA, 220 kV; used in utilities, T&D networks, and large industries.

- Distribution Transformers – 25 kVA-3.15 MVA, up to 33 kV; for state utilities and electrification projects.

- Dry-Type Transformers – Cast Resin & VPI; for metros, airports, data centers, hospitals, and commercial use.

- Special Application – Furnace, Rectifier, and customized transformers for steel, cement, chemicals, refineries.

Primary growth factors for Voltamp Transformers Ltd.

Voltamp Transformers key growth drivers:

- Power Demand & Electrification: India’s electricity demand is rising ~6–7% CAGR, with rural electrification and T&D expansion driving transformer needs.

- Policy & Infra Capex: Govt. push via Make in India, PLI, and heavy infra/T&D capex boosts demand across power and manufacturing sectors.

- Industrial Capex: Growing transformer demand from steel, cement, chemicals, data centres, and other power-intensive industries.

- Capacity Expansion: New Jarod plant (~6,000 MVA) enables higher ratings (up to 250 MVA, 220 kV) and supports better utilization and margins.

Detailed competition analysis for Voltamp Transformers Ltd

Key financial metrics – TTM;

| Company | Revenue(₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E (TTM) |

| Voltamp | 1934.23 | 366.22 | 18.93 | 325.41 | 16.82 | 23.00 |

| Shilchar Tech. | 623.15 | 184.75 | 29.65 | 146.85 | 23.57 | 31.38 |

| Bharat Bijlee | 1901.69 | 167.33 | 8.80 | 133.65 | 7.03 | 25.47 |

| TRAIL | 2019.38 | 327.46 | 16.22 | 216.44 | 10.72 | 60.41 |

Key insights on Voltamp Transformers Ltd

- Reputation and Customer Base: Voltamp serves large industrial, utility, and PSU clients; it is trusted by multinational firms (ABB, Siemens, etc.) for high-quality, customized transformers.

- Product Range & Technology: Offers both oil-filled and dry-type transformers, compact substations, RMUs, etc. Dry-type (cast resin) is a niche where it has strong market share.

- Certifications, Quality & After-Sales: Strong focus on quality, testing facilities, services, maintenance, overhauls, spares.

- High Margins & Return Metrics: As noted, ROCE very high; margins improved even as input costs rose. Efficiency improvements are helping.

Recent financial performance of Voltamp Transformers Ltd. for Q1 FY26

| Metric | Q1 FY25 | Q4 FY25 | Q1 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Revenue (₹ Cr.) | 428.15 | 624.81 | 423.58 | -32.21% | -1.07% |

| EBITDA (₹ Cr.) | 75.79 | 116.40 | 72.64 | -37.59% | -4.15% |

| EBITDA Margin (%) | 17.70 | 18.63 | 17.15 | -148 bps | -55 bps |

| PAT (₹ Cr.) | 79.44 | 96.83 | 79.55 | -17.84% | 0.13% |

| PAT Margin (%) | 18.55 | 15.50 | 18.78 | 23 bps | 328 bps |

| Adjusted EPS (₹) | 78.52 | 95.71 | 78.63 | -17.84% | 0.15% |

Voltamp Transformers Ltd. financial update (Q1 FY26)

Financial performance

- Revenue stood at ₹423.6 crore, down ~1% YoY due to lower execution and invoicing delays.

- Profit Before Tax (PBT) grew 3% YoY to ₹104.7 crore, supported by cost discipline and treasury income. Profit After Tax (PAT) was ₹79.6 crore, flat YoY.

- EBITDA margin at ~17.2%, marginally lower than ~17.7% last year, due to lower volumes and fixed cost absorption.

- Maintained consistent dividend payout policy; prior year (FY25) final dividend was ₹100/share (1000% on FV ₹10). FY26 dividend announcement awaited.

Business highlights

- Order Book Growth: Order intake rose 33% in MVA terms and 17% in value terms since April 2025, giving strong revenue visibility of ~₹1,685 crore for FY26.

- Capacity Utilisation: Production impacted temporarily by project delays (solar projects, heavy rains), but management confident of recovering lost ground in H2 FY26.

Outlook

- New Jarod Plant (Gujarat) – progressing to enhance manufacturing capacity up to 250 MVA / 220 kV class; expected to support long-term growth.

- Selective Order Acceptance – company limiting orders with >9-month delivery period to avoid margin erosion from input cost volatility.

Recent Updates on Voltamp Transformers Ltd.

- Capacity Expansion: Ongoing development of the new Jarod plant in Gujarat, which will enhance manufacturing capacity up to 250 MVA, 220 kV class transformers; expected to significantly boost long-term growth and product range.

- Order Book Strength: Robust intake with 33% YoY growth in MVA terms and 17% in value terms; provides strong revenue visibility (~₹1,685 crore for FY26).

- Renewable & Infrastructure Focus: Actively participating in supply for solar, wind, metro, and data center projects, aligning with India’s energy transition and infrastructure expansion.

- Selective Order Policy: Renewed strategy of accepting orders with delivery schedules under 9 months, to safeguard margins against raw material price volatility.

Company valuation insights – Voltamp Transformers Ltd.

Voltamp is currently trading at a TTM P/E of 23x, well below the industry average of 70x, but the stock has corrected sharply with a -45% return over the past year versus the Nifty 50’s -0.5%. The underperformance reflects near-term soft operational performance and capacity constraints.

That said, Voltamp remains a leading transformer manufacturer with a strong balance sheet (zero debt, healthy cash reserves), prudent execution track record, and a solid order book (~₹12,600 Cr, 11,266 MVA). Demand visibility remains strong from utilities, industrial capex, and high-growth segments like renewables and data centers. With its new 6,000 MVA Jarod plant (commissioning in FY27) enabling higher ratings up to 250 MVA, capacity bottlenecks should ease, driving volume growth and margin resilience.

Applying a 21x multiple to FY27E EPS of ₹417, we derive a 12-month target price of ₹8,760, implying ~20% upside from current levels. A shorter-term target of ₹8,000 suggests ~9% upside over the next six months, supported by robust order inflows, sector tailwinds, and capacity expansion visibility.

Major risk factors affecting Voltamp Transformers Ltd.

- Raw Material Price Volatility– Prices are globally linked and highly volatile; sudden spikes can squeeze margins since large transformer contracts are often fixed-price.

- Order Book Execution Risks- Large, long-duration projects carry risk of delays in delivery, site readiness, or approvals (common in power/infra projects).

- Competitive Intensity –Transformer market in India is fragmented with strong domestic peers and global OMEs. Intense price competition may force Voltamp to compromise on margins to get orders.

- Dependence on Power Sector Capex- Demand for transformers is directly tied to government spending on T&D networks, renewable integration, and industrial capex.

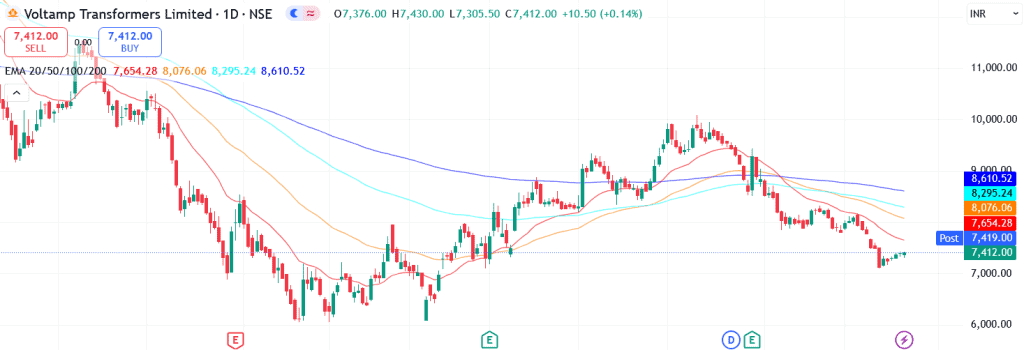

Technical analysis of Voltamp Transformers Ltd. share

Following a prolonged downtrend since July, Voltamp has now approached a key support level, with early signs of reversal emerging, though short-term momentum still looks weak.

The stock is currently trading below its 20-day, 50-day, 100-day, and 200-day EMAs, highlighting near-term weakness. However, with prices nearing the 20-day EMA, a decisive cross above could confirm the reversal trend.

The MACD at -288.4 has just seen the line cross above the signal line, indicating a potential reversal of the downtrend. The RSI at 35.9 suggests the stock is near oversold territory, presenting a possible entry opportunity. Relative RSI values (-0.12 over 21 days, -0.24 over 55 days) reflect slight underperformance against the broader market, though improving momentum could narrow the gap.

A breakout above the ₹8,000 resistance may unlock further upside toward ₹8,760, aligning with its 12-month fundamental target. On the downside, ₹6,800 is a crucial support, holding above this zone will be key for sustaining the bullish reversal setup.

- RSI: 35.9 (Near oversold region)

- MACD: -288.4 (Negative, reversal signal forming)

- Resistance: ₹8,000

- Support: ₹6,800

Voltamp Transformers Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹8000 (9% upside) and a 12-month target of ₹8760 (20% upside).

Why buy now?

Strong near-term revenue visibility order volumes +33% since Apr 2025

The company has delivered high ROCE historically and is essentially debt-free, giving it funding flexibility for capex without heavy leverage.

Capacity additions (higher MVA / 220 kV capability) should let the company take larger/tighter-spec orders and improve economies of scale.

Resilient margins & profitability Q1 FY26 results despite a small revenue dip, showing operational resilience and ability to protect profits.

Portfolio fit

Voltamp is a debt-free transformer leader with a strong order book across utilities and industries. Rising power demand, grid expansion, and industrial capex offer multi-year growth, while the new 6,000 MVA plant boosts scale and margins. It provides clean exposure to India’s power infrastructure growth with financial stability and earnings leverage.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebVoltamp Transformers Ltd.: Budget 2025-26 opportunities

- Higher Allocation to Power and T&D Infrastructure – Budget 2025-26 is emphasized upgrading India’s transmission & distribution (T&D) network to handle renewable integration and reduce losses.

- Renewable Energy Push – Every GW of renewable addition requires significant evacuation infrastructure, including transformers; Voltamp is well positioned to supply to solar parks, wind farms, and green hydrogen projects.

- ‘Make in India’ & Import Substitution- Incentives in the budget to encourage domestic manufacturing of electrical equipment will support local transformer players against imports.

- Data Center & Industrial Capex Boost- Data centers, in particular, need reliable medium- and high-capacity transformers, a fast-growing vertical for Voltamp.

Final thoughts

Picture a growing economy powered by reliable electricity, factories humming, data centers running 24/7, metros and airports expanding, all relying on transformers at the core of the grid. This is where Voltamp fits in. For investors, Voltamp is not just a capital goods stock; it’s a play on India’s rising power demand and infrastructure buildout. While cyclicality in industrial capex is a reality, disciplined investors may find long-term value in Voltamp’s strong balance sheet, capacity expansion, and critical role in India’s electrification journey.