Summary:

This blog explains what Gamma means in options trading and how it tracks the speed at which delta changes when the underlying asset price moves.

It explores how gamma shifts based on option moneyness, the differences between high or low gamma positions, and how traders apply gamma in their strategies.

What Gamma Means in Options

Gamma is one of the Option Greeks, a group of measures that show how sensitive an option’s price is to different market variables. While most beginners start with delta, gamma is what takes your understanding a step further.

Simply put, gamma tells you how much an option’s delta will change when the underlying asset moves by one point. Delta measures how much the option’s price moves with the underlying. Gamma measures how quickly that delta itself is shifting.

For example, if an option has a delta of 0.40 and a gamma of 0.05, a one-point rise in the underlying asset increases the delta to 0.45. This changing sensitivity is what makes gamma important in active trading.

How Gamma Works in Trading

Gamma is not fixed. It responds to price movement, the passage of time, and changes in volatility. Each of these factors pulls gamma in a different direction, and the combined effect is what traders need to stay on top of.

Moneyness drives where gamma is highest

At-the-money (ATM) options carry the most gamma. When an option sits right at the strike price, its delta is most exposed to the next price move and can shift significantly with even a modest change in the underlying.

Deep positions sit at the extremes

Deep in-the-money (ITM) options already have a delta close to 1, so there is not much room left to grow. Deep out-of-the-money (OTM) options have very low delta to begin with, and that delta changes slowly. Both ends carry low gamma for opposite reasons.

Time decay sharpens gamma near expiry

As a contract approaches its expiry, ATM options go through a reactive phase. A small price move in either direction can flip the option from ATM to ITM or OTM in a matter of hours. This is why gamma tends to spike sharply in the final few sessions of a contract.

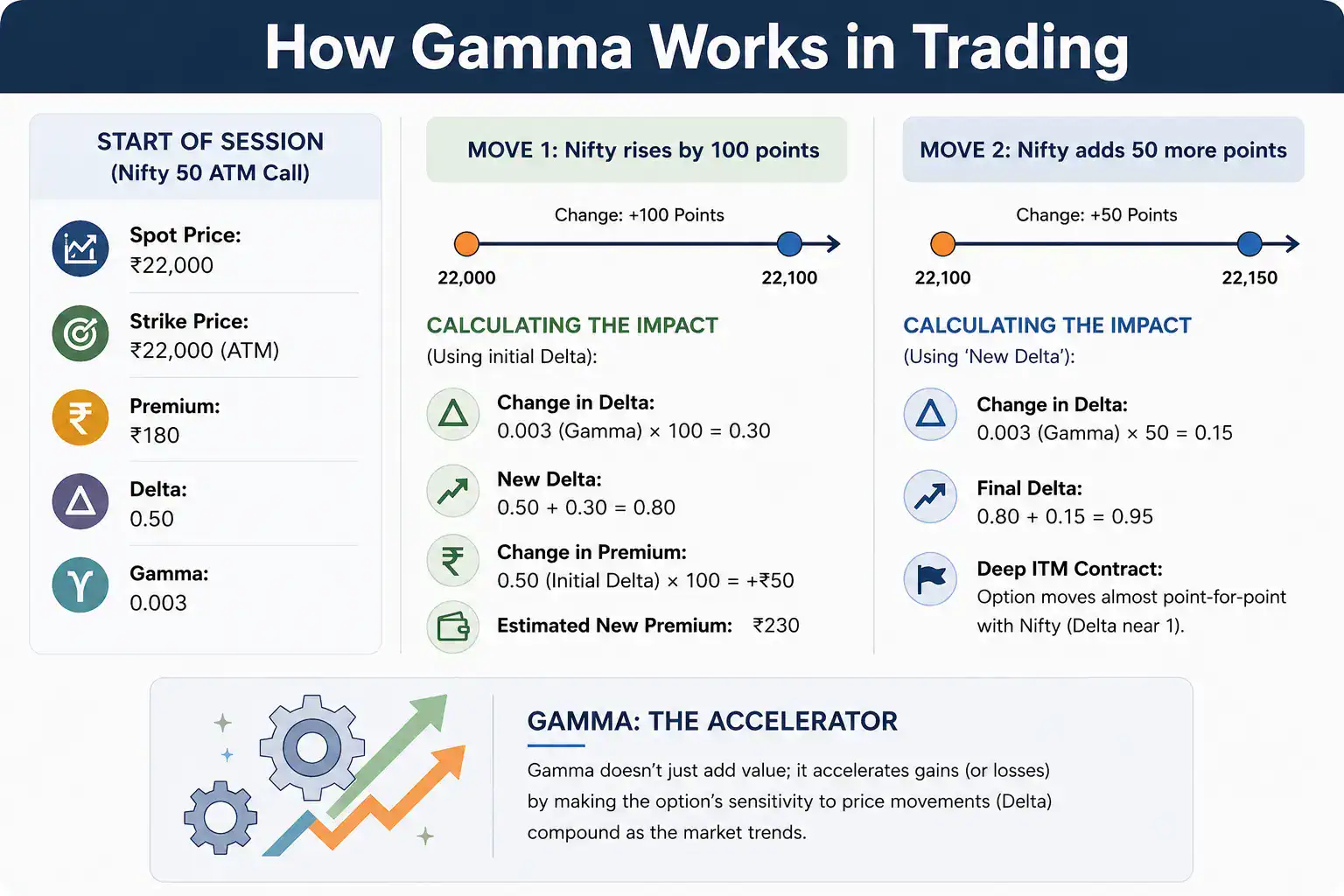

Example: A trader buys a Nifty 50 call option at the start of a session. Nifty is sitting exactly at the strike price of ₹22,000, making it an ATM contract with a premium of ₹180. Delta is 0.50, and gamma is 0.003.

Then Nifty begins to move. It climbs 100 points and settles at 22,100. By this point, the option has quietly transformed. Delta has jumped to 0.80, and the premium has risen to around ₹230. The contract is now responding more like an ITM option, picking up speed with every point Nifty adds.

Nifty is not done. It pushes another 50 points to 22,150. Delta hits 0.95, and the option is now deep ITM, moving almost in lockstep with Nifty. Gamma nudged delta higher with each move until the position was barely recognisable from what it was at entry. Gamma did not simply add value but also accelerated how the position responded with every move.

Why Gamma Matters for Traders

Gamma is not an academic exercise. It has direct implications for how trades are sized, managed, and exited. Here is what it actually means in practice.

- Position exposure

A high-gamma position reacts sharply to price movement. Knowing this before entering a trade helps you size it appropriately and avoid being caught off guard by a position that is suddenly far more sensitive than you expected. - Hedge frequency

For traders using options hedging strategies, gamma determines how often the hedge needs rebalancing. High gamma means the hedge drifts quickly and requires more frequent adjustment. Low gamma gives the hedge more staying power. - Entry timing

Some traders seek out high-gamma options when they expect a strong directional move. Others deliberately avoid them when they want a steadier, more controlled exposure to the underlying asset. - Expiry awareness

In the last few sessions before expiry, gamma for ATM contracts can become exceptionally high. A modest adverse move at this stage can cause the delta to flip sharply, turning a comfortable position into an uncomfortable one very quickly.

Gamma and Delta Relationship

Delta and gamma are connected in a way that is easy to overlook at first. They are not independent numbers; one feeds directly into the other.

When you buy an option, you carry long gamma. Your delta moves in your favour as the underlying trend is in your direction. A call buyer benefits from a rising market not just because the option price increases, but because delta grows along the way, making each additional point gained more valuable than the last.

When you sell an option, the dynamic flips. You carry short gamma, which means delta moves against you as the underlying trends. Option sellers take on this risk knowingly because the premium collected upfront compensates for it, at least in theory.

This push and pull sits at the heart of most serious options trading strategies. A delta-neutral position that looks perfectly balanced at the time of entry will not stay that way when gamma is high. Every price move shifts the delta, and the position has to be adjusted repeatedly to stay neutral.

High Gamma vs Low Gamma

Gamma is not uniform across options, and knowing where yours stands changes how you manage the trade.

| Parameter | High Gamma | Low Gamma |

| Option moneyness | At-the-money | Deep ITM or deep OTM |

| Time to expiry | Near expiry | Far from expiry |

| Delta sensitivity | Reacts sharply to price changes | Changes gradually |

| Risk level | Higher short-term uncertainty | More stable and predictable |

| Best suited for | Directional and momentum traders | Hedgers and premium sellers |

- Option moneyness: ATM options carry the highest gamma because delta is most uncertain at the strike price. Move too far in either direction and gamma drops, as deep ITM and deep OTM outcomes are far more predictable.

- Time to expiry: Far-dated contracts have more time cushion, which keeps gamma relatively subdued. As the contract shortens toward expiry, ATM gamma can climb steeply in a short period.

- Delta sensitivity: High gamma translates to a delta that is constantly adjusting, demanding active awareness. Low gamma moves more gradually, making it easier to monitor without needing to check in as frequently.

- Risk level: High gamma brings more short-term volatility as delta can swing noticeably with each price move. Low gamma stays relatively stable, suiting traders who prefer to keep things quieter.

- Best suited for: Traders expecting a sharp directional move naturally gravitate toward high gamma options. Those focused on options risk management or running income strategies tend to prefer lower gamma profiles.

How Traders Use Gamma

Gamma feeds into trading decisions at multiple levels, from position sizing all the way to portfolio-level risk management.

- Scalping through delta adjustments

Gamma scalping involves maintaining a delta-neutral position and rebalancing it repeatedly as the underlying moves. Each adjustment captures a small gain. Individually modest, these gains can add up meaningfully over a volatile session. - Preparing for event risk

Before a high-impact event, traders check their gamma exposure carefully. A position with large gamma ahead of a surprise can swing a portfolio sharply. Some trim it down beforehand; others increase it if they have a strong directional view. - Choosing strikes based on the gamma profile

Traders do not always pick a strike based on price target alone. An ATM strike gives maximum sensitivity for those expecting a strong move. A slightly OTM strike suits those who want a more measured response. - Net gamma across positions

When running multiple positions, net gamma tells you whether large moves help or hurt the book overall. A net long-gamma position benefits from volatility. A net short-gamma position prefers calmer conditions. Understanding options trading basics includes knowing which environment your book is suited for.

Final Takeaway for Beginners

Gamma sounds intimidating, but it really just tells you how alive your delta is. Start by watching how the delta shifts as the underlying moves. Over time, you will develop a feel for when the gamma is working in your favour. Simply begin and track it consistently.

FAQs

Gamma is neither good nor bad. It increases responsiveness in options positions, which can amplify both profits and losses depending on market direction.

High gamma means delta changes rapidly when the underlying asset moves, making the option price more sensitive to market movement.

Gamma is usually highest in ATM options, especially when expiry is close, and price sensitivity increases sharply, which is why this period deserves closer attention.

Traders use gamma to monitor delta movement, manage hedges, adjust positions, and understand how options may react during volatility.

Not at all. Understanding gamma helps even beginners because it explains why option prices can react more quickly and supports better decision-making.