Every few years, a financial product gets labelled the sensible choice for everyday investors. Right now, ETF stocks hold that title and for good reason. Assets under management in global ETFs crossed $14 trillion in 2024, reflecting a decade-long shift away from expensive actively managed funds toward low-cost, transparent, index-tracking alternatives. India’s mutual fund industry AUM rose 12.2% to approximately $790 billion in FY26, with non-gold ETF inflows alone jumping 4.4x month-on-month to ₹19,802 crore in March 2026, per AMFI data. But popularity is not the same as suitability. Whether or not, are ETFs a good investment depends entirely on what you’re investing for, how long you’re staying in, and whether you understand what you’re actually buying.

Are ETFs a Good Investment?

For most long-term investors, yes. But that answer needs details, not just a short description.

ETFs mutual funds are genuinely well-suited for investors who want broad market exposure without paying high fund management fees, without needing to pick individual stocks, and without committing to the lock-in structures or entry loads that some mutual funds carry. For someone investing consistently over 10, 15, or 20 years, the combination of low costs, built-in diversification, and market-linked returns makes ETFs one of the most efficient wealth-building vehicles available to retail investors today.

That said, ETFs are not a guaranteed return product. They track indices which means when markets fall, ETF values fall with them. They don’t outperform the market; they replicate it. For investors chasing alpha or looking for short-term gains, ETFs are structurally the wrong tool. And for those who don’t understand what index they’re buying into or how the fund is structured, ETFs carry risks that aren’t immediately obvious from the surface-level simplicity they’re often marketed with.

The honest answer: ETFs are a good investment for patient, informed, cost-conscious investors with a long timeline. They are not a shortcut, not a guaranteed wealth creator, and not suitable as a standalone solution for every financial goal.

What Are ETFs and How Do They Work?

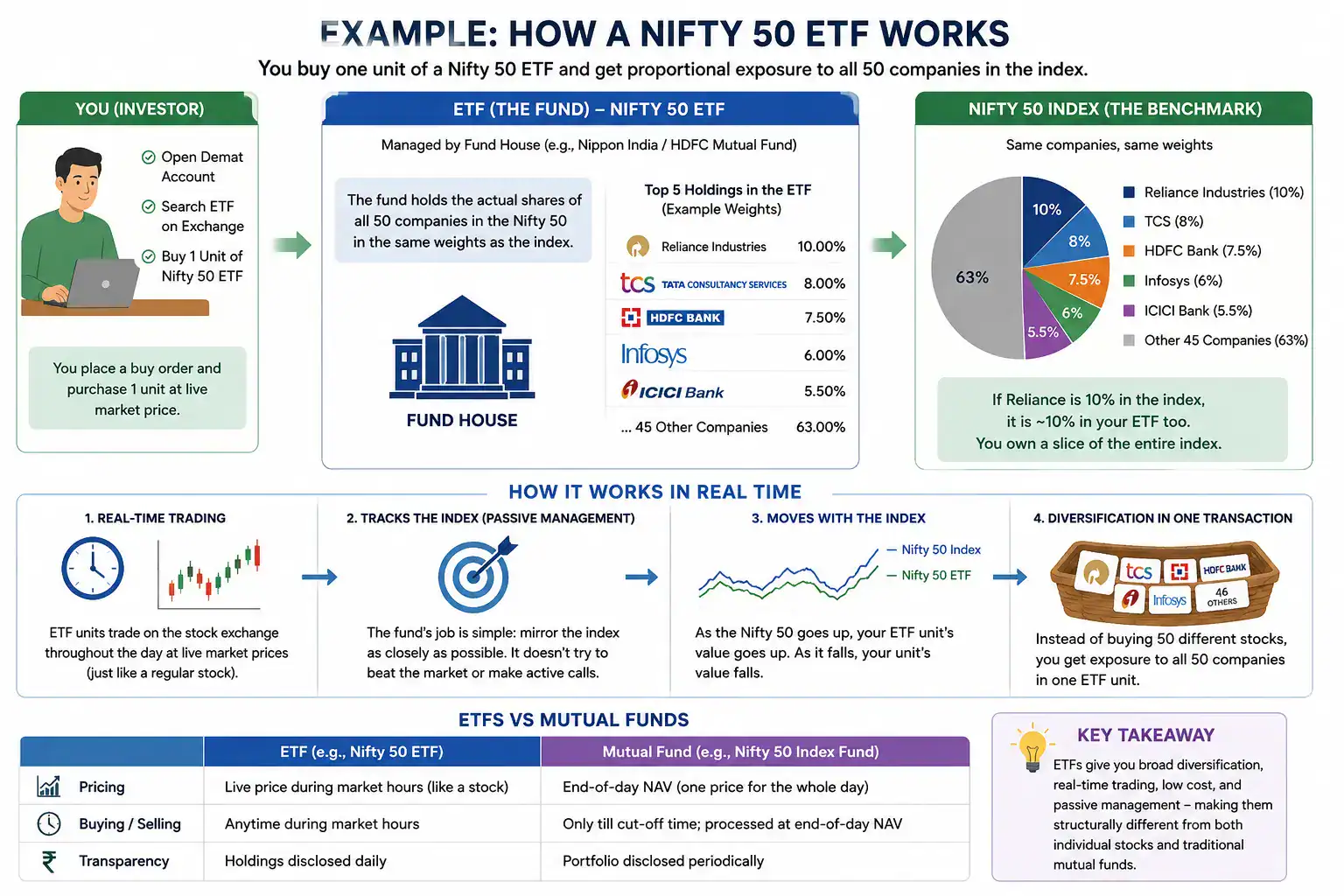

An Exchange Traded Fund (ETF) is essentially a ready-made portfolio of investments packaged into a single tradable unit that moves on the stock exchange the same way ordinary shares do. You buy and sell it through your Demat account at live market prices, just as you would buy a share of Reliance or Infosys.

The simplest way to understand how it works is through an example.

Say you want to invest in the top 50 companies in India but you don’t have the capital or time to buy shares in all 50 individually. A Nifty 50 ETF solves that problem in one transaction. When you buy one unit of a Nifty 50 ETF, you’re automatically getting proportional exposure to all 50 companies in the index: Reliance, TCS, HDFC Bank, Infosys, and 46 others in the exact same weights they carry in the index.

If Reliance constitutes 10% of the Nifty 50, it makes up roughly 10% of your ETF unit. If TCS is 8%, your ETF reflects that too. You own a slice of the entire index, not a single company.

Now here’s the working part. The ETF is managed by a fund house say Nippon India or HDFC Mutual Fund. They hold the actual shares of all 50 companies in a fund. When you buy an ETF unit, you’re buying into that fund. The fund’s job is simple: mirror the index as closely as possible. It doesn’t try to beat the market or make active calls, it just tracks it. That’s why ETFs are called passively managed funds.

As the Nifty 50 goes up, your ETF unit’s value goes up. As it falls, your unit’s value falls. The price of your ETF unit moves throughout the trading day in real time unlike a mutual fund, where you only get the end-of-day NAV regardless of when you placed your order.

This combination of broad diversification, real-time trading, and passive management is what makes ETFs structurally different from both individual stocks and traditional mutual funds.

Benefits of Investing in ETFs

ETFs provide several practical advantages that make them different from many traditional investment products, which include the following:

- Exposure to an entire market through one transaction: Instead of selecting multiple individual stocks, investors can access an entire index, sector, or asset class with a single ETF unit. For example, buying a Nifty 50 ETF gives exposure to companies across banking, IT, energy, FMCG, telecom, and automobile sectors together.

- Suitable for different investment strategies: ETFs can be used for long-term investing, short-term market exposure, sector allocation, or portfolio balancing depending on the type of ETF selected.

- No dependency on fund manager stock-picking decisions: Since index ETFs follow predefined benchmarks, returns are generally linked to index performance rather than individual fund manager calls. This reduces fund-manager-specific risk that may arise from wrong stock selection or allocation decisions.

- Live market pricing during trading hours: ETF units trade on exchanges like stocks, allowing investors to buy or sell during market hours instead of waiting for end-of-day NAV processing. This becomes useful during volatile sessions where prices move significantly within the same day.

- Useful for accessing difficult or expensive asset classes: ETFs make it easier to invest in segments that may otherwise require higher capital or operational effort. Gold ETFs, for instance, allow gold exposure without locker charges, purity concerns, or making charges associated with physical gold purchases.

- Tax efficiency in certain structures: Many ETFs are considered relatively tax-efficient because portfolio turnover is usually lower than actively managed funds.

Risks & Limitations of ETFs

ETFs also carry certain structural and market-related limitations that investors should understand, which include the following:

- ETF prices may differ from actual portfolio value

ETF market prices can temporarily trade above or below their actual NAV because prices depend on exchange demand and supply. For example, several international ETFs in India traded at unusually high premiums after overseas investment limits were temporarily exhausted, causing ETF prices to move significantly above underlying portfolio value. - Low liquidity may create pricing inefficiencies: ETFs with lower trading volume can have wider bid-ask spreads, making buying and selling less efficient. In some cases, investors may end up paying more than the actual value of the ETF holdings. For instance, certain global ETFs in India traded at premiums of nearly 20–25% above their actual NAV because fresh unit creation was restricted while investor demand remained high.

- Trading-related costs can reduce cost advantage: Although ETFs generally have lower expense ratios, investors may still incur brokerage charges, bid-ask spread costs, STT, and exchange-related charges on every transaction. Frequent trading can therefore reduce the overall cost benefit.

- Returns still depend on market performance: ETFs do not protect investors from market declines because they generally move along with the assets they track. An example of this is during major market corrections, Nifty and Sensex ETFs also recorded declines alongside the broader equity market because the underlying stocks themselves fell in value.

ETFs vs Stocks vs Mutual Funds

The major differences between ETFs, stocks, and mutual funds are as follows:

| Basis of comparison | ETFs | Stocks | Mutual funds |

| Meaning | Exchange Traded Funds pool money and invest in a basket of securities that usually track an index, sector, commodity, or asset class. | Stocks represent ownership in a single listed company. | Mutual funds pool investor money and invest across securities based on a specific investment objective. |

| Ownership exposure | Exposure to multiple securities through one investment. | Exposure to one company only. | Exposure to multiple securities through a professionally managed portfolio. |

| Trading method | Bought and sold on stock exchanges throughout market hours. | Bought and sold on stock exchanges throughout market hours. | Purchased or redeemed directly through AMC at end-of-day NAV. |

| Pricing | Prices change continuously during market hours based on demand and supply. | Prices fluctuate continuously during market hours. | Transactions happen at the closing NAV calculated after market hours. |

| Diversification level | Generally diversified because one ETF may hold many securities. | No diversification unless multiple stocks are purchased separately. | Usually diversified across several securities. |

| Fund management style | Mostly passively managed and benchmark-linked. | Self-managed by the investor. | Can be actively or passively managed. |

| Expense ratio | Usually lower because most ETFs track indices. | No expense ratio, but brokerage and trading costs apply. | Active mutual funds generally have higher expense ratios. |

| Liquidity | Depends on exchange trading volume and market makers. | Liquidity depends on the company’s trading activity. | Redemption is handled directly by the fund house. |

| Transparency | Holdings are generally disclosed frequently. | Investors directly know which company shares they hold. | Portfolio disclosures are periodic rather than live. |

| Intraday tradinv | Allowed. | Allowed. | Not available because pricing is NAV-based. |

| Dividend handling | Dividends may be distributed or reinvested depending on ETF structure. | Dividends are received directly from the company if declared. | Dividends depend on the mutual fund payout option selected. |

How to Invest in ETFs (Step-by-Step Guide)

The process of investing in ETFs generally involves the following steps:

- Open a demat and trading account

ETFs are traded on stock exchanges like regular shares, so investors usually need both a demat account and a trading account with a broker registered with NSE or BSE. Without these accounts, exchange-based ETF transactions cannot be executed.

- Complete KYC verification

PAN, Aadhaar, address proof, bank details, and IPV verification are generally required before trading access is activated. Most brokers now offer fully digital onboarding processes.

- Identify the type of ETF required

Investors should first decide what exposure they want instead of selecting randomly. For example:

- Broad market exposure through Nifty or Sensex ETFs

- Gold exposure through Gold ETFs

- International exposure through Nasdaq or US-focused ETFs

- Debt exposure through Bond or Gilt ETFs

- Sector exposure through Banking or IT ETFs

- Compare important ETF metrics before investing

Instead of selecting only based on past returns, investors usually compare operational factors such as:

- Expense ratio

- Average daily trading volume

- Assets under management (AUM)

- Tracking error

- Bid-ask spread

- Liquidity on exchanges

- Search the ETF on the exchange platform

ETFs trade using ticker symbols similar to stocks. For example, investors may search using symbols like NIFTYBEES, GOLDBEES, or BANKBEES depending on the ETF selected.

- Place a buy order carefully

Investors can place either a market order or a limit order. In ETFs with lower liquidity, limit orders are often preferred because they allow investors to specify the maximum purchase price instead of buying at an unfavourable spread-driven price.

- Check ETF price against NAV before execution

ETF market price can sometimes differ slightly from actual NAV. Investors often compare the live trading price with indicative NAV to avoid purchasing units at a significant premium.

- Monitor liquidity after investing

ETF performance alone is not the only factor to monitor. Trading volumes, spreads, benchmark tracking, and fund size are also important because low participation can affect future liquidity and pricing efficiency.

- Review taxation and holding structure

Tax treatment may vary depending on whether the ETF is equity-oriented, gold-based, or debt-oriented. Investors therefore usually review capital gains rules and holding periods before investing.

- Use SIP-style investing if investing regularly

Some brokers allow scheduled ETF purchases similar to SIPs. This helps investors gradually accumulate units over time instead of investing a lump sum in a single transaction.

Final Thoughts

ETFs work best when the investor behind them is patient, consistent, and clear on what they’re buying. Low fees, broad diversification, and market-linked returns make them one of the more dependable building blocks for long-term wealth. But they are a tool, not a promise. Knowing are ETFs a good investment all in all comes down to one thing, if the person holding them has the discipline to stay invested long enough for the compounding to do its job.

FAQs

Yes, ETFs can lose value because their prices move according to the underlying assets they track. If the market, sector, or index declines, the ETF value may also decline accordingly.

ETFs may suit investors seeking lower costs, real-time trading, and passive investing, while mutual funds may suit investors preferring professional active management, SIP convenience, and no exchange-based trading requirements.

Yes, ETFs are commonly used for long-term wealth creation because they provide diversified market exposure, lower expense ratios, and access to broad indices that historically participated in long-term market growth.

Some ETFs distribute income through dividends or interest payouts depending on their holdings. Equity ETFs may pass company dividends, while bond ETFs may distribute interest income from underlying debt securities.