In a world increasingly focused on pharmaceutical resilience, supply chain de-risking, and complex molecule production, Divi’s Laboratories has quietly built a global reputation. With a focus on chemistry excellence, high compliance, and cost efficiency, Divi’s is more than just another pharma company – it’s a trusted backend partner to some of the world’s largest innovators. While not flashy, it has built a business that compounds slowly and consistently, with high margins, strong return ratios, and minimal debt.

But does Divi’s Laboratories offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | DIVISLAB |

| Industry/Sector | Healthcare (Pharmaceuticals & Drugs) |

| CMP | 6707.50 |

| Market Cap (₹ Cr.) | 1,78,076 |

| P/E | 80.67 (Vs Industry P/E of 34.80) |

| 52 W High/Low | 6,862.50 / 4,395.30 |

| EPS (TTM) | 82.53 |

| Dividend Yield | 0.45% |

About Divi’s Laboratories

Founded in 1990 by Dr. Murali Divi, Divi’s Laboratories Ltd. is a Hyderabad-based pharmaceutical company that specializes in Active Pharmaceutical Ingredients (APIs), Intermediates, and Custom Synthesis for global pharma and nutraceutical majors. Over the past three decades, Divi’s has become a global leader in generic APIs and a preferred partner for contract manufacturing, particularly in high-value, complex molecules.

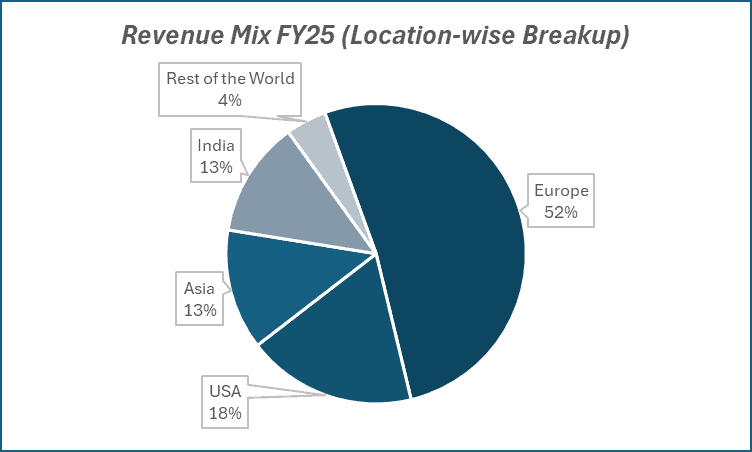

With four manufacturing facilities and multiple R&D centers, Divi’s serves over 95 countries, supplying to both regulated (US, EU) and semi-regulated markets.

Key business segments

Divi’s Laboratories operates primarily in the following key business segments:

- Generic APIs – Manufacturing and sale of APIs for off-patent drugs across therapeutic categories like pain management, cardiovascular, and anti-inflammatory.

- Custom Synthesis (CDMO) – Long-term contract manufacturing and development partnerships with global innovators for patented molecules.

- Nutraceuticals – Production of carotenoids, vitamins, and mineral ingredients used in food and wellness products.

Primary growth factors for Divi’s Laboratories

Divi’s Laboratories key growth drivers:

- Global Pharma Outsourcing: Rising cost and compliance pressures in the West drive outsourcing to low-cost, high-quality players like Divi’s.

- China+1 Strategy: Global clients reducing dependence on Chinese suppliers, improving India’s relevance.

- Capacity Expansion: Ongoing greenfield and brownfield expansions to support higher demand and complex synthesis.

- High Entry Barriers: Regulatory compliance, IP respect, and chemistry depth make Divi’s a preferred partner with limited competition.

- Nutraceutical Tailwinds: Growing global demand for wellness and preventive health supports revenue growth from this segment.

Detailed competition analysis for Divi’s Laboratories

Key financial metrics – FY25;

| Company | Revenue(₹ Cr.) | R&D as a % of Sales (%) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E (TTM) |

| Divi’s Laboratories | 9360.00 | 0.9% | 31.71% | 2191.00 | 23.41% | 80.67 |

| Sun Pharmaceutical | 52578.44 | 6.3% | 28.69% | 10980.10 | 20.88% | 37.06 |

| Cipla Ltd. | 27547.62 | 6.3% | 25.87% | 5291.05 | 19.21% | 23.02 |

| Torrent Pharma | 11516.00 | 5.1% | 32.31% | 1911.00 | 16.59% | 59.22 |

| Dr. Reddy’s Lab | 32643.90 | 8.5% | 26.18% | 5703.50 | 17.47% | 19.20 |

Key insights on Divi’s Laboratories

- Divi’s has delivered a 5-year sales CAGR of 12%, with 60–65% revenue from exports, offering natural hedging and global diversification.

- It enjoys EBITDA margins of ~30–35%, driven by in-house R&D and scale efficiencies.

- Profit CAGR of 10% over 5 years reflects steady demand and margin stability.

- A debt-free balance sheet and strong free cash flows highlight financial strength.

- Repeat business and long-term CDMO contracts ensure visibility and customer stickiness.

- A clean regulatory track record enables consistent business from US/EU markets.

Recent financial performance of Divi’s Laboratories for Q4 FY25

| Metric | Q4 FY24 | Q3 FY25 | Q4 FY25 | QoQ Growth (%) | YoY Growth (%) |

| Revenue (₹ Cr.) | 2303.00 | 2319.00 | 2585.00 | 11.47% | 12.24% |

| EBITDA (₹ Cr.) | 731.00 | 743.00 | 886.00 | 19.25% | 21.20% |

| EBITDA Margin (%) | 31.74% | 32.04% | 34.27% | 223 bps | 253 bps |

| PAT (₹ Cr.) | 538.00 | 589.00 | 662.00 | 12.39% | 23.05% |

| PAT Margin (%) | 23.36% | 25.40% | 25.61% | 21 bps | 225 bps |

| Adjusted EPS (₹) | 20.30 | 22.23 | 24.98 | 12.37% | 23.05% |

Divi’s Laboratories financial update (Q4 FY25)

Financial performance

- Q4 FY25 revenue at ₹2,585 cr, up 12.2% YoY; FY25 revenue ₹9,360 cr, up 19.3% YoY.

- Q4 FY25 net profit ₹662 cr, up 23% YoY; FY25 PAT ₹2,191 cr, up 37% YoY.

- Material consumption steady at ~40% of revenue; Q4 forex gain of ~₹10 cr vs. ₹2 cr loss in Q4 FY24; FY25 forex gain ₹48 cr vs. ₹30 cr in FY24.

- Standalone liquidity as of Mar 31, 2025: cash on books ₹3,696 cr; receivables ₹2,855 cr; inventories ₹3,033 cr.

Business highlights

- Generics portfolio faced pricing pressures but volumes remained stable; leadership maintained through process innovation and capacity building.

- Custom synthesis/CDMO momentum strong: healthy uptick in RFQs, long‑term agreement inked with a global pharma player (revenues to kick in from Q3/Q4 FY26).

- Peptide segment gaining traction (GLP‑1, GIP, GLP‑2 analogs); investments in both solid‑ and liquid‑phase synthesis underway.

- Contrast medium project showing steady progress, enhancing capabilities in a high‑growth niche.

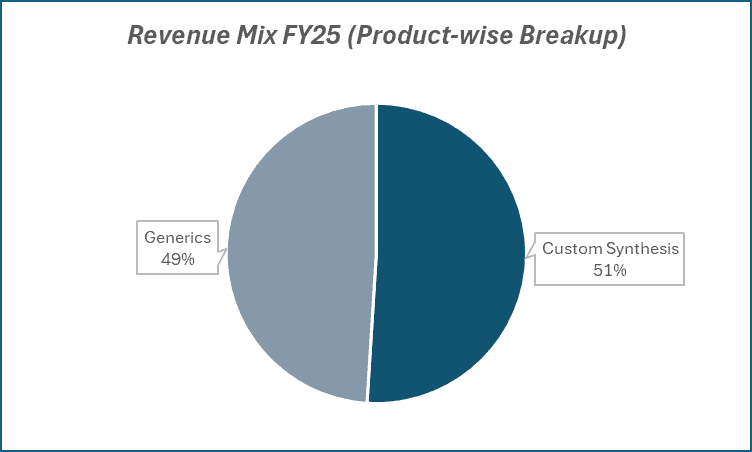

- Exports constituted 87% of FY25 revenues (70% to US/EU); product mix: generics 49%, custom synthesis 51%; nutraceuticals ₹781 cr in FY25 (₹205 cr in Q4).

Outlook

- Double‑digit revenue growth guidance ahead.

- FY26 capex pegged at ~₹1,400 cr (including maintenance).

- Kakinada integration to drive backward integration, raw‑material security and margin expansion.

- 300 acres land bank at Kakinada for phased capacity expansion.

Recent Updates on Divi’s Laboratories

- Expansion momentum and capex: The greenfield Unit III at Kakinada began commercial operations in Q4, and FY26 capex guidance is ₹1,400 cr to support backward integration and capacity ramp-up .

- Strategic Long term deal: In April, Divi’s signed a long-term supply deal with a global pharma player, boosting the stock ~3.5%. Production begins by Jan 2027, with ₹650–750 cr capex planned.

Company valuation insights – Divi’s Laboratories

Divi’s Laboratories is trading at a rich TTM P/E of 80.7x, well above the industry average of 34.8x, yet has still delivered a 46.7% return over the last 12 months versus the Nifty 50’s 6.0%, reflecting its strong growth and premium positioning.

The stock’s valuation premium is underpinned by sustained EBITDA margin expansion, debt‑free balance sheet, and a robust CDMO order book that drives double‑digit revenue and profit CAGRs.

Applying a 65× multiple to our FY27E EPS of ₹128 yields a 12‑month target price of ₹8,320 (≈ 23% upside) and, for a shorter 3‑month horizon, a target of ₹7,400 (≈ 10% upside), offering a compelling risk‑reward given its earnings visibility and operating leverage.

Major risk factors affecting Divi’s Laboratories

- Client Concentration: A few key clients account for a large share of revenues, making Divi’s vulnerable to strategic shifts.

- Regulatory Risk: Any adverse US FDA or EU inspection could disrupt operations or impact credibility.

- Raw Material Dependence: Although insulated compared to others, supply chain shocks or input cost volatility can affect gross margins.

- Slower New Projects: Delay in onboarding new CDMO molecules or generic launches can slow growth temporarily.

Technical analysis of Divi’s Laboratories share

Divi’s Laboratories is displaying early signs of a bullish reversal, having broken out of a six-month sideways channel (Oct ’24–Apr ’25) with a strong 7% rally since mid-May. This breakout, coming amid broader market consolidation, reflects Divi’s defensive strength and signals renewed momentum.

The stock now trades well above its 50-day, 100-day, and 200-day EMAs, confirming the resumption of a long-term uptrend. The MACD is positive at 57.84, and a pending bullish crossover suggests further upside potential.

The RSI at 57.57 signals healthy buying interest, while Relative RSI readings of -0.03 (21-day) and 0.09 (55-day) indicate longer-term outperformance. An ADX of 19.26 shows a trend gaining strength.

A break above ₹7,400 resistance could pave the way toward the ₹8,320 target, while ₹6,240 remains the key support for trend confirmation.

- RSI: 57.57 (Decent Buying Interest)

- ADX: 19.26 (Developing Trend)

- MACD: 57.84 (Positive, bullish crossover pending)

- Resistance: ₹7,400

- Support: ₹6,240

Divi’s Laboratories stock recommendation

Current Stance: Buy, with a 3-month target of ₹7,400 (~10% upside) and a 12-month target of ₹8,320 (~23% upside) based on 65× our FY27E EPS estimate of ₹128.

Why buy now?

CDMO Momentum: Strong order pipeline and a long-term supply deal with a global pharma major enhance visibility and earnings stability.

Margin Leadership: Sustained EBITDA margins of ~30–35%, supported by process innovation, backward integration, and scale efficiencies.

Diversified Revenue Mix: Balanced exposure across generics, custom synthesis, nutraceuticals, and growing traction in peptides and contrast media.

Portfolio fit

Divi’s Laboratories offers a high-quality, global pharma outsourcing play with a clean regulatory track record, robust free cash flows, and zero long-term debt. Its leadership in APIs and strategic investments in capacity and innovation make it a strong fit for investors seeking exposure to the global healthcare supply chain and long-term defensiveness.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebDivi’s Laboratories: Budget 2025-26 opportunities

- PLI & API Support: Extended incentives under the PLI scheme aid Divi’s backward integration and API strength.

- Export Boost: Policy push for pharma exports benefits Divi’s 88% export-driven revenue mix.

- R&D Incentives: Increased allocation for pharma innovation supports Divi’s focus on peptides and contrast media.

- CDMO Growth: Government backing for India’s CDMO sector aligns with Divi’s clean regulatory record and global client base.

- Infra Push: Logistics and port upgrades improve export efficiency for global pharma suppliers like Divi’s.

Final thoughts

Divi’s Laboratories represents a rare combination of global scale, domestic trust, and long-term stability in the pharmaceutical manufacturing world. It doesn’t chase flashy launches or aggressive M&A – instead, it wins with quiet execution, chemistry excellence, and financial prudence.

For investors, Divi’s offers a defensive compounding story in the CDMO and API space with structural global tailwinds, strong cash flows, and a track record of navigating regulatory and macro challenges. If you’re looking for quality pharma exposure with high visibility and low volatility, Divi’s deserves a place on your radar – and possibly in your core portfolio.