You see the announcement, your share count jumps, the price drops, and nothing seems to have changed. That is exactly why bonus shares and stock splits get confused so often. Both produce more shares at a lower price, but they are built on entirely different logic. The mechanics, the accounting, and the tax treatment differ. This guide cuts through the surface and lays out what each action actually means for you.

What Are Bonus Shares?

Bonus shares are extra shares issued by the company to existing shareholders at no cost. The company converts its accumulated profits or free reserves into equity and hands them out to shareholders in a fixed ratio.

For instance, in a 1:1 bonus issue, a shareholder with 100 shares will receive 100 additional shares. He will end up with 200 shares total. The total investment value stays the same since the share price adjusts downward proportionally.

What Is A Stock Split?

A stock split is when a company divides its existing shares into multiple smaller units by reducing the face value proportionally. No new shares are actually created from reserves. The existing shares are simply subdivided.

In a stock split of 1:2, one share with a face value of ₹10 becomes two shares of face value ₹5 each. The total market capitalisation of the company remains exactly the same because the price per share halves as the number of shares doubles.

Bonus Share vs Stock Split

Here is a quick side-by-side look at the differences before we go deeper into each one.

| Parameter | Bonus Shares | Stock Split |

| Share Price | Share price gets diluted | Repriced proportionally after division |

| Number of Shares | New shares added | Existing shares divided, none created |

| Company Reserves | Transferred to equity capital | Remain unchanged |

| Accounting Entry | Reserves moved to share capital | Only face value restated |

Breaking down each parameter:

- Share Price: Both actions bring the price down, but for different reasons. A bonus issue dilutes the price because new shares enter the pool. A split corrects the price because each existing share is subdivided.

- Number of shares: A bonus issue adds entirely new shares to the outstanding pool, drawn from reserves. A stock split increases the count by dividing what already exists; no new shares are created or issued.

- Company Reserves: A bonus issue permanently transfers money from reserves to paid-up capital. A stock split changes nothing in that column.

- Accounting Entry: In a bonus issue, reserves are debited, and share capital is credited. A stock split requires no such journal entry; only the face value and share count are restated.

Difference Between Bonus Shares and Stock Split

The headline numbers look alike. The mechanics beneath them do not.

Impact on Share Price

After a bonus issue, the share price adjusts on the ex-bonus date in proportion to the ratio. It reduces the price because the outstanding shares increase, but the total market value stays unchanged.

In a stock split, the same price correction happens, but it is only a mechanical restatement. No new value is created or destroyed.

Impact on Number of Shares

Bonus shares add new shares to the outstanding pool. A 1:2 bonus on 100 shares creates 100 new shares from reserves; you hold 200.

A stock split produces the same count through division, not creation. Each existing share breaks into smaller units. A 1:2 split on 100 shares also gives 200, but nothing new was issued.

Impact on Company Reserves

A bonus issue pulls directly from free reserves. Once that amount is capitalised, it moves permanently into paid-up share capital and is no longer available to be paid out as a future dividend.

A stock split changes nothing on the reserves side. Before and after, the number looks identical, only the face value and share count columns shift.

Accounting Treatment Difference

In a bonus issue, reserves are debited and paid-up share capital is credited by the same amount. Net worth holds steady, but equity composition changes.

In a stock split, there is no debit or credit between reserves and capital. The company simply restates the face value and adjusts the share count to match.

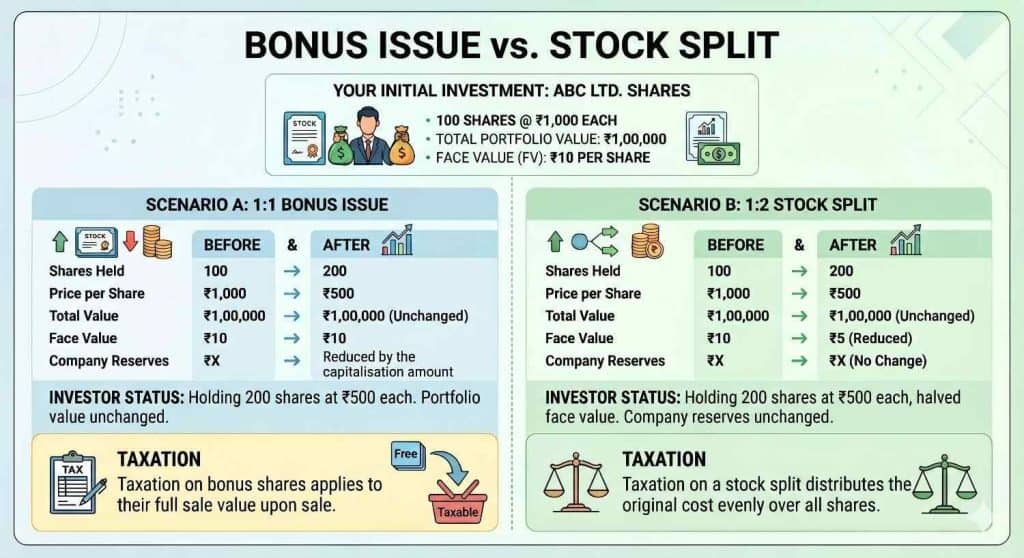

Bonus Share vs Stock Split Example

You hold 100 shares of ABC Ltd. at ₹1,000 each. Total value: ₹1,00,000. Face value: ₹10 per share.

Scenario A: 1:1 Bonus Issue

Starting with 100 shares at ₹1,000 each, a 1:1 bonus doubles your holding. You now hold 200 shares at ₹500. Portfolio value is unchanged, but the company has permanently moved a portion of its retained earnings into paid-up share capital.

The tax catch: original 100 shares carry a cost of ₹1,000 each, but the 100 bonus shares have zero acquisition cost. When you sell, that entire sale value of the bonus shares is taxable as capital gains.

Scenario B: 1:2 Stock Split

Same starting point: 100 shares at ₹1,000. After the 1:2 split, you hold 200 shares at ₹500, and the total value stays at ₹1,00,000. The difference is in the detail: face value drops from ₹10 to ₹5, and the company’s reserves remain completely untouched.

The tax treatment is simpler: the original ₹1,00,000 cost spreads evenly across all 200 shares. No zero-cost shares, no asymmetric tax liability. Holding period runs from the original purchase date with no reset.

The share count and price look identical in both cases. The face value, the reserves, and the tax treatment tell a very different story.

Why Companies Issue Bonus Shares

A bonus issue is rarely random. It points to a deliberate action by the company.

- Rewarding without cash: Instead of receiving dividends, shareholders get more shares, and the company keeps its liquid reserves available for operations or expansion.

- Signalling reserve strength: Issuing bonus shares tells the market that profits have been quietly building. It is a confidence signal.

- Improving stock liquidity: Lower per-share prices after a bonus issue typically draw more retail participation and trading activity.

- Strengthening the equity base: Transferring accumulated profits to paid-up capital restructures the balance sheet in an organised way.

Why Companies Do A Stock Split

A stock split is generally a price-driven decision, though it carries its own strategic weight.

- Making shares accessible: When a stock trades at several thousand rupees, many retail investors cannot afford even a single unit. A split solves that.

- Lifting trading volumes: More affordable shares invite more buyers and sellers, which improves the participation levels and enhances market depth.

- No balance sheet cost: Reserves stay untouched. It is a clean action with zero financial disruption.

- A sign of past appreciation: Companies rarely split unless the price has run up considerably, which itself communicates conviction about the stock’s journey.

Bonus Shares vs Stock Split: Which Is Better for Investors?

There is no universal winner here. Portfolio value does not increase on announcement day in either case.

Bonus shares carry a stronger signal – they reflect accumulated earnings. The downside is the zero acquisition cost on those extra shares, which creates a heavier tax burden at the time of sale.

Stock splits are cleaner from a tax angle and tend to lift liquidity more immediately. The company does not spend anything, and your cost basis simply gets redistributed.

What matters most is the business behind the announcement. A strong company rewards you either way. A weak one does not become stronger by splitting or issuing a bonus.

Advantages of Bonus Shares

Bonus shares come with some clear benefits for investors who understand how they work.

- Free additional shares: You receive more shares at no extra cost, which increases your holding without any fresh investment.

- No immediate tax: The issuance itself is not a taxable event. Capital gains apply only when you sell.

- Signal of earnings quality: Companies with strong retained profits can afford bonus shares, and the ones that issue them regularly tend to show it.

- More units for future gains: A higher share count amplifies the impact of any future price appreciation.

Advantages of a Stock Split

A stock split has its own set of benefits that should not be overlooked.

- Lower entry price: Lowering the per-share price makes the stock accessible to a wider group of investors.

- Better liquidity: More affordable shares trade more actively, reducing the friction of entering or exiting a position.

- No impact on reserves: Since no reserves are used, the company is able to maintain its financial flexibility and future payout capacity.

- Clean EPS treatment: Unlike a bonus issue, a stock split adjusts the Earnings Per Share (EPS) proportionally, keeping the valuation consistent.

Final Verdict: Bonus vs Split

Both bonus shares and stock splits are changes that do not immediately add to or subtract from your wealth. What they reflect is different, though. A bonus issue says the company has earned and retained enough to give back without touching cash. A stock split says the price has grown enough that access needs to be broadened.

For investors, the wiser approach is to evaluate the business itself rather than read too much into either corporate action alone.