Do you know of investments that are 100% risk-free? There may be a few here and there, but the number of such investments is insignificant.

Investments are known for the risks they carry along with multiplying your wealth. Price fluctuations of investments are uncontrollable, making them risky. But, there must be ways to reduce risk, if not to avoid it. Do you agree?

In today’s article, we will discuss one such theory that aids in mitigating risks while investing. Read further to know the concept and functioning of the Modern Portfolio Theory (MPT).

You may also like: The significance of Porter’s five forces model

What is a portfolio?

A portfolio refers to a collection of different classes of investments that an investor owns.

The purpose of investments is to achieve financial goals. Holding a portfolio of investments rather than a single investment can help to reach that goal sooner.

Basic principles of portfolio management

Portfolios are objective-driven. Some portfolios aim at investing in assets to earn steady income in the long term, while other portfolios may focus on growth in the short term.

Portfolio management is significant in achieving the desired objectives. It refers to investing the right amount of money in different classes of assets and shuffling funds between them based on market conditions to stay in line with the portfolio’s objective.

Below are the basic principles to follow for a portfolio to be successful:

- Identifying the goal – Investors start investing for various reasons. Some investors aim to earn stable additional income in the form of investments. Some others invest in undervalued shares to make profits when prices increase. Understanding the goal of investors is the key to building a portfolio.

- Selection of assets – Assets/instruments in the portfolio must align with the objectives of the portfolio. For investors looking at stable income, a significant portion of investment must go to debt funds, whereas, an investor looking for high returns must hold a portfolio that has a dominant share in equities. Inaccurate selection of assets can lead to failure in achieving financial goals.

- Diversification – Investing in a diverse class of investments is a significant part of building a successful portfolio. Diversification is a well-known technique to mitigate the risks of investments.

- Balancing the portfolio – Investment prices are constantly moving. So, it is essential to shuffle funds between different asset classes to attain profits. Once the result is achieved, the original composition of the portfolio must be restored.

Also read: Your guidebook to Dow theory in technical analysis

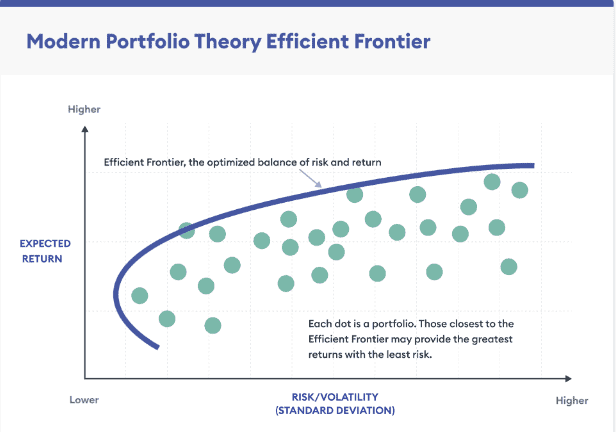

What is modern portfolio theory?

It is a portfolio management theory that suggests building a portfolio where investments are collected, in a way that offers maximum returns at a given level of risk.

All investments are subject to risks. Considering the risk-bearing ability of the investor, the portfolio is optimised to provide the best returns.

The modern portfolio theory is also called Markowitz’s Portfolio theory, as it was introduced by Harry Markowitz in 1952. He was an American Economist. He won the Nobel Prize in 1990 for his contribution towards portfolio management.

Understanding Markowitz Portfolio Theory

The modern portfolio theory applies mathematical and statistical tools to assess the risk and return of different investments to provide maximum profits.

Markowitz’s model of portfolio management

The theory is built on the concept that high-risk investments offer high returns and low-risk investments offer low returns. Markowitz suggests having the right mix of both, to increase returns and decrease risks.

Investments are subject to two main types of risks – Systematic and unsystematic.

Systematic risks are those that impact the entire market. For example, interest rate risk occurs due to changing rates in the economy. Such risks are uncontrollable.

Unsystematic risks are those that are specific to one stock, company or one industry. These risks cannot be avoided wholly but are controllable to a large extent through diversification.

Also read: Behavioural finance: Understanding the psychology behind investment decisions

The risk appetite of investors towards each type of risk is measured, and assets with low risk-low return and high risk-high return are chosen accordingly.

Diversification in this model is done to achieve two objectives:

- To keep the standard deviation of the portfolio close to zero:

Standard deviation is a statistical tool used in finance to measure the risk of an asset. It suggests how prices deviate from their average price during a market uncertainty.

- To maintain minimum covariance between securities:

Covariance measures the degree of relation between securities and how they respond in the same direction. Diversification aims to hold assets having low correlation, to compensate for a downward movement with another upward movement.

Assumptions of the Markowitz portfolio theory

The model has multiple assumptions. Some of them are:

- The efficient market hypothesis, where the model assumes that the security’s prices are accurate and efficient to factor in the effects of the market.

- The investors are rational in choosing their investments.

- Investors are against risk and prefer reducing the degree of risk to the maximum extent possible.

- Investors base their investment decisions on mathematical calculations like expected returns, standard deviation, etc.

Benefits of using Markowitz’s model

- The model uses well-built mathematical tools to arrive at numbers that help in investment decisions.

- Diversification is one of the best techniques to hedge risks in the financial market. This theory follows the same idea.

- Since risk is considered while building the portfolio, it covers the probability of losses due to systematic risks.

- It gives investors exposure to different financial assets.

Criticisms of the model

- The first drawback of the model is its assumptions. There are various criticisms of the theory of rational investors and efficient market hypothesis, like behavioural finance, that identify human emotions behind investment decisions.

- The model considers risks and returns but ignores the other costs associated with investments, which will impact the final profit.

Modern Portfolio Theory Formula

Modern Portfolio Theory (MPT), developed by economist Harry Markowitz, focuses on building an investment portfolio that maximises returns while minimising risk through diversification. The theory suggests that investors should not evaluate assets individually but rather consider how they work together within a portfolio.

The core formula in modern portfolio theory is the expected portfolio return, calculated as the weighted average of returns of all assets in the portfolio.

Where:

- E(Rp) = Expected return of the portfolio

- Wi = Weight of each asset in the portfolio

- Ri = Expected return of each asset

Another key part of MPT is the portfolio variance formula, which measures portfolio risk by considering correlations between assets.

This formula shows that diversification can reduce overall portfolio risk when assets are not perfectly correlated.

Modern Portfolio Theory And Investment Analysis

Modern Portfolio Theory plays an important role in investment analysis and portfolio construction. It helps investors understand how combining different assets—such as stocks, bonds, and other securities—can improve the overall risk-return profile of a portfolio.

Instead of selecting investments based only on individual performance, MPT encourages investors to evaluate how assets interact with each other. For example, combining a high-growth but volatile stock with stable bonds can create a balanced portfolio that delivers stable returns with controlled risk.

Investment managers often use MPT principles to build diversified portfolios that aim to achieve optimal returns for a given level of risk.

Modern Portfolio Theory Assumptions

Modern Portfolio Theory is based on several key assumptions about how markets and investors behave.

First, it assumes that investors are rational and risk-averse, meaning they prefer higher returns with lower risk. Second, the theory assumes that investors make decisions based on expected returns and volatility.

Another assumption is that markets are efficient, meaning all available information is already reflected in asset prices. MPT also assumes that investors have access to the same information and can borrow or lend money at a risk-free rate.

While these assumptions help build the theoretical framework, real-world markets may not always behave exactly as the theory predicts.

Modern Portfolio Theory Asset Allocation

Asset allocation is one of the most important applications of modern portfolio theory. It involves distributing investments across different asset classes such as equities, bonds, commodities, and cash equivalents.

The goal is to achieve the best possible risk-return balance. For example, younger investors with higher risk tolerance may allocate a larger portion of their portfolio to equities, while conservative investors may focus more on bonds and stable income-generating assets.

MPT highlights that diversification across uncorrelated assets can reduce overall portfolio risk without necessarily reducing expected returns.

Modern Portfolio Theory Criticism

Despite its popularity, modern portfolio theory has faced several criticisms.

One major criticism is that the theory relies heavily on historical data, which may not accurately predict future market behaviour. Financial markets are dynamic and influenced by unpredictable factors such as economic shocks, political events, and investor sentiment.

Another limitation is that MPT assumes markets are perfectly efficient, which is not always true in reality. Behavioural biases, emotional decisions, and market anomalies can cause prices to deviate from theoretical expectations.

Additionally, during extreme market conditions such as financial crises, correlations between assets may increase, reducing the diversification benefits suggested by the theory.

Even with these criticisms, modern portfolio theory remains a foundational concept in portfolio management and investment strategy.

Bottomline

The modern portfolio theory is also called Markowitz’s mean-variance optimisation model since it is purely based on these statistical formulas to maximise returns for an investor. The model runs on the widely-accepted strategy of diversifying investments to mitigate risks. However, due to the assumptions of the model, the results may not always align with the desired objective.