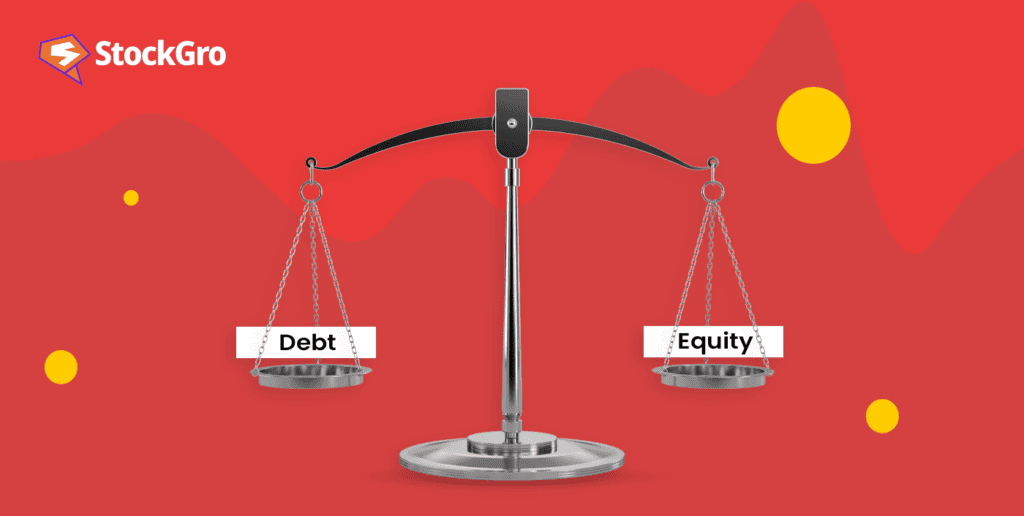

Companies have to raise capital to grow. In the broadest classification, there are two ways to do this – either by raising money through debt (either bank debt, or bonds) or by selling parts of the company (equity shares). The capital structure of a company is a mix of equity and debt that it uses to raise money for its expenses and growth.

In this article, we’re going to understand what a capital structure is in depth, explore the differences between debt and equity financing, and comprehend what makes creating an optimal capital structure so difficult, yet interesting!

Understanding capital structure

The optimal capital structure for any business is one that helps it minimise the cost of its capital – that is, helps it raise its money as cheaply as possible. In theory, debt raising through bank debt is the best way to go. This is because interest payments towards repayment of bank debt is tax deductible, which can be a significant next cash inflow for large businesses.

However, it’s not the best solution for everybody. Too much debt on a company’s balance sheet increases risk to shareholders, because they’re the last ones to get paid if the company gets into trouble. Hence, there’s a need for companies to strike the right balance between selling equity and taking on more loans.

You may also like: What is Capital Market – an engaging guide for beginners

The Weighted Average Cost of Capital (WACC)

This is a metric that’s very often used by financial analysts to figure out how expensive it is for a company to raise capital through either of the two sources. The optimal capital structure is one that minimises this number while maximising the market value of the company.

The lower the cost of capital (interest payments on a bank loan, for instance), the higher is the return on that capital for the company. For instance, if a company borrows $2 million at 5%, it has to generate at least 5% return on that money before it can start to see any gains. On the other hand, another company that only pays 3.5% on the same capital starts turning a profit on their investment when they hit 5% returns.

A lower WACC translates into greater cash inflows for the company, which increase its current value.

Choosing between debt and equity

Choosing between debt and equity to finance a company isn’t, most times, a clear choice. Debt is cheaper than equity because it is less risky, but concerning for investors. Typically, the return required to compensate debtors is less than the return equity investors expect from the company.

But that becomes a problem when you understand that debt payments are always given more priority over dividend payments to shareholders. Suppose a company goes bankrupt and has to liquidate its assets.

- If you’re a bondholder / the bank – you’d get paid first with the money that the company raises by liquidating its assets. All your debts would be paid.

- If you’re a shareholder – you’d be the last one to take your share of the liquidation.

This means that even though equity holders get a better return on their investments in a well-performing company, debt investors are less at risk.

Also Read: Debt instruments in India: Understanding your investment options

Can a company be completely financed by debt?

Theoretically, it could be, but this is far from ideal. This is because as debt increases, so does a company’s interest payments. This means that it would have to have cash flows every year to generate profits that would enable it to make those payments on time.

Furthermore, as a company tacks on more debt, the capital structure becomes more risky for equity investors. They start expecting better returns to take on more risk, which puts an added pressure on the company to generate cash flows to pay dividends. The value of the business goes down because the WACC increases throughout the income statement.

Finding the optimal capital structure

It is usually difficult to point out a standard way of figuring out an optimal capital structure for a company, since it’s something that depends on company to company.

There are several metrics that analysts look at to start. First, a company that has a good potential in the market would always prefer debt, because it wouldn’t want to dilute its existing shareholders. (Dilution happens when existing shareholders of a company own less of it when the company issues new shares to newer investors).

Debt-to-equity is an important ratio that analysts use to figure out how much debt a company has compared to its equity. They also compare other companies in the industry with that number to understand if the company is employing an unusual amount of debt compared to its competitors.

Also Read: Why should you invest in balanced advantage funds?

Conclusion

Since capital structures are so subjective, there’s no magic ratio that prescribes the perfect capital structure. Analysts often use experience and comparables to figure out, roughly, what the optimal structure for a company in a specific industry should look like. It also depends on what growth stage the company is in, the regulatory environment, and other macroeconomic factors.