You must have heard a lot of investment gurus advising you to build a diversified portfolio. This means that you must not put all your money in one security or asset class. Well, this is a basic understanding of building a diversified portfolio.

There is another way you can build a diversified portfolio, where your risks are being diversified away. Let us understand the risk parity portfolio and how you can build one.

To understand this blog, when we say risk, it means standard deviation. The higher the standard deviation, the more uncertain we are about the investment’s short-term horizon.

What is a risk parity portfolio?

Before we begin, risk = standard deviation in this context. The higher the standard deviation, the more uncertain we are about the investment’s short-term horizon.

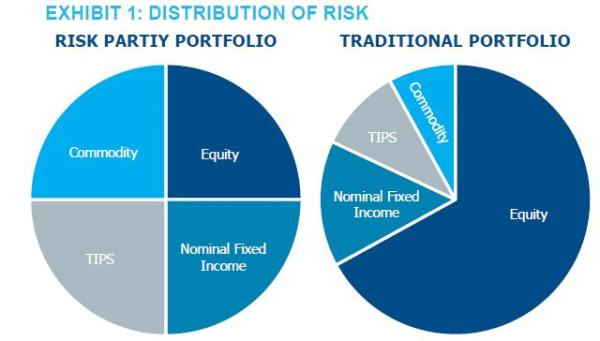

A risk parity portfolio distributes investments based on risk, not the invested amount. Instead of relying on traditional rupee-weighted allocation, a risk parity portfolio focuses on ensuring that each asset class contributes equally to the portfolio’s overall risk.

You may also like: Rebalancing your finances and inner zen!

The problem with traditional portfolios

The risk parity formula came into existence to surpass the traditional 60-40 portfolio. These portfolios have 60% to stocks and 40% to bonds. A notable limitation in the 60-40 portfolio is that approximately 90% of its risk is associated with the stock portion. In simpler terms, the returns of a 60-40 portfolio are highly influenced by stock performance.

When stocks perform well, the 60-40 portfolio tends to see gains, albeit somewhat moderated.

Conversely, the 60-40 portfolio will likely experience losses when stocks underperform. The fate of the 60-40 portfolio is intricately tied to the performance of stocks.

Basics of a risk parity portfolio construction

Hedge funds, HNIs (High net-worth individuals) and UHNIs (ultra-high-net-worth individuals) are the ones who use the risk parity portfolio. It uses a sophisticated quantitative methodology, differentiating it from more straightforward allocation strategies. Its primary objective is to attain the ideal level of return at a specified risk threshold.

Risk parity portfolio optimisation provides the flexibility to employ leverage, alternative diversification, and even short selling in both portfolios and funds.

In contrast to traditional allocation methods, risk parity allows portfolio managers to exercise discretion when selecting asset combinations.

Instead of determining allocations to diverse asset classes in pursuit of an optimal risk target, risk parity strategies establish the optimal risk target level in advance as their foundational investment principle.

Also read: Risk management in stock market

Understanding risk parity with an example

To illustrate this, consider the 60-40 portfolio, where stocks carry a higher portion of the risk. In the context of risk parity, this calls for a substantial shift towards allocating more to bonds and less to stocks. Achieving an equitable risk distribution could lead to a revised allocation of around 20% to stocks and 80% to bonds, altering the original 60-40 ratio significantly.

This shift results in significant reductions in both portfolio returns and risk. However, it may not be your ideal portfolio. The 20% stocks and 80% bonds allocation would create an exceptionally low-volatility portfolio. This would suit an extremely risk-averse individual primarily focused on generating income rather than capital appreciation.

Fundamental assumptions of risk parity come into play:

- Riskier assets are expected to yield higher returns than cash, allowing them to be leveraged (i.e., borrowed funds, effectively shorting cash to purchase more risky assets) to achieve superior portfolio returns. This approach results in a negative allocation to cash and a >100% allocation to risky assets, such as stocks and bonds.

- All assets are assumed to have similar Sharpe ratios, representing the expected return divided by the volatility of returns. If this holds, investors can leverage assets without compromising portfolio efficiency (Sharpe ratio). The goal is to maintain a portfolio with the highest Sharpe ratio, aiming for the highest return per unit of risk exposure.

The solution, according to the risk parity strategy, is leverage. The portfolio allocation for risk parity typically involves doubling the 20-80 allocation discussed earlier, resulting in a -100% allocation to cash. In this scenario, the portfolio is leveraged 2 to 1, meaning that an additional rupee is borrowed to invest for each rupee in the portfolio.

Leverage (borrowing) comes with a cost, as investors must pay a financing rate for borrowing funds to purchase more stocks and bonds than their initial capital allows.

Leveraging in this manner effectively doubles the risk in the portfolio. The short cash position is generally considered risk-free, which means that doubling the exposure to stocks and bonds also doubles the overall risk.

While leveraging doubles the pre-financing-cost return of the portfolio, it does not double the return once the cost of shorting cash is accounted for. This means that the impact of leverage on return is not one-to-one.

The risk parity portfolio allocates a substantial percentage to bonds. Some might even consider risk parity as essentially a leveraged bond portfolio. This is because bonds have lower risk when compared to stocks, leading to a greater allocation to them within the portfolio.

Also read: How to benchmark like a boss: Your guide to investment success!

Pros & Cons

Let us look at the pros and cons that are associated with the risk parity portfolio:

Pros:

- Traditional portfolios like the 60-40 allocation derive a significant portion of their risk and returns from equities. They perform well during periods of economic growth. As the markets slow down, so do this 60 – 40 portfolio. Risk parity portfolios, on the other hand, distribute risk equally across all assets, enabling them to derive returns from a broader range of factors beyond just the stock market. This diversity makes them potentially well-suited to various economic environments, enhancing their overall diversification.

- Rising interest rates are a significant concern for risk parity investors. When interest rates increase, cash becomes more appealing relative to other assets, particularly bonds. This scenario can lead to a decline in the value of nearly all assets in the risk parity portfolio while the cost of financing rises due to higher interest rates.

Cons:

- Leverage introduces risk into the equation. The risk parity portfolio relies heavily on the assumption that assets are diversified (with correlations across asset classes significantly less than one). However, it’s important to recognise that there’s a possibility that all assets might decline simultaneously. In this scenario, the portfolio would perform terribly.

- Risk parity may be susceptible to overfitting the portfolio to historical data. Bonds have exhibited exceptional performance over the past few decades, driven by a consistent decline in interest rates. During this period, bonds outperform cash, making leverage an attractive choice.

Conclusion

Risk parity is an innovative approach to portfolio management that challenges the traditional notion of portfolio allocation. By focusing on risk rather than capital, risk parity aims to create well-diversified portfolios with balanced risk contributions from various asset classes. Many fund houses have started to offer risk parity ETFs that trade on the exchange. As a retail investor, you start by investing in these ETFs.

As financial markets evolve, risk parity remains a noteworthy portfolio strategy, offering a unique perspective on portfolio diversification and risk management. Whether it becomes the core of an investor’s strategy or an addition to a diversified portfolio, risk parity represents an intriguing approach in the ever-evolving landscape of investment and asset management.