Summary:

This blog covers how tax on share buybacks works in India and who is responsible for paying it under the current rules.

It explains the shift from company-level tax to shareholder-level capital gains, the tax rates for long-term and short-term holders, and the implications for retail, promoter, and non-resident investors.

It also explores why companies announce buybacks and how buyback taxation compares with dividend taxation.

Share buyback taxation has changed not once but twice in quick succession, leaving most investors confused. Whether you are a shareholder deciding to tender shares, or trying to make sense of your Income Tax Return (ITR), this guide walks you through how buyback taxation works, and what you should factor in before acting.

What Is Share Buyback?

A share buyback is when a company purchases its shares back from current shareholders, which reduces the number of outstanding shares available in the market. It is carried out through one of these different buyback methods:

- Tender offer: The company offers the shareholders to acquire their shares at a fixed price within a set window. This is the most common route today.

- Open market purchases: Earlier, companies could also buy back shares directly through stock exchanges. The Securities and Exchange Board of India (SEBI) discontinued this route to address participation inequities and tax distortions.

- Direct negotiation: A company may also repurchase shares through a privately negotiated deal with a specific shareholder or group of shareholders. This route is less common and typically seen in unlisted companies.

The offered price is usually at a premium to the prevailing market price, which is what makes buybacks worth paying attention to.

How Buyback Taxation Works in India

The proceeds from buybacks are treated as capital gains, starting from April 1, 2026. Tax is calculated only on the net profit, based on the duration of the holding.

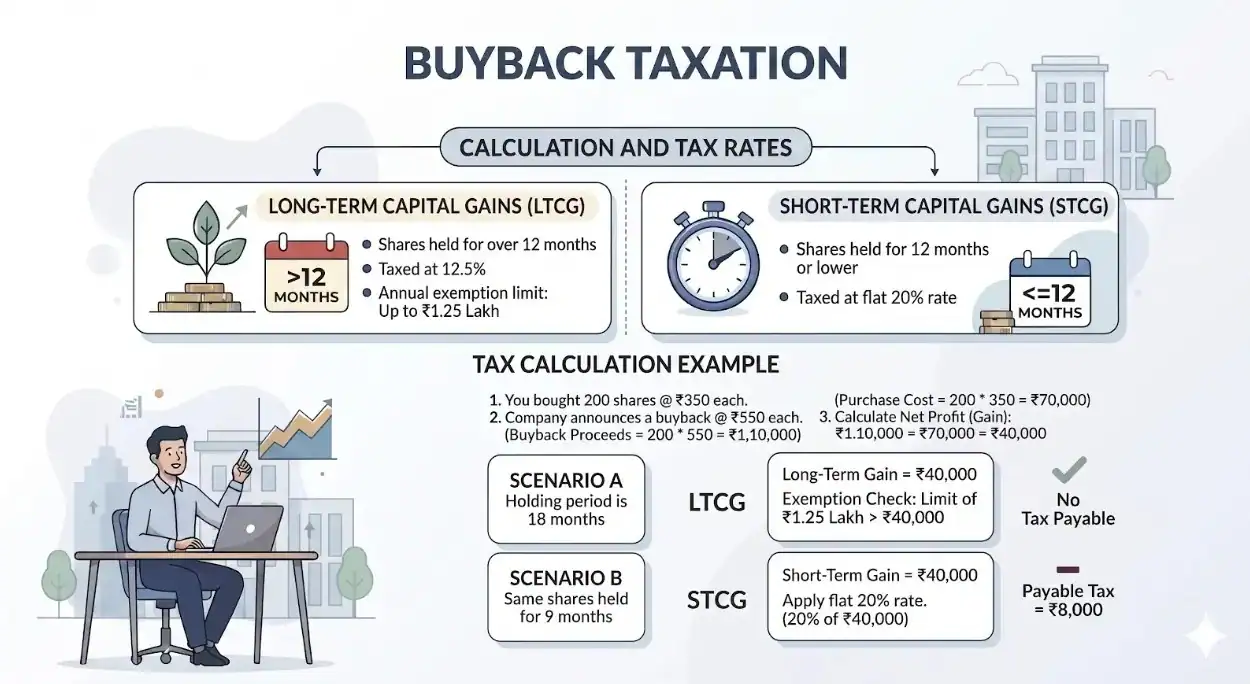

Calculation and Tax Rates

- Long-Term Capital Gains (LTCG): When shares are held over 12 months, they are taxed at 12.5%. An annual exemption limit of up to ₹1.25 lakh is given.

- Short-Term Capital Gains (STCG): If the holding period is less than or equal to 12 months, the shares are taxed at 20%.

Example: You bought 200 shares at ₹350 each, and the company announces a buyback at ₹550. The holding period is 18 months. Your gain is ₹40,000. Since this falls under the ₹1.25 lakh exemption, no tax is payable. If the same shares were held for 9 months, STCG at 20% would apply, making your payable tax ₹8,000.

Worth noting: If there are any losses from buybacks, they can be set off against other capital gains. This can be carried over up to eight years.

Earlier Tax Structure vs Current Rules

The jump from company-level tax to shareholder-level capital gains is a meaningful one, both structurally and in what it costs.

Before October 2024

The companies were required to pay tax on the difference between the issue price and the buyback price. Shareholders used to receive proceeds with zero tax liability.

October 2024 to March 31, 2026

Buyback proceeds were reclassified as deemed dividends on October 1, 2024, to correct this asymmetry. It made them taxable for shareholders as per the rate of their income slabs.

April 1, 2026 onward (current rule)

The deemed dividend treatment was reversed. Buyback proceeds now fall under capital gains, and shareholders are taxed only on the net profit, meaning the buyback price received minus what they originally paid for the shares.

Who Pays Tax on Buyback Now

From April 1, 2026, the shareholder pays the tax. The company has no buyback tax obligation.

Resident shareholders self-report capital gains from a buyback in their ITR. They are no longer subject to Tax Deduction at Source (TDS) on buyback proceeds.

Non-residents stand on different grounds entirely. Section 195 continues to govern withholding for them, at either the domestic rate or the Double Taxation Avoidance Agreements (DTAA) rate, whichever is kinder to the shareholder.

Impact on Retail Investors

Let’s take a closer look at how investors are affected after the switch to capital gains taxation for buybacks.

- Tax on actual gain only

The full buyback receipt is no longer taxable. Only the profit is brought to tax, making the revised system more investor-friendly. - LTCG exemption

Gains up to ₹1.25 lakh in a financial year from listed equity remain exempt. Long-term shareholders with a modest number of shares may attract no tax at all. - Short-term holders

Investors who bought shares within 12 months of a buyback offer face STCG at 20%. Tendering shares in a hurry may cost more in tax than it saves in premium capture, especially for smaller holdings. - Simpler reporting

The capital loss complication that existed under the deemed dividend regime has gone. There is no longer a need to separately account for acquisition cost as a carry-forward loss. The buyback taxation is now structurally identical to selling shares in the secondary market.

Why Companies Announce Buybacks

A buyback decision is influenced by multiple business and financial considerations rather than one standalone objective.

- Distributing Surplus Cash: When a company holds liquidity in more than near-term needs, returning it to shareholders through a buyback is often preferred over letting it sit idle.

- Lifting Earnings per Share (EPS): Reducing the total shares outstanding allows earnings to be distributed over a smaller pool of shares. EPS goes up without any change in actual profitability, improving the valuation.

- Market Signal: When management is buying back shares at a premium to market price, it is a visible signal that they believe the stock is worth more than its current market price.

- Offering an Exit: For shareholders looking to partially or fully exit a position, a buyback provides a price-certain opportunity, often at a premium.

Tax Implications for Different Scenarios

The tax outcome on a buyback depends on who the investor is and how long the shares were held. Here is how it maps across common situations:

| Investor Type | Holding Period | Tax Rate |

| Retail | Over 12 months | 12.5% LTCG |

| Retail | Under 12 months | 20% STCG |

| Promoter | Over 12 months | 12.5% LTCG + additional buyback tax |

| Promoter | Under 12 months | 20% STCG + additional buyback tax |

| Non-resident | Over 12 months | 12.5% LTCG or applicable DTAA rate |

| Non-resident | Under 12 months | 20% STCG or applicable DTAA rate |

Retail

Long-term holders pay 12.5% LTCG, with the ₹1.25 lakh annual exemption applying. Short-term holders pay 20% STCG with no exemption.

Promoters

Standard capital gains rates apply, plus an additional buyback tax is levied, putting the effective rate at approximately 22% for domestic company promoters and around 30% for non-corporate promoters, excluding surcharge and cess.

Non-Resident Shareholders

Long-term gains are taxed at 12.5% and short-term at 20% for non-residents. Where a DTAA provides a more favourable rate, that applies subject to a valid residency proof. Section 195 TDS provisions still apply in both cases.

One thing to be clear about: the buyback price is not what gets taxed. Only the gain over what you paid originally is taxable. A shareholder who bought shares at ₹400 and receives ₹700 in a buyback pays tax on ₹300, not ₹700.

Buyback vs Dividend: Tax Comparison

Here is a table drawing a comparison of dividend vs buyback tax:

| Parameter | Buyback (from April 2026) | Dividend |

| Tax Base | Net gain (price minus cost) | Full amount received |

| Tax Rate | 12.5% LTCG, 20% STCG | Slab rate, up to 30% |

| Reporting Head | Capital gains in ITR | Income from other sources |

| Exemption | Up to ₹1.25 lakh | None |

- Tax Base: A buyback taxes only the profit. A dividend taxes the entire receipt. This can create a substantial difference in the taxable income.

- Tax Rate: A buyback has significantly less tax burden compared to dividends, whose tax rate can go up to 30%, based on the income slab.

- Reporting Head: Dividend is reported under the relevant “other sources” income category. Buyback gains go into the “capital gains” head, which is familiar territory for most investors who hold listed equity.

- Exemption: Buybacks benefit from the LTCG annual exemption. Dividends carry no equivalent threshold relief.

Final Takeaway for Investors

Buyback taxation in India is in a cleaner and more investor-friendly shape than it has been in the last few years. Long-term shareholders benefit from capital gains treatment, with tax applying only on the actual profit made. Short-term holders need to weigh the STCG rate before deciding whether to participate. For most retail investors who have held shares through a typical market cycle, a buyback offer at a premium to market price is a reasonably attractive exit route.

Always verify your holding period and acquisition cost before tendering shares in any buyback.

FAQs

Yes. Buyback gains are taxable in investors’ hands as capital gains. Tax applies only to the profit, not the full buyback amount.

From April 1, 2026, shareholders pay tax on buyback gains. Companies no longer pay buyback tax under the current structure.

A buyback can be more tax-efficient because only the net gain is taxed, while dividends are taxed on the full amount received at the applicable slab rates.

Companies use buybacks to return surplus cash, improve EPS, signal confidence in valuation, or offer shareholders an exit.

They can be useful for long-term investors, especially when offered at a premium and when gains fall within the LTCG exemption limit.