Summary

The binomial option pricing model is a method to estimate the fair value of options using a discrete-time framework.

It models possible future price movements and calculates option payoffs at each node.

This approach helps traders and analysts price options accurately while considering volatility, time, and interest rates. The model is widely used for both American and European options.

What are Binomial Option Pricing Models

A binomial option pricing model is a method used to estimate the fair value of options by modeling the potential future movements of an underlying asset. Unlike a single-point formula, it considers multiple possible paths that the stock price could take over time. This approach makes it versatile for valuing both options trading instruments, including European and American options.

Traders appreciate the binomial model because it allows stepwise calculations, taking into account price volatility, interest rates, and dividends over multiple periods. Its lattice structure makes it especially useful for American options, where early exercise decisions must be incorporated into pricing.

How the Binomial Option Pricing Model Works

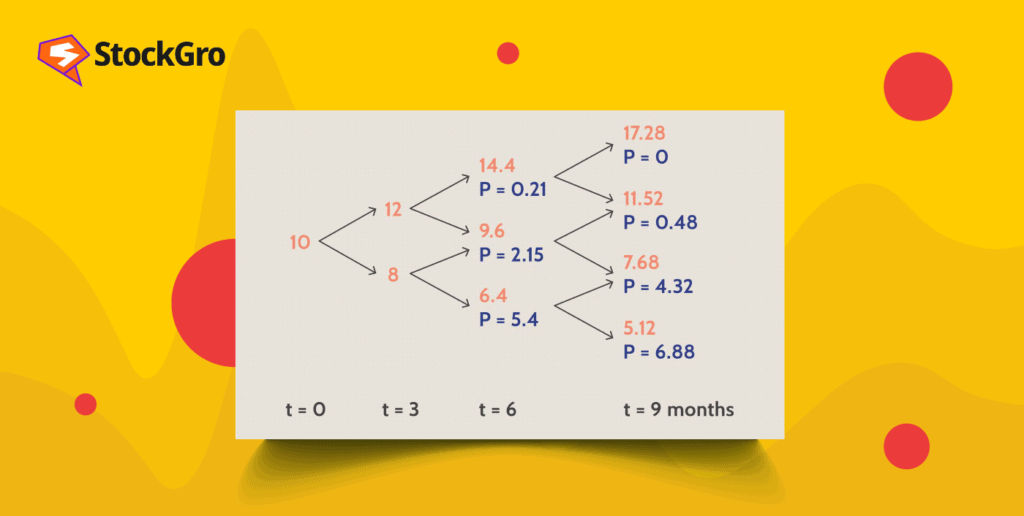

The binomial model creates a lattice of possible future stock prices, evaluating each step to determine the option’s fair value. Here’s a deeper look:

- Step 1 – Define Time Intervals: Divide the option’s life into n discrete periods. Shorter intervals provide more accurate results but increase computation.

- Step 2 – Calculate Up (u) and Down (d) Factors: Determine the potential upward and downward movement of the stock per interval using volatility:

where σ is volatility and Δt is the length of one interval.

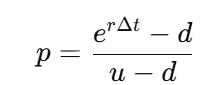

- Step 3 – Determine Risk-Neutral Probability: Calculate the probability of an upward move:

where r is the risk-free rate. This ensures expected returns align with the risk-free rate.

- Step 4 – Work Backwards to Price Option: Start from option values at expiration and discount back using the risk-neutral probabilities. Early exercise decisions are incorporated for American options.

Additional tips:

- Multiple steps allow capturing volatility changes and market paths.

- Adjusting intervals lets traders test sensitivity to time and volatility.

- The model works for calls, puts, and exotic options, making it versatile.

Key Components Used in the Binomial Model

- Underlying Stock Price (S0): The current market price of the asset.

- Strike Price (K): The predetermined price at which the option can be exercised.

- Time to Expiration (T): The duration remaining until the option expires.

- Volatility (σ): Measures how much the underlying asset price is expected to fluctuate.

- Risk-Free Rate (r): The interest rate of a risk-free investment, used for discounting.

- Up (u) and Down (d) Factors: Multipliers representing potential price movements in each time step.

- Risk-Neutral Probability (p): Probability that aligns expected return with the risk-free rate, used to calculate expected option value.

Advantages and Limitations of Binomial Option Pricing Models

Advantages

- Supports American Options: Can handle early exercise features, unlike Black-Scholes. This allows accurate pricing for options where early exercise is possible.

- Flexible Time Intervals: Adjusting the number of steps allows traders to balance accuracy and computational load.

- Visual Representation: The lattice structure clearly shows all possible price paths and option outcomes.

- Customizable for Dividends and Complex Payoffs: Can factor in expected dividends and exotic payoff structures.

- Practical for Risk Management: Helps in assessing potential outcomes under different volatility scenarios.

Limitations

- Computationally Intensive: Large number of steps increases calculation time and complexity.

- Dependent on Accurate Inputs: Wrong estimates for volatility or risk-free rate can misprice the option.

- Steeper Learning Curve: Requires understanding of probability, discounting, and option mechanics.

- Interval Sensitivity: Too coarse a grid may underestimate option value; too fine increases complexity unnecessarily.

- Limited Intuition: Beginners may struggle to connect lattice steps to real-world market behavior.

Binomial Model vs Black-Scholes Model

| Feature | Binomial Model | Black-Scholes Model |

| Asset Type | European & American | Primarily European |

| Early Exercise | Supports American options | Not suitable for American options |

| Computation | Stepwise, lattice-based | Closed-form formula |

| Flexibility | High, adjustable steps | Less flexible for complex scenarios |

| Ease for Beginners | Moderate, visual | Easier for standard options |

Real-World Examples and Practical Use Cases

Institutional Applications

Financial institutions and corporations widely use the binomial option pricing model to price complex derivatives and manage risk. For instance, banks apply the model to value employee stock options, especially American options with early exercise features. Portfolio managers also simulate multiple price paths to hedge large equity positions, assess exposure, and prepare for market volatility.

Retail Trader Applications

Individual traders and retail investors use the binomial model to evaluate options for short-term strategies. For example, a trader buying a call option on a stock priced at ₹1,000 with a strike of ₹1,050 can calculate potential outcomes using a 3-step binomial tree. This helps in determining fair option prices, planning entry and exit points, and adjusting positions based on market movement, volatility, and risk tolerance.

Common Mistakes Traders Make While Using Option Pricing Models

Ignoring Volatility Changes

Volatility directly impacts option pricing. Using outdated historical volatility can misrepresent potential outcomes, leading to incorrect trade decisions.

Skipping Risk-Free Rate Adjustments

Failure to correctly apply the risk-free discounting can overestimate or underestimate the option’s current value.

Neglecting Dividends

Omitting expected dividends affects the price of American options, especially those likely to be exercised early.

Overcomplicating Steps

Too many time intervals may increase computation without improving accuracy significantly. Traders should balance detail with efficiency.

Misapplying American vs European Assumptions

Using European-style assumptions for American options ignores early exercise potential, leading to undervaluation.

Not Backtesting Models

Failing to validate the model against historical data reduces reliability and may result in unexpected losses.

Ignoring Transaction Costs

Real-world trading involves brokerage and margin costs; neglecting these can erode expected profits from modeled strategies.

How to Start Learning and Practicing Option Pricing Strategies

- Use Virtual Trading Platforms: Practice without risking real money.

- Study Option Mechanics: Understand stock options, Greeks, and payoff diagrams.

- Start Simple: Begin with European options before attempting American options with early exercise.

- Simulate Multiple Scenarios: Test changes in volatility, strike prices, and expirations to see effects on option value.

Final Thoughts

The binomial option pricing model is an invaluable tool for traders and investors seeking to value options systematically. Its stepwise structure allows for flexible application, especially for American options or complex payoffs. Beginners should start with simulations and gradually incorporate more steps and scenarios to build confidence in their trading and hedging strategies.

FAQs

Yes. It’s a method that values options using a step-by-step price tree with multiple possible outcomes.

Yes. Unlike Black-Scholes, the binomial model can price American options and allows early exercise decisions.

Yes. Volatility determines potential price swings, directly impacting the value and risk of options.

Yes. Beginners can start with few steps and simple options to understand the method before advancing.

Yes. Options that can be exercised before expiry, which the binomial model can account for step-by-step.

Yes. Use virtual trading platforms or demo accounts to simulate strategies safely.