What is Capital Protection Fund?

A capital protection fund is a closed-ended hybrid mutual fund scheme whose portfolio is deliberately structured to return your initial investment by the time the fund matures, while also giving a portion of the corpus the opportunity to grow through equity exposure.

According to the Securities and Exchange Board of India (SEBI), these schemes have to be called Capital Protection Oriented Funds (CPOFs) because protection here is an objective, not a guarantee. It comes from how the portfolio is structured rather than from any insurance cover or institutional backing.

How Capital Protection Funds Work?

The fund manager divides the corpus into two distinct allocations.

- Around 80% flows into high-rated debt instruments like AAA-rated bonds, government securities, treasury bills, and certificates of deposit. This debt portion is managed so that by the time the mutual fund matures, its grown value matches the original amount invested.

- The remaining portion, roughly 20%, goes into equities. Good equity performance adds returns on top; poor performance hurts the upside but does not affect the principal protection already created by the debt component.

Key Features of Capital Protection Funds

Before putting money into one of these schemes, it helps to know exactly what you are dealing with structurally.

- Always closed-ended: You cannot enter or exit freely during the tenure. The fund opens during a New Fund Offer (NFO) period and matures on a fixed date.

- Fixed tenures: These funds run for three to five years, giving investors a structured window that sits between short-term fixed income products and longer equity commitments.

- Mandatory credit rating: Unlike most fund categories, every CPOF must carry a CRISIL or equivalent rating, offering an independent read on how robust the capital protection structure actually is.

- Highest-rated debt only: SEBI mandates that the debt component be invested exclusively in instruments with the highest credit ratings, keeping speculative risk out of the safety engine entirely.

- Exchange listed: Units trade on the Bombay Stock Exchange (BSE) and the National Stock Exchange (NSE), though secondary market liquidity tends to be thin in practice.

Benefits of Investing in Capital Protection Funds

For the right investor profile, these funds solve a very specific problem rather elegantly.

- Principal safety by design

The debt allocation is calibrated to return the initial amount by maturity. Even a flat equity market does not cost you your capital. - Equity upside without risking the principal

The equity slice gives you genuine exposure to market growth while the bulk of your money stays anchored in high-rated debt instruments. - Built for defined goals

As these funds have a fixed maturity date, they align naturally with time-bound financial targets like a down payment for a house, a wedding fund, or a child’s tuition that kicks in at a known point. - A natural guard against impulsive exits

The closed-ended structure makes premature redemption difficult, which keeps investors from making emotion-driven decisions during market fluctuations. - Independent quality check

The mandatory CRISIL rating on every CPOF gives investors something most fund categories simply do not offer: an external, structured assessment of how the protection mechanism holds up.

Risks and Limitations You Should Know

The safety framing around these funds can occasionally create a false sense of certainty. A few realities deserve honest attention.

- Orientation is not an obligation: SEBI has been clear that capital protection is the aim, not the promise. A structural failure in even one component of the debt portfolio can compromise the entire arrangement.

- Credit risk: A bond rated AAA today is not immune to a future downgrade or default. If the debt component weakens, the protection logic weakens with it.

- Interest rate sensitivity: While holding debt avoids mark-to-market losses, a sharp shift in the interest rate environment can still affect the fund’s internal dynamics over multi-year tenures.

- Limited liquidity: Closed-ended is not the same as locked in. You can technically sell on an exchange, but finding a buyer at a fair price before maturity is difficult. Plan as though your money is committed for the full tenure.

- Returns have a ceiling: With only a small fraction of the investment in equities, a CPOF will never compete with a diversified equity fund on raw return numbers. That trade-off is the whole point, but it needs to be accepted going in.

Real-World Scenarios & Use Cases

The theory clicks better once you place it next to real-life situations.

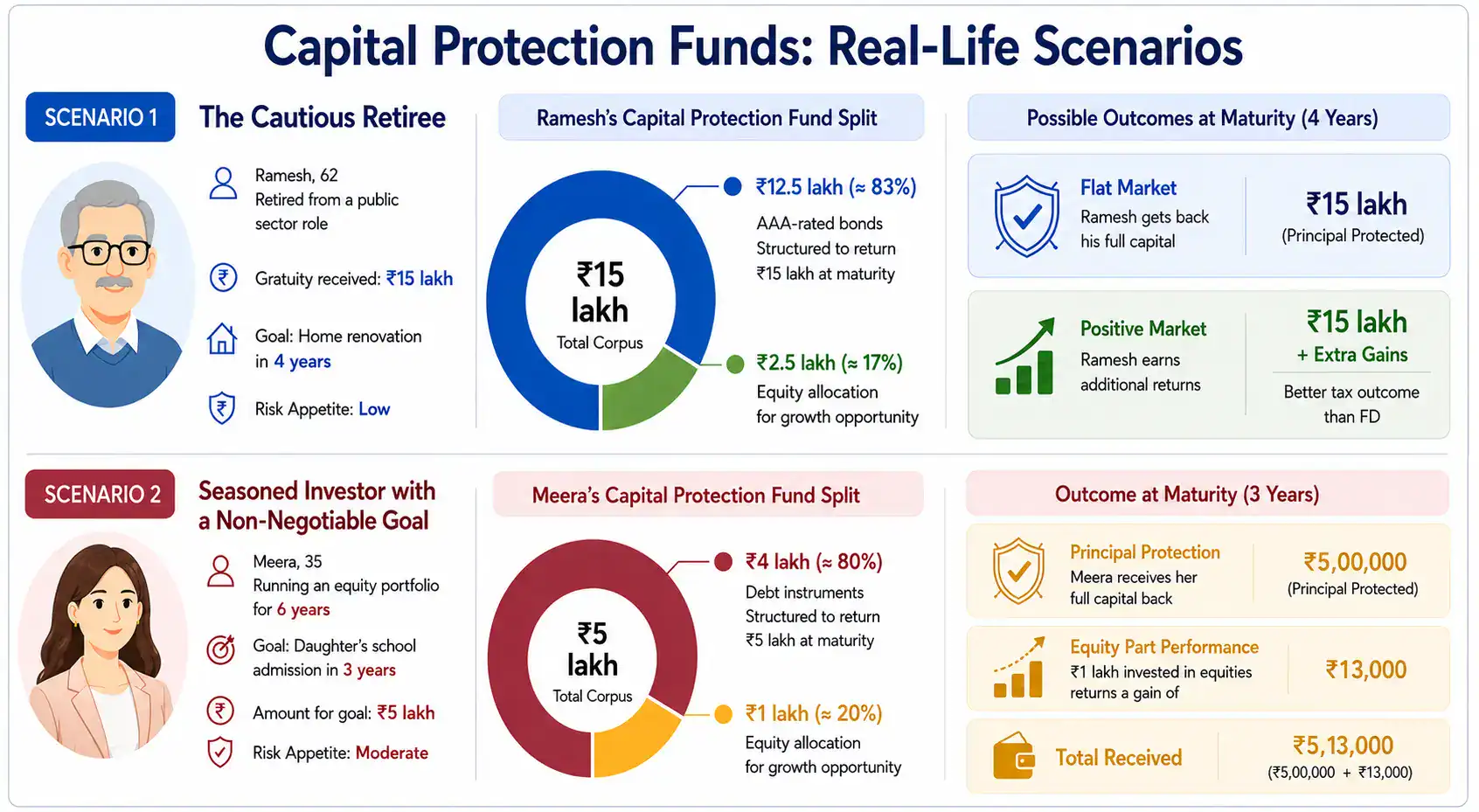

Scenario 1: The Cautious Retiree

Ramesh, 62, recently retired from a public sector role with a gratuity payout of ₹15 lakh sitting in his savings account. He does not need the money right away, but has a home renovation planned four years out. Equity mutual funds make him nervous. A regular FD seems safe, but at his 30% tax slab, the interest returns are significantly eroded.

His financial adviser points him toward a four-year capital protection-oriented fund. Roughly ₹12.5 lakh of his corpus goes into AAA-rated bonds structured to return ₹15 lakh at maturity. The remaining ₹2.5 lakh takes a swing at equities. In a flat market, Ramesh still gets his capital back. If equities cooperate, he walks away with a meaningful gain and a more favourable tax outcome than he would have had from the FD route.

Scenario 2: Seasoned Investor with a Non-Negotiable Goal

Meera, 35, has been running an equity portfolio for six years and is comfortable with volatility. She has ₹5 lakh earmarked for her daughter’s school admission fees due in three years. She simply cannot afford to lose this money. Putting it in equities feels reckless, and parking it in a savings account feels wasteful.

She puts it into a three-year CPOF. Around ₹4 lakh sits in debt instruments, working its way back to the ₹5 lakh principal amount by maturity. The remaining ₹1 lakh participates in equities, returning a modest gain of ₹13,000. The fees are covered, her equity portfolio stays fully invested, and she does not have to choose between growth and certainty.

Common Mistakes Investors Make

Even a conservative product like this comes with its share of avoidable errors.

- Treating orientation as a guarantee: The single most expensive misconception in this category. Read the offer document and understand what the rating actually measures before you invest.

- Getting the tenure wrong: A five-year CPOF is no help if your goal lands in three years. Match the fund’s maturity to your actual cash flow requirement, not the other way around.

- Overlooking the expense ratio: With higher returns already capped by a small equity allocation, every basis point of expense matters more here than in a high-growth equity fund.

- Skipping the debt quality check: AAA is a starting point, not a final answer. Look at the specific instruments inside the portfolio, their concentration, issuer diversity, and duration, as all of them determine the protection structure’s strength.

- Expecting equity-level performance: A CPOF is not a disguised equity fund. Investors who go in hoping for double-digit returns and come out disappointed have simply misread the product from the start.

Conclusion

A capital protection fund is not trying to be everything for every investor. What it does offer is principal safety through portfolio structure, a measured slice of equity growth, and a fixed timeline that suits a precise set of needs. If your goals are defined, your timeline is clear, and your priority is peace of mind over chasing returns, this is a category worth understanding properly.

FAQs

No, these funds are not entirely free from risk. Capital protection is only an investment objective, not a guarantee, and credit or market-related risks can still affect returns.

These funds suit conservative investors seeking limited equity exposure with relatively better capital safety, especially for time-bound financial goals and moderate return expectations.

Unlike fixed deposits, capital protection funds combine debt and equity exposure, offering potential market-linked upside along with comparatively more tax-efficient long-term returns.

Most capital protection funds have fixed maturities ranging between three and five years, making them suitable for medium-term financial planning and defined future goals.

They may outperform inflation over time if the equity allocation performs well, though returns are generally lower than those of diversified equity mutual funds.