Summary

Corporate debt funds invest mainly in high-rated company bonds, with SEBI requiring at least 80% of the portfolio in AA+ and above corporate bonds.

These funds suit investors looking for moderate returns, better liquidity than fixed deposits, and lower volatility than equity funds.

Returns are market-linked, so investors must check credit quality, duration, YTM, expense ratio, exit load, and taxation before investing.

What is a Corporate Debt Fund?

A corporate debt fund is a debt mutual fund that invests in company-issued bonds. The Securities and Exchange Board of India (SEBI) mandates that at least 80% investment of these funds must go into corporate bonds rated AA+ or above.

Put simply, your money is being lent to large, creditworthy corporations. They pay interest on those borrowings, and that income eventually reflects in your returns. Companies issue these bonds for purposes such as managing working capital or refinancing existing debt.

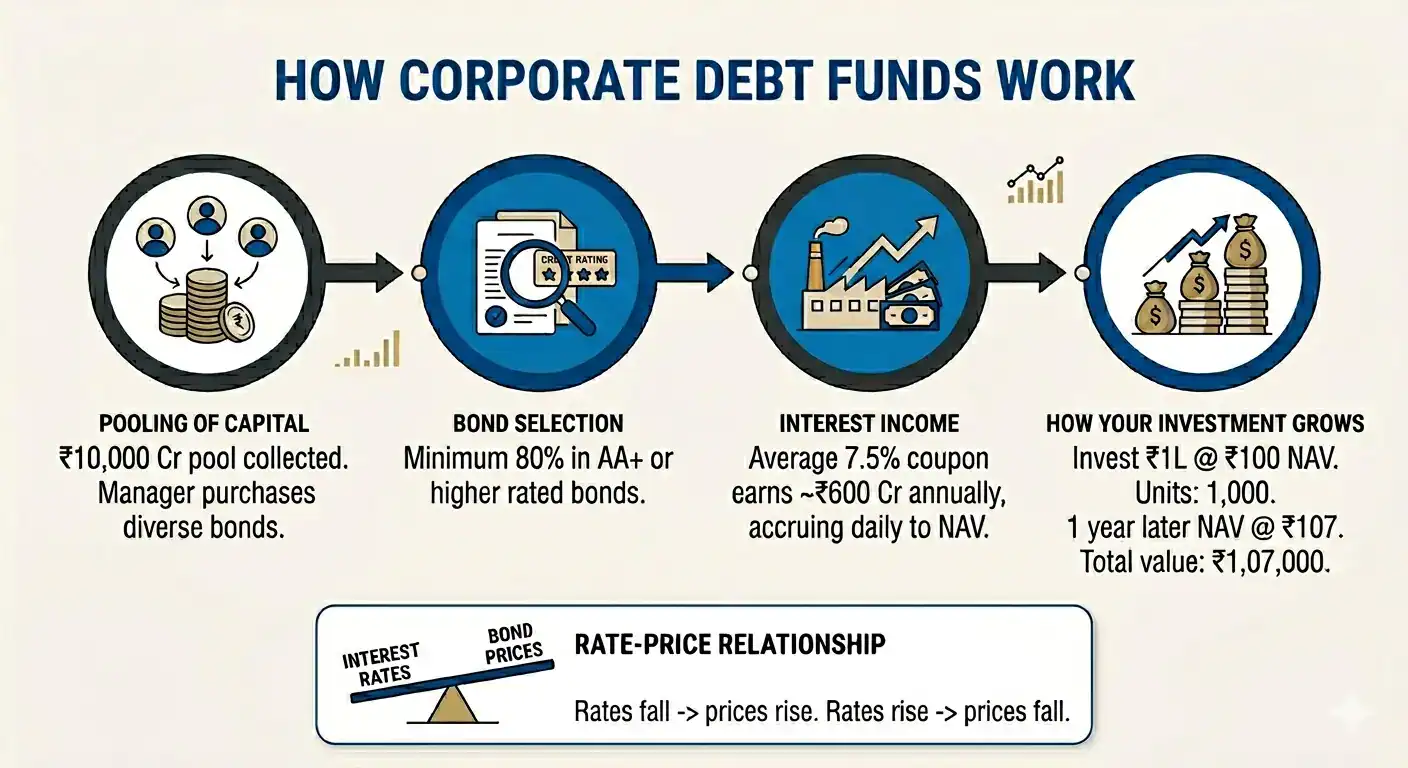

How Corporate Debt Funds Work

The fund pools money from many investors and deploys it across a basket of high-rated corporate bonds. Here is how it actually flows.

Pooling of capital

Assume ₹10,000 crore is collected across investors. The fund manager now has the capital to buy bonds across multiple sectors and issuers.

Bond selection

Fund managers evaluate the credit rating history, financials of the issuer, and prevailing interest rate trends. In this case, a minimum of ₹8,000 crore of the corpus must sit in bonds rated AA+ or higher.

Interest income

Say the fund portfolio carries an average coupon of 7.5% per annum. On ₹8,000 crore, that generates roughly ₹600 crore in annual interest. This accrues into the fund’s Net Asset Value (NAV) daily.

How your investment grows

You invest ₹1,00,000 at a NAV of ₹100. You hold 1,000 units. A year later, the NAV is ₹107. Your investment is now worth ₹1,07,000. That appreciation reflects both the interest income earned and any movement in bond prices.

Rate-price relationship

Bond prices move opposite to interest rates. When rates fall, existing bonds become more valuable. When rates rise, their prices dip. Lately, the bond prices have been stable as the Reserve Bank of India (RBI) has maintained the repo rate at 5.25%, as of April 2026.

Corporate Debt Fund vs Other Debt Funds

Each debt fund category serves a different need. Here is a side-by-side comparison.

| Parameter | Corporate Debt Fund | Gilt Fund | Credit Risk Fund | Liquid Fund |

| Minimum credit quality | AA+ and above | Government securities | AA and below | Very high |

| Return potential | Moderate to moderately high | Moderate | Higher | Low |

| Credit risk | Low | Very low | High | Very low |

| Interest rate sensitivity | Moderate | High | Low to moderate | Very low |

| Ideal holding period | 1 to 3 years | 3 years and above | 2 to 4 years | Days to 3 months |

- Credit Quality: Gilt funds invest only in government securities, making them the safest among these options. Liquid funds also maintain high-quality holdings, while corporate debt and credit risk funds take progressively higher credit exposure.

- Interest Rate Sensitivity: Gilt funds react the most to interest rate movements because of longer maturities. A corporate debt fund carries moderate sensitivity, credit risk funds relatively lower, while liquid funds remain the least affected.

- Return vs Risk: Liquid funds focus on stability and liquidity with lower return potential. Corporate debt funds aim for balanced risk and return, while credit risk funds take higher exposure for stronger yield opportunities.

- Holding Period: Liquid funds are designed for short-term needs, while gilt funds suit longer investment horizons. Corporate debt and credit risk funds are better suited for medium-term goals.

Benefits of Corporate Debt Funds

These funds carry practical advantages that are listed below:

- Regulatory Credit Floor

The 80% AA+ mandate is not a fund manager’s discretion. SEBI enforces it. This structural protection is what makes corporate debt funds a low-risk mutual fund category relative to most alternatives in fixed income. - High Liquidity

A fixed deposit (FD) locks your money in for a set tenure. Corporate debt funds are open-ended. You can exit on any business day at the current NAV, subject to any applicable exit load. - Professional Management

The fund manager tracks credit ratings, issuer health, and duration continuously. That expertise is what most retail investors do not have the time, knowledge, or tools to replicate. - Built-In Diversification

A corporate debt fund holds multiple bonds across sectors like banking, infrastructure, and NBFCs. That spread reduces concentration risk without requiring you to understand each individual issuer.

Risks of Corporate Debt Funds

Corporate debt funds, like all market-linked investments, carry certain risks investors should understand.

- Interest rate risk

Rising rates push bond prices down, which pulls the NAV lower temporarily. Funds with longer durations feel this more sharply. - Credit risk

Even AA+ rated bonds are not immune to downgrades. If an issuer runs into financial trouble, the fund’s NAV takes a hit. Bond default risk is lower here than in credit-heavy categories, but it is not zero. - Liquidity risk

In stressed markets, certain bonds become difficult to sell at fair prices. This can delay or reduce the value realised on redemptions. - Reinvestment risk

When rates fall and bonds mature, the fund must redeploy that money at whatever rates the market offers. Sometimes that means settling for less.

Who Should Invest in Corporate Debt Funds?

These funds are not for everyone, but they suit a broad range of investor profiles.

- Conservative investors who want their money to be professionally managed in the debt market space.

- Working professionals who need a liquid parking space for new opportunities and emergencies.

- Retirees seeking moderate and predictable income with limited market exposure.

- First-time mutual fund investors who are not ready for equity but want to move beyond savings accounts.

- Those using a Systematic Investment Plan (SIP) in debt funds to build a steady corpus in a disciplined way.

Factors to Consider Before Investing

Before you pick a corporate bond fund, it is essential to evaluate the factors influencing it.

- Credit quality mix: Know the fund split before you invest. An AAA rating has the lowest default risk. AA+ offers marginally better yields with slightly more risk.

- Yield to maturity (YTM): YTM is the expected return on holding a bond till maturity. Funds with an unusually high YTM might be carrying lower-rated bonds to appear lucrative. Read the credit quality alongside it.

- Duration: Shorter duration means less sensitivity to rate changes. If you are unsure where rates are headed, a lower duration fund is a calmer choice.

- Expense Ratio: Even a minute difference in the expense ratio compresses net returns over time. Direct plans carry meaningfully lower ratios than regular plans.

- Exit Load: Some funds charge extra for early redemptions, reducing the net gains. Factor that into your investment planning.

Common Mistakes Investors Make

Even simple products get misused. Here are the usual errors investors often make.

- Comparing them to FDs: These are market-linked products. The NAV moves. A bad month is possible. Expecting guaranteed returns is the first and most common error.

- Neglecting manager evaluation: Most investors never check who is managing the fund. That track record through a credit stress cycle is worth looking up before you invest.

- Chasing yields without checking credit: A fund showing 9% YTM when the market average is 7.5% is likely holding lower-rated paper. That is just risk disguised as returns.

- Ignoring portfolio duration: Many investors only look at the returns and stop there. The bond duration actually tells you how much rate risk you are sitting on.

- Exiting prematurely: These funds need some time to work properly. Redeeming earlier means giving up accrued income and potentially paying an exit load.

Taxation on Corporate Debt Funds

The corporate debt fund tax rules have quietly shifted over the years.

Investments made on or after April 1, 2023, are taxed at your income slab rate. The holding period does not matter anymore. For investments made before that date and held beyond 36 months, long-term capital gains tax applies at a flat 12.5% rate.

For investors in higher brackets, the net post-tax return from recent investments is noticeably lower than in the previous structure. Plan redemptions with this in mind.

How to Invest in Corporate Debt Funds

Getting started is simple. Here is a step-wise approach you can take to invest in corporate debt funds:

Step 1: Complete KYC

Your Know Your Customer (KYC) formalities must be done through an AMFI-registered platform. PAN and Aadhaar are required.

Step 2: Choose direct or regular

Direct plans have no distributor commission and a lower expense ratio. Regular plans involve a middleman, providing expert investing advice and convenience at an extra cost. Select the option that best matches your investing confidence and support needs.

Step 3: Evaluate the fund

Do not go only by the highest returns. Deeply examine the credit quality, YTM, and expense ratio across multiple funds before committing.

Step 4: Decide the investment mode

A lump sum works well if you have an existing corpus to deploy. A monthly SIP of even ₹1,000 is enough to get started if you are building gradually.

Step 5: Invest through a registered platform

Use the AMC’s own website or any AMFI-registered investment platform. Verify that the platform follows the regulatory requirements before investing.

Step 6: Review periodically

A review every six months is adequate. Watch for credit rating changes within the portfolio or a significant shift in fund duration.

Final Thoughts

Corporate debt funds are not designed for quick gains. They offer a measured way to earn better than a savings account while staying well clear of equity volatility. The key is going in with realistic expectations, an awareness of the tax structure, and with a medium to long investment horizon. Done right, these funds can earn their place in most portfolios.

FAQs

Corporate debt funds are considered relatively safer within debt mutual funds because they mainly invest in AA+ and above-rated bonds. However, they still carry interest rate, credit, liquidity, and reinvestment risks.

These funds suit conservative investors, retirees, first-time mutual fund investors, and those seeking moderate returns with lower volatility than equities over a medium-term horizon.

Yes, losses are possible if interest rates rise, bond prices fall, or issuers face credit issues. Unlike fixed deposits, returns are market-linked and not guaranteed.

Yes, beginners can consider corporate debt funds as they offer professional management, diversification, and moderate risk compared to equity mutual funds.

They serve different purposes. Corporate debt funds prioritise stability and predictable income, while equity funds aim for higher long-term growth with significantly higher market risk.