Summary

Corporate bonds are debt instruments issued by companies to raise capital from investors.

They offer regular interest income and have defined maturity periods. Corporate bonds are generally less volatile than stocks but carry credit risk depending on the issuer’s financial health.

They are suitable for investors seeking steady returns and moderate risk exposure.

What is Corporate Bond?

A corporate bond is a debt security issued by a company to borrow funds from investors at a fixed or floating interest rate for a predetermined tenure. Investors who buy corporate bonds effectively lend money to the company in exchange for periodic coupon payments and principal repayment at maturity. Corporate bonds are widely traded in secondary markets, and their prices fluctuate based on credit ratings, interest rates, and company performance. For example, monitoring prudent-corporate-advisory-services-ltd-share-price or similar corporate stocks helps investors understand the financial health and credibility of bond issuers.

Corporate bonds are attractive to investors seeking regular income and lower volatility than equities while still participating in corporate growth. They provide a predictable cash flow in the form of coupon payments, which makes them suitable for risk-conscious investors or retirees.

Types of Corporate Bonds Investors Should Know

- Secured Bonds: Backed by company assets; offer lower risk and interest rates.

- Unsecured (Debenture) Bonds: Not backed by assets; rely on the company’s creditworthiness.

- Convertible Bonds: Can be converted into equity shares at a pre-specified price and date.

- Non-Convertible Bonds (NCBs): Cannot be converted into equity; offer higher coupon rates than convertible bonds.

- Callable Bonds: Can be redeemed by the issuer before maturity, typically when interest rates decline.

- Perpetual Bonds: No fixed maturity date; pay coupons indefinitely.

How Corporate Bonds Generate Returns for Investors

Corporate bonds provide two primary sources of returns:

- Coupon Payments: Fixed or floating interest paid periodically, representing regular income.

- Capital Gains: When bonds are sold in the secondary market at prices higher than the purchase price.

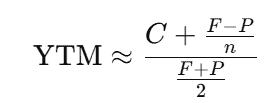

The total return can be estimated using yield to maturity (YTM) formulas:

Where CCC = annual coupon payment, FFF = face value, PPP = purchase price, nnn = years to maturity.

Monitoring a company’s PE ratio and financial health is critical because creditworthiness directly affects interest payments and bond price movements. Strong fundamentals reduce default risk and improve investor confidence.

Benefits and Risks of Investing in Corporate Bonds

Benefits:

- Regular Income: Predictable coupon payments provide cash flow stability.

- Lower Volatility: Less risky than equities; suitable for conservative investors.

- Diversification: Corporate bonds balance equity-heavy portfolios and hedge against market swings.

- Potential Capital Appreciation: Selling in secondary markets can yield gains if market rates decline.

Risks:

- Credit Risk: Default by the issuing company can lead to loss of principal or interest.

- Interest Rate Risk: Rising rates reduce the market value of existing bonds.

- Liquidity Risk: Not all corporate bonds are easily tradable.

- Callable Risk: Issuer may redeem bonds early, affecting expected returns.

- Inflation Risk: Fixed coupons may lose purchasing power during high inflation periods.

Corporate Bonds vs Stocks vs Fixed Deposits

| Feature | Corporate Bonds | Stocks | Fixed Deposits |

| Risk | Moderate; depends on issuer credit rating | High; market-linked | Low; bank-backed |

| Returns | Coupon + capital gains | Dividends + capital appreciation | Fixed interest only |

| Liquidity | Moderate; secondary market trading | High; exchanges | Moderate; premature withdrawal may incur penalty |

| Growth Potential | Limited but predictable | High growth potential | Low growth; safe |

| Suitability | Income-focused investors with moderate risk appetite | Long-term growth-oriented investors | Capital preservation and safety seekers |

| References | Evaluating credit ratings and difference-between-debt-and-equity-ipo | PE ratio, stock performance | Bank interest rates |

How Beginners Can Start Investing in Corporate Bonds

- Open a demat and trading account with an AMC, broker, or online platform.

- Start with secured or high-rated bonds to reduce default risk.

- Use bond ETFs or corporate bond mutual funds for diversified exposure.

- Track issuer performance and macroeconomic indicators affecting interest rates.

- Gradually increase allocation as familiarity and confidence grow.

Corporate Bond Strategies for Smart Portfolio Management

- Laddering Strategy: Invest in bonds with staggered maturities to manage liquidity and reinvestment risk.

- Diversification: Spread investments across sectors and credit ratings.

- Interest Rate Monitoring: Adjust holdings based on expected rate movements to optimize returns.

- Combine with Stocks and FDs: Use bonds to reduce volatility while keeping growth potential from stocks.

- Periodic Rebalancing: Review portfolio regularly to maintain target allocation between bonds, equity, and cash.

Conclusion

Corporate bonds offer a stable and predictable way to earn returns while balancing equity risk. They are suitable for investors seeking regular income, moderate risk, and portfolio diversification. Understanding bond types, issuer creditworthiness, and market dynamics is crucial for maximizing returns. For beginners, starting with secured bonds or bond funds and gradually exploring more sophisticated instruments ensures disciplined investing.

FAQs

Yes. High-rated and secured bonds are relatively safe for beginners compared to stocks, offering predictable income.

Corporate bonds carry credit risk linked to the issuing company, whereas government bonds are generally safer due to sovereign backing.

Yes. Defaults, rising interest rates, or early call provisions can reduce expected returns or principal.

Ratings like AAA or AA indicate strong creditworthiness and lower default risk.

Interest income is taxed as per your income tax slab, while capital gains from bond sales follow short-term or long-term capital gains rules depending on holding period.

Yes. Active trading in the secondary market allows capital gains when market rates fall or bonds are revalued.