Selling a mutual fund unit sooner than planned can quietly add to your tax bill. Short-term capital gains tax on mutual funds applies when you redeem units before completing the required holding period, and the rates have changed significantly. This article walks you through everything from applicable rates to smart tax planning strategies.

Short Term Capital Gain Tax on Mutual Funds

Short-term capital gain (STCG) on mutual funds is the profit made when units are redeemed before completing their stipulated holding period. The tax treatment depends on the type of mutual fund and the duration of the investment.

The STCG rules have shifted since the Finance (No. 2) Act, 2024, came into effect. For those focused on tax-efficient investing, understanding the new rules is an important first step.

STCG Tax Rates on Mutual Funds in India (Latest Rules)

Until July 2024, equity fund investors paid 15% on short-term gains. This was increased to 20% in the Union Budget for 2024-25, declared on July 23, 2024. Here is a summary of the current applicable rates:

| Fund Type | Tax Rate |

| Equity-oriented mutual funds | Flat 20% |

| Debt-oriented mutual funds (invested in on or after April 1, 2023) | Income slab rate |

| Debt-oriented mutual funds (acquired before April 1, 2023) | Up to 36 months: Slab rate, otherwise LTCG rules apply |

A few key points:

- Gains from transactions before July 23, 2024, continue to be taxed at 15%.

- Along with STCG tax, investors are required to pay a 4% health and education cess

Holding Period for Short Term Capital Gains in Mutual Funds

The holding period runs from the purchase date to the redemption date.

For equity and equity-oriented hybrid funds, gains are short-term if units are sold within 12 months.

Debt funds bought before April 1, 2023, follow a 36-month holding period rule. For newer debt fund investments made on or after April 1, 2023, the holding period does not change their short-term tax treatment.

In Systematic Investment Plan (SIP) redemptions, the holding period is checked instalment by instalment. A single redemption can therefore contain both LTCG and STCG components. This is one of the most misunderstood aspects of SIP tax rules: the SIP start date does not determine the holding period; each instalment’s own purchase date does.

Tax-Saving Strategies for Short Term Capital Gains

Managing STCG tax is not about avoiding it, but timing and structuring the exits sensibly. Here are some approaches that work.

Hold Investments Longer When Possible

Staying invested beyond 12 months in equity funds moves gains from the 20% STCG rate to the lower long-term capital gain tax on mutual funds rate of 12.5%. You also unlock the ₹1.25 lakh annual exemption that STCG does not offer. When there is no urgent reason to exit, waiting pays.

Use Tax-Loss Harvesting

Tax-loss harvesting involves booking losses on underperforming funds to offset your STCG. Investors can offset short-term capital losses against both short-term and long-term gains, while unused losses may be carried forward for 8 years.

Choose Tax-Efficient Funds

Index funds and ETFs generate fewer internal portfolio churn events. For investors looking for tax efficiency, these options are worth considering as part of a broader long-term investment strategy.

Plan Withdrawals Smartly

You may use any unused basic exemption limit under your chosen tax regime to reduce your STCG before applying the 20% rate. Spreading the redemptions across years keeps your taxable gains manageable.

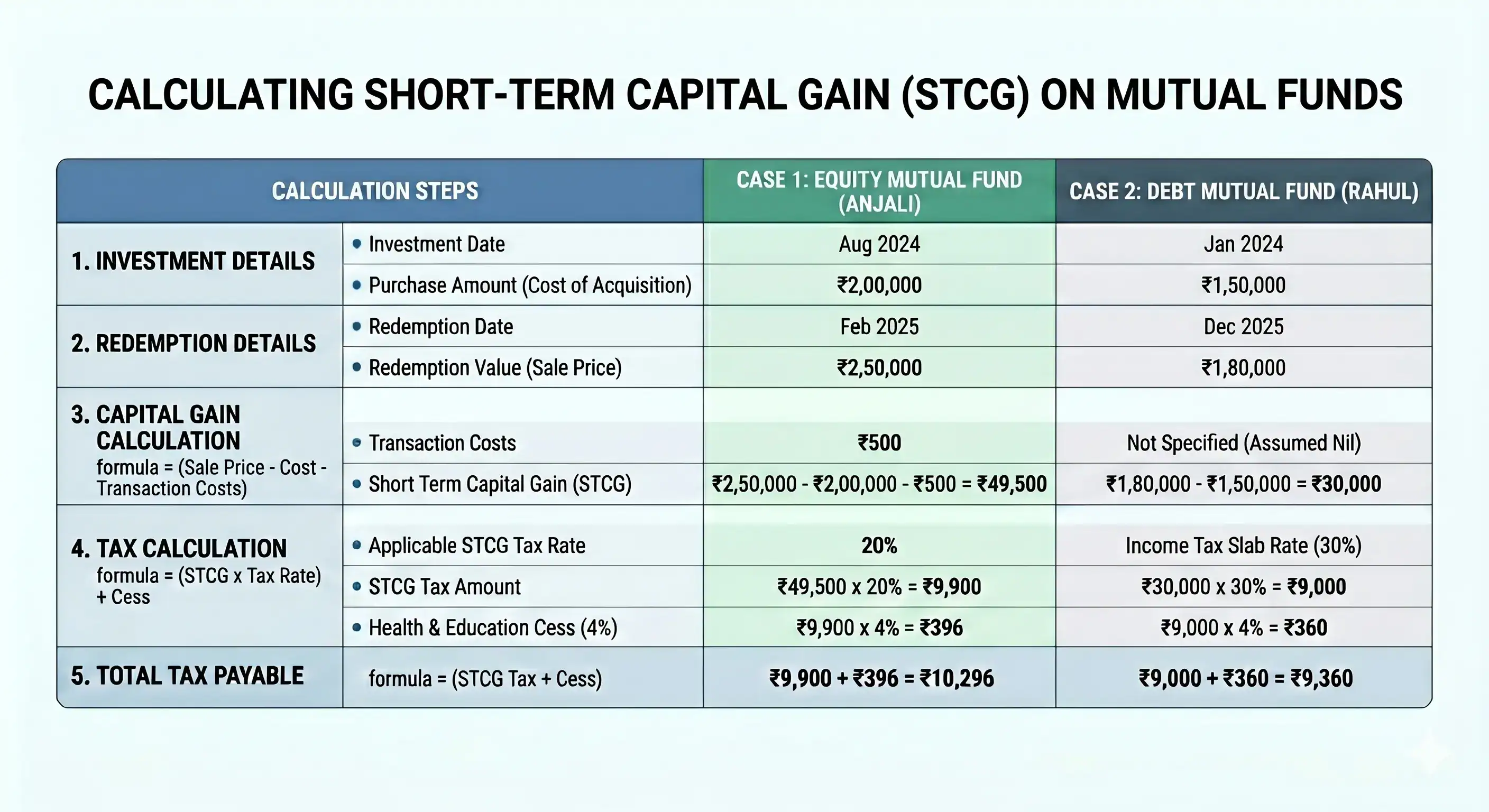

How to Calculate Short Term Capital Gain on Mutual Funds

STCG on mutual funds is calculated with the given formula:

STCG = Sale Value – Cost of Acquisition – Transaction Expenses

Case 1: Equity Mutual Fund

Anjali invested ₹2,00,000 in a large-cap fund in August 2024 and redeemed it in February 2025 for ₹2,50,000, with ₹500 in transaction costs. Her short-term capital gain works out to ₹49,500. At 20% STCG rate, her tax comes to ₹9,900. After adding 4% cess of ₹396, she has to pay a total tax of ₹10,296.

Case 2: Debt Mutual Fund

Rahul invested ₹1,50,000 in a debt fund in January 2024. He redeemed it in December 2025 for ₹1,80,000, giving him a gain of ₹30,000. Since his applicable slab is at 30%, his tax comes to ₹9,000. Adding 4% cess of ₹360 brings his total tax payable to ₹9,360.

The capital gain calculation outcome differs substantially between fund types, which is why knowing which category your fund falls into matters before you redeem.

Difference Between STCG and LTCG on Mutual Funds

The distinction between STCG and LTCG is at the heart of tax planning strategies India has exercised for mutual fund investors.

| Criteria | STCG | LTCG |

| Holding period (equity funds) | Up to 12 months | More than 12 months |

| Equity Funds | 20% flat | 12.5% above ₹1.25 lakh |

| Annual Exemption | None | ₹1.25 lakh per year |

| Debt Funds | Always STCG, slab rate | Not applicable |

Breaking this down further:

- Holding Period: For equity-oriented funds, the 12-month mark is the dividing line between STCG and LTCG. Crossing it meaningfully changes your tax rate.

- Equity Funds: The LTCG tax on equity funds (12.5%) is lower than 20% (STCG). This difference can turn into a substantial figure for larger redemptions.

- Exemption: LTCG on equity funds comes with a ₹1.25 lakh annual exemption; STCG has no such relief.

- Debt Funds: The gains on debt funds categorised as short-term and tax is levied on them at income slab rates.

How to Reduce or Save STCG Tax on Mutual Funds

While STCG cannot always be avoided entirely, there are several practical tax-saving tips that can help you minimise the liability.

- Extend the holding period: Holding the fund for even a few more weeks can shift your gain from short-term to long-term, giving you the benefit of lower tax rates.

- Offset gains with capital losses: If your portfolio has loss-making investments, you can redeem them to offset the losses against your STCG, reducing the taxable amount.

- Staggering redemptions: With a Systematic Withdrawal Plan (SWP), you can spread the redemptions across months or years. This lowers the tax hit in any single financial year.

- Consider ELSS funds: While Equity Linked Savings Scheme (ELSS) does not directly reduce your existing STCG, investing in them builds a long-term, tax-efficient corpus given their mandatory 3-year lock-in period.

Common Mistakes Investors Make with Mutual Fund Taxes

Many investors pay more STCG tax than necessary simply due to gaps in awareness.

- Treating the entire SIP as one investment: Each instalment has its own holding period. Redeeming the full SIP corpus early can mean several recent instalments attracting STCG.

- Ignoring fund switches: Switching from one scheme to another is treated as a redemption plus fresh purchase, even between Regular and Direct plans. This triggers STCG on the units switched out.

- Not accounting for exit loads: Beyond tax, redeeming early often attracts exit load charges that further reduce your net returns, a cost that compounds the STCG tax hit.

- Skipping reporting: STCG, dividends, and TDS credits all need to be declared under the relevant Income Tax Return (ITR) schedules. Omitting any of these can invite scrutiny.

Final Thoughts

STCG tax on mutual funds is no longer a minor footnote in your investment planning. As the rates and rules have shifted meaningfully, the holding period, redemption timing, and fund type all have a direct bearing on what you actually take home. A bit of foresight before redeeming tends to go a long way.

Frequently Asked Questions (FAQs)

No. Equity mutual funds redeemed within 12 months are now taxed at 20% after July 23, 2024, while debt fund gains are taxed as per slab rates.

You can legally reduce STCG tax by holding investments longer, using tax-loss harvesting, staggering withdrawals, and planning redemptions around exemption limits and tax slabs.

Yes. SIPs can attract STCG tax because each instalment is treated separately, and units redeemed before completing the required holding period become taxable.

Yes. ELSS funds attract STCG tax if redeemed after the mandatory 3-year lock-in but before qualifying for applicable long-term capital gains treatment.

Yes. Short-term capital losses can be adjusted against both STCG and LTCG in the same financial year, with unused losses carried forward for eight years.