The decisions regarding money or finances are mostly influenced by habits, family advice, social media chatter, and often, by half-understood ideas passed down over time. Many of these ideas unknowingly turn into personal finance myths that you should stop believing.

From assuming that saving alone guarantees security to believing that the stock market is no different from gambling, these notions can distort financial judgment. The result is not always immediate loss, but missed opportunities that compound over the years.

Which is why, this blog has been brought into effect to question widely accepted beliefs and place them against practical financial reasoning.

What Are Personal Finance Myths?

Personal finance myths are common beliefs about money that sound correct but are not entirely true. These ideas usually come from family advice, social media, or things people hear repeatedly over time. Because they are shared so often, they begin to feel like facts, even when they are not.

Myth 1: Saving Money Is More Important Than Investing

This is one of the most common personal finance myths you should stop believing. Saving money is important, but treating it as more important than investing can limit long-term financial growth.

While saving helps to preserve money, it does not grow it significantly. Additionally, inflation gradually reduces the time value of money, which means your purchasing power declines over time. Investing, on the other hand, allows money to grow through compounding.

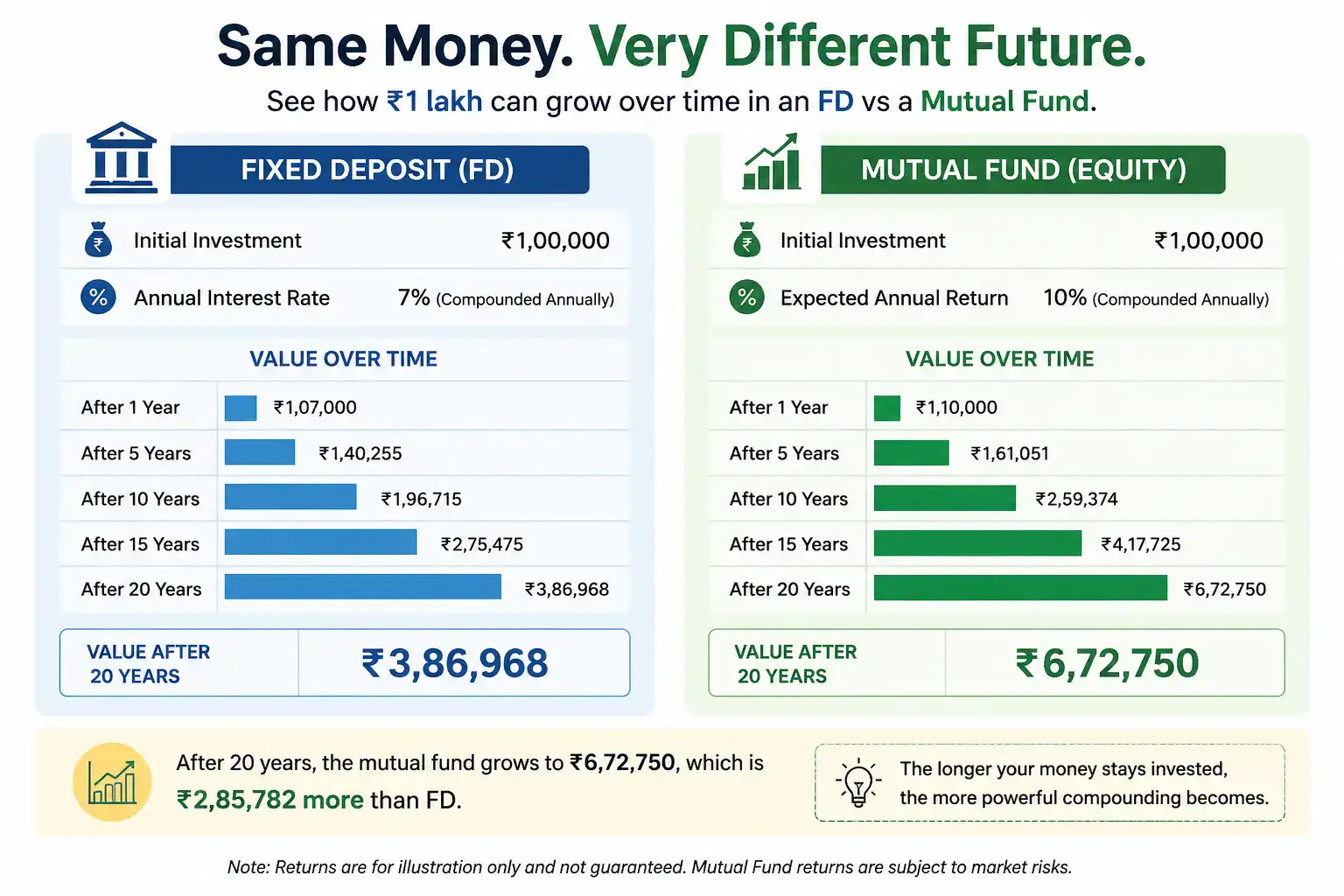

For this, a balanced approach could be keeping savings for short-term needs and emergencies, while investing for long-term goals. Let’s say you have ₹1 lakh in savings. See the potential growth comparison when you choose to open an FD or invest in mutual funds:

Myth 2: You Need a Lot of Money to Start Investing

Many people in India believe investing requires a large amount of money up front. This assumption discourages beginners, making them delay investing until they feel financially ‘ready’.

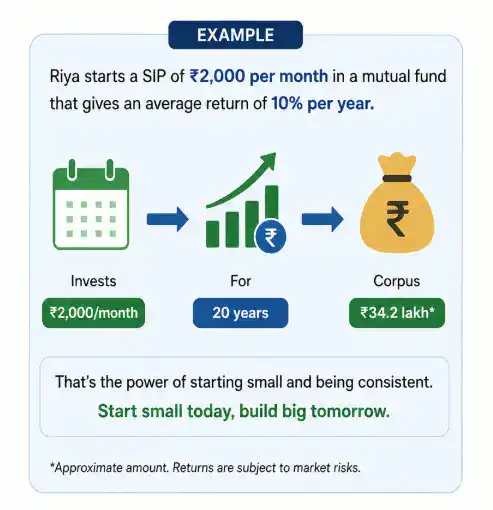

In reality, modern investment options allow individuals to begin with small amounts of even ₹100, for example, Systematic Investment Plans (SIPs).

Therefore, we should start with a small, regular investment and increase contributions gradually as income grows. Consistency is more important than the initial amount.

Myth 3: Credit Cards Always Lead to Debt

Credit cards are often seen as a path to debt. Most people believe that using a credit card automatically results in overspending and financial trouble. This perception comes from cases where poor repayment habits lead to high interest costs.

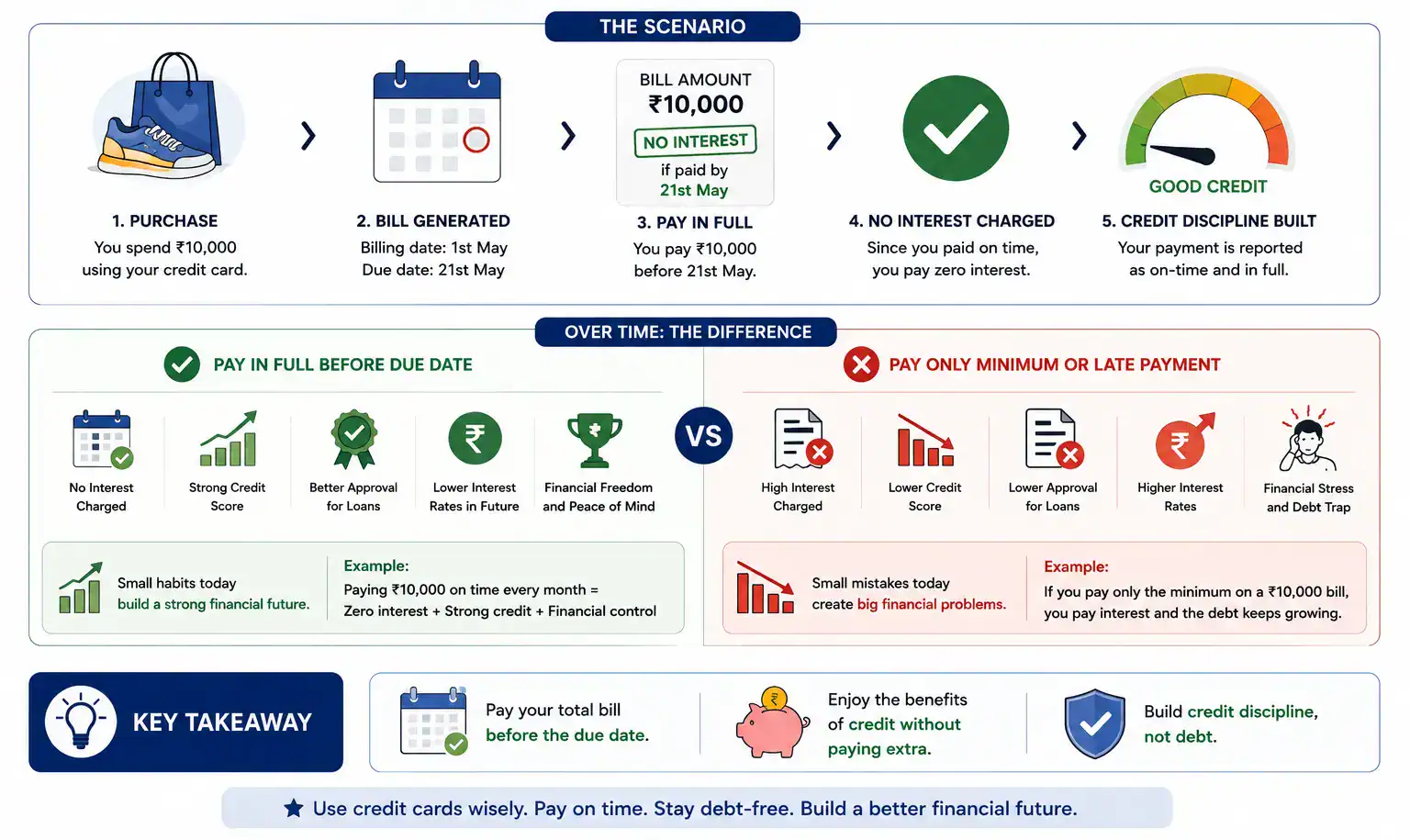

A credit card itself does not create debt. The debt arises when the balances are not paid on time. When used responsibly, credit cards offer an interest-free period and can help build a strong credit history. They also provide convenience and rewards.

The credit cards should be used as a payment tool rather than borrowed money. The users should maintain their spending within their ability to repay in full each month.

Myth 4: Renting is Always a Waste of Money

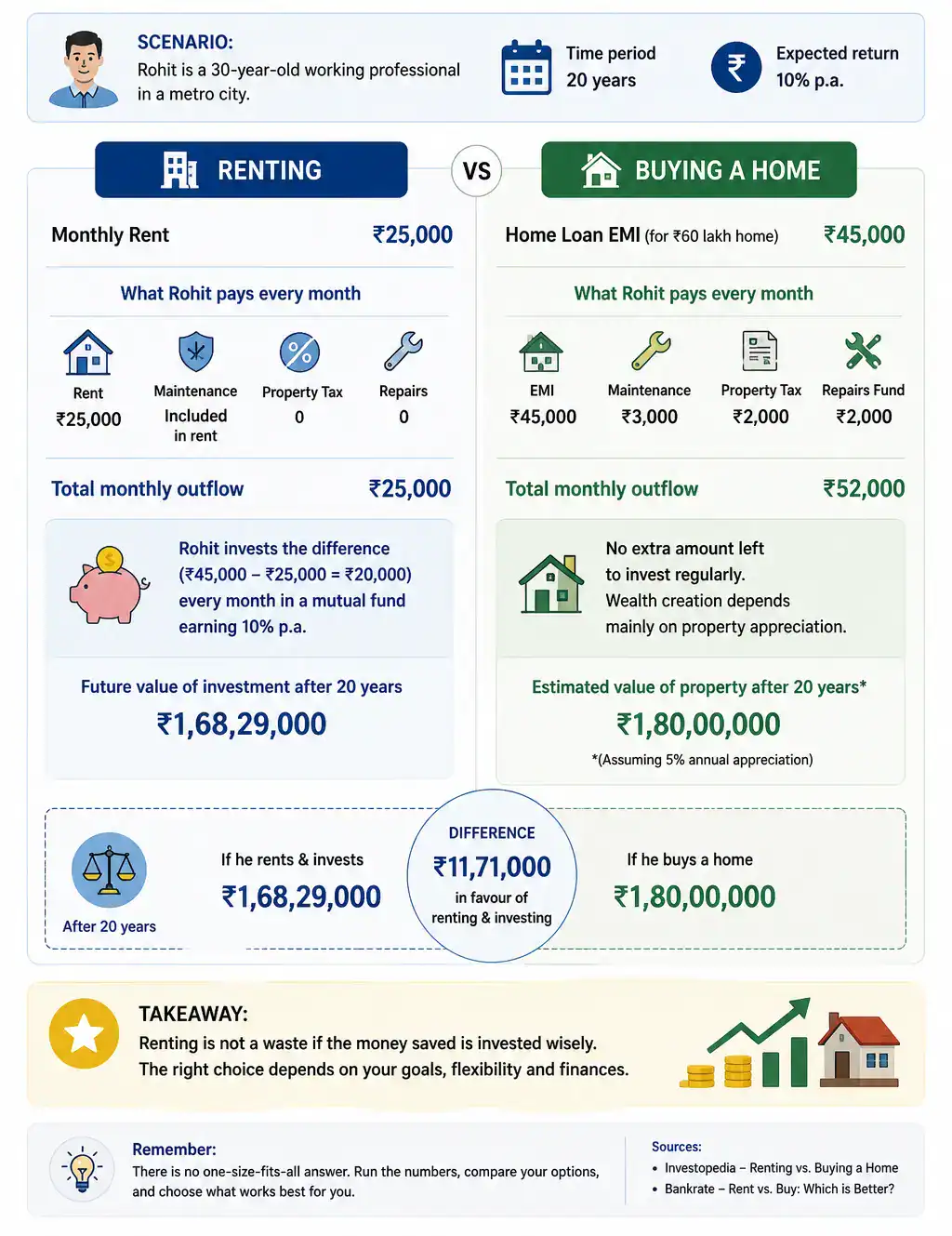

In most households, owning a home is seen as the only sensible financial goal. Rent, in comparison, is viewed as money that simply disappears each month without creating an asset. While home ownership can build long-term value, treating it as the default choice in every situation can lead to poor decisions.

Renting is usually more affordable in the short term, as it avoids high upfront costs such as down payments and registration charges. Ownership, on the other hand, brings ongoing expenses like maintenance and repairs.

The decision should be based on financial readiness, job stability, and long-term plans rather than a fixed belief.

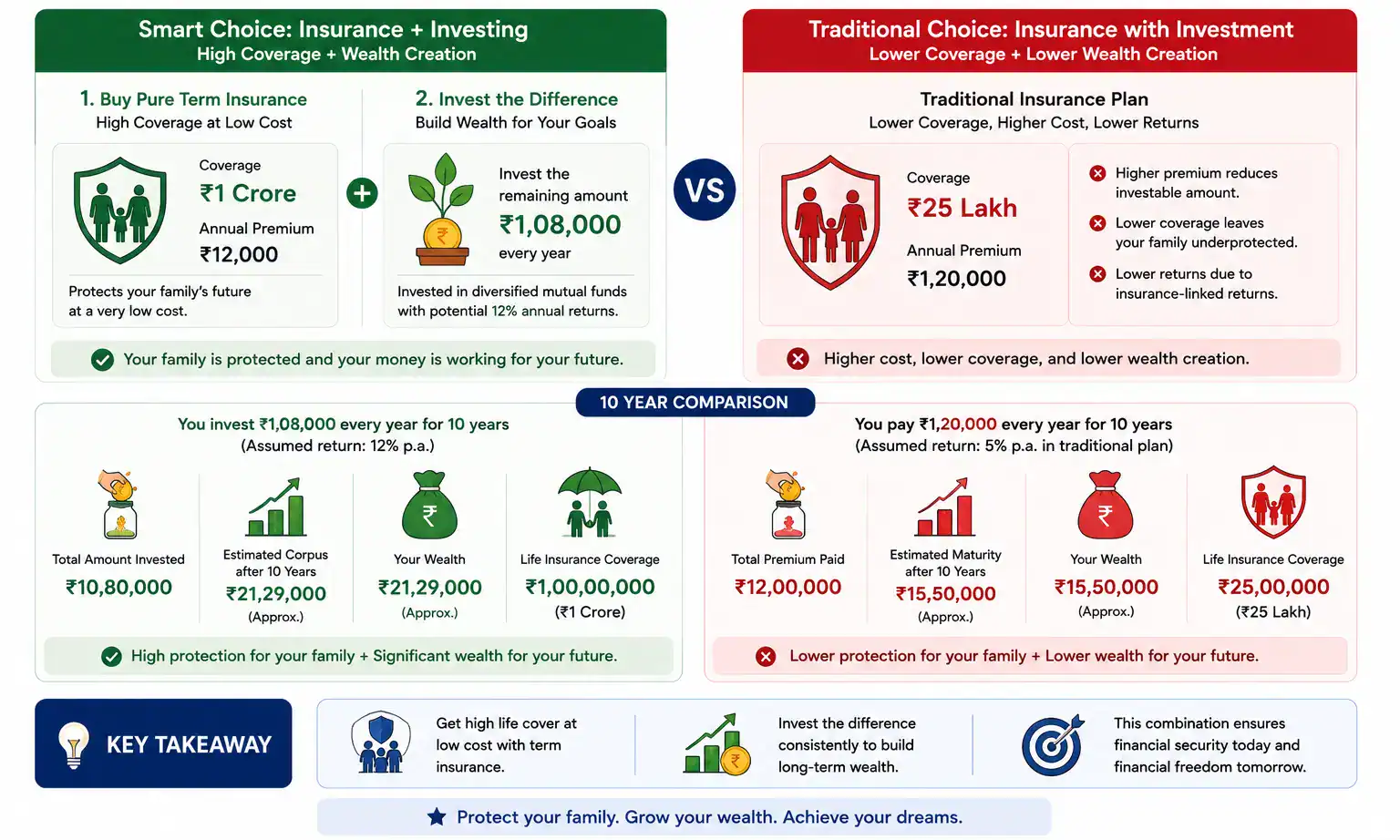

Myth 5: Insurance Is an Investment

In India, agents offer insurance plans as a promise for safety, guaranteed returns, and a payout at maturity. It sounds like a neat package, so insurance slowly gets viewed as an investment tool rather than a safety net.

In reality, insurance is designed to protect against financial loss, not to grow wealth. The returns from traditional policies are often modest and may struggle to beat inflation. Combining protection with investment usually leads to lower efficiency on both sides.

Myth 6: You Should Avoid All Debt

For some reason, debt is painted as something to be feared and avoided at all costs. The stories of loan defaults and rising interest burdens reinforce the idea that any form of borrowing is financially harmful.

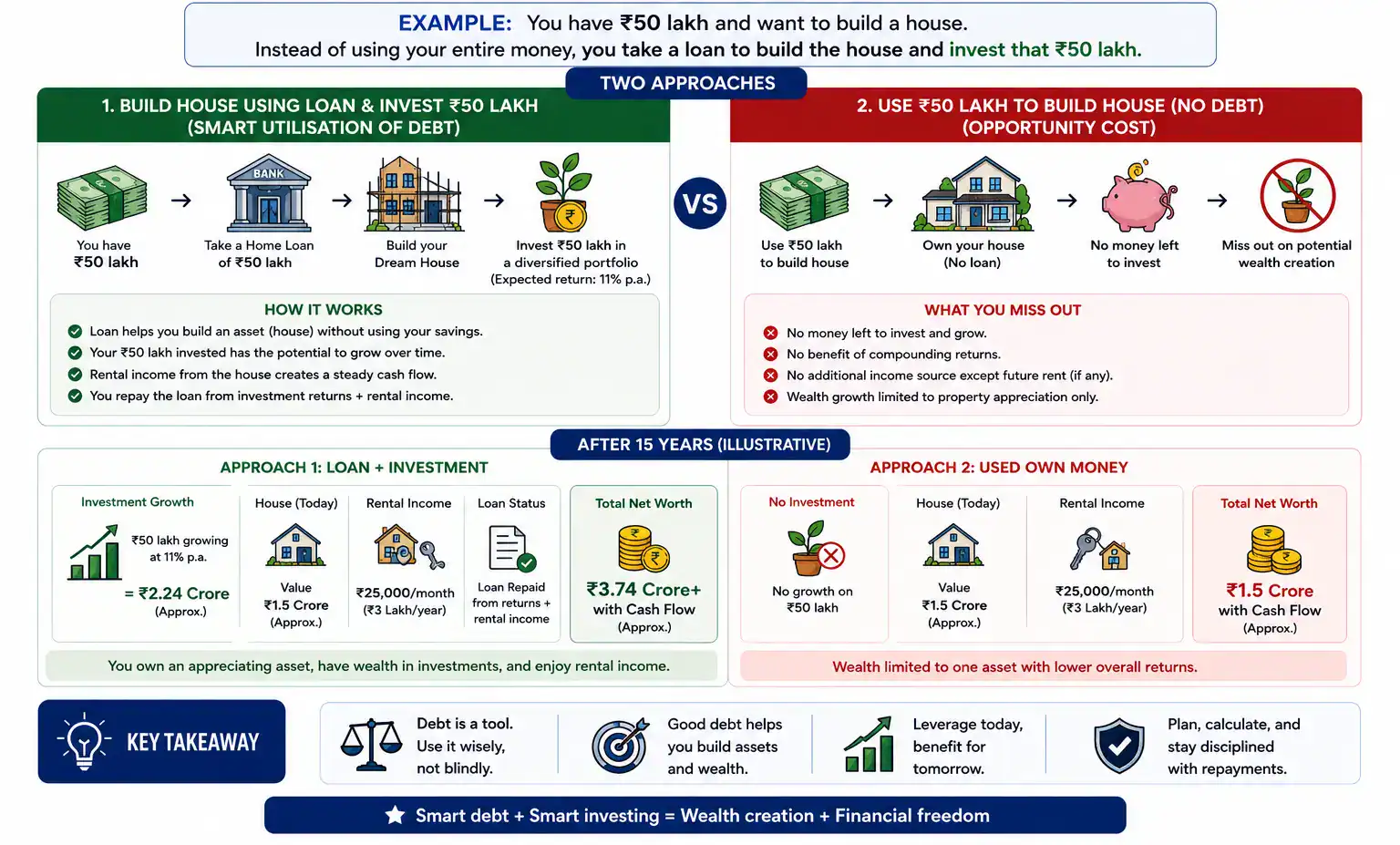

In reality, not all debt works against you. There is a clear difference between high-interest, short-term debt and borrowing that supports asset creation. Loans taken for education, business, or a reasonably priced home can contribute to long-term financial progress when managed carefully.

Consider a situation where you have ₹50 lakh and plan to build a house. Instead of using the entire amount upfront, you choose to take a home loan for construction while investing the ₹50 lakh in suitable instruments.

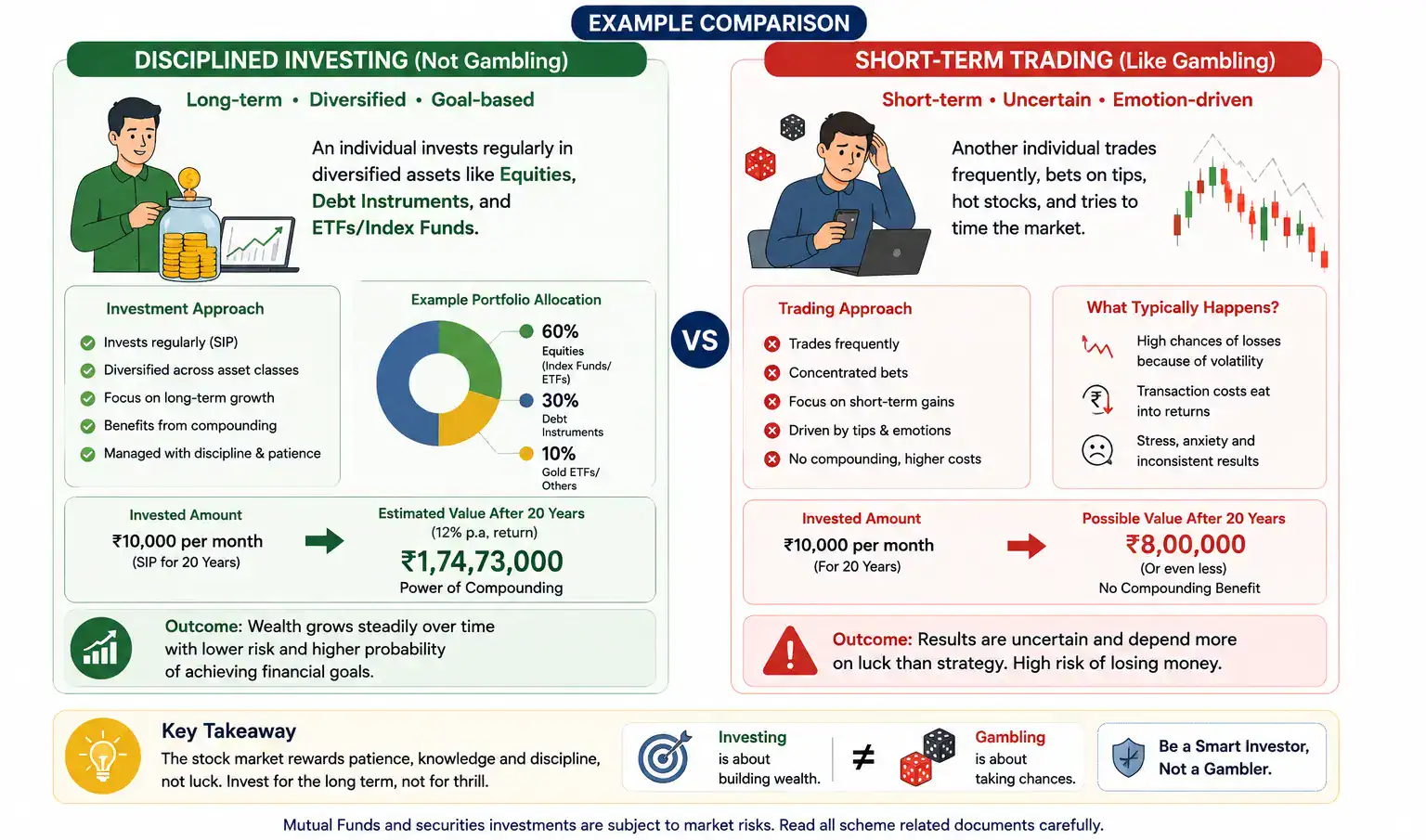

Myth 7: The Stock Market Is Gambling

When markets turn volatile, and losses make headlines, it is easy to misinterpret investing as a game of chance.

Gambling depends on chance, while investing in the stock market is based on research, business performance, and long-term growth. The companies generate earnings, expand operations, and create value over time. Investors who study fundamentals and remain patient are not relying on luck but on economic progress.

The market should be approached with knowledge and discipline, while focusing on long-term investing, diversifying across assets, and avoiding short-term speculation driven by emotions.

Myth 8: You Only Need Financial Planning Later in Life

Financial planning is often seen as something to consider once income stabilises or major responsibilities begin. The early years are treated as a phase for spending and experimentation, with planning postponed for ‘later’.

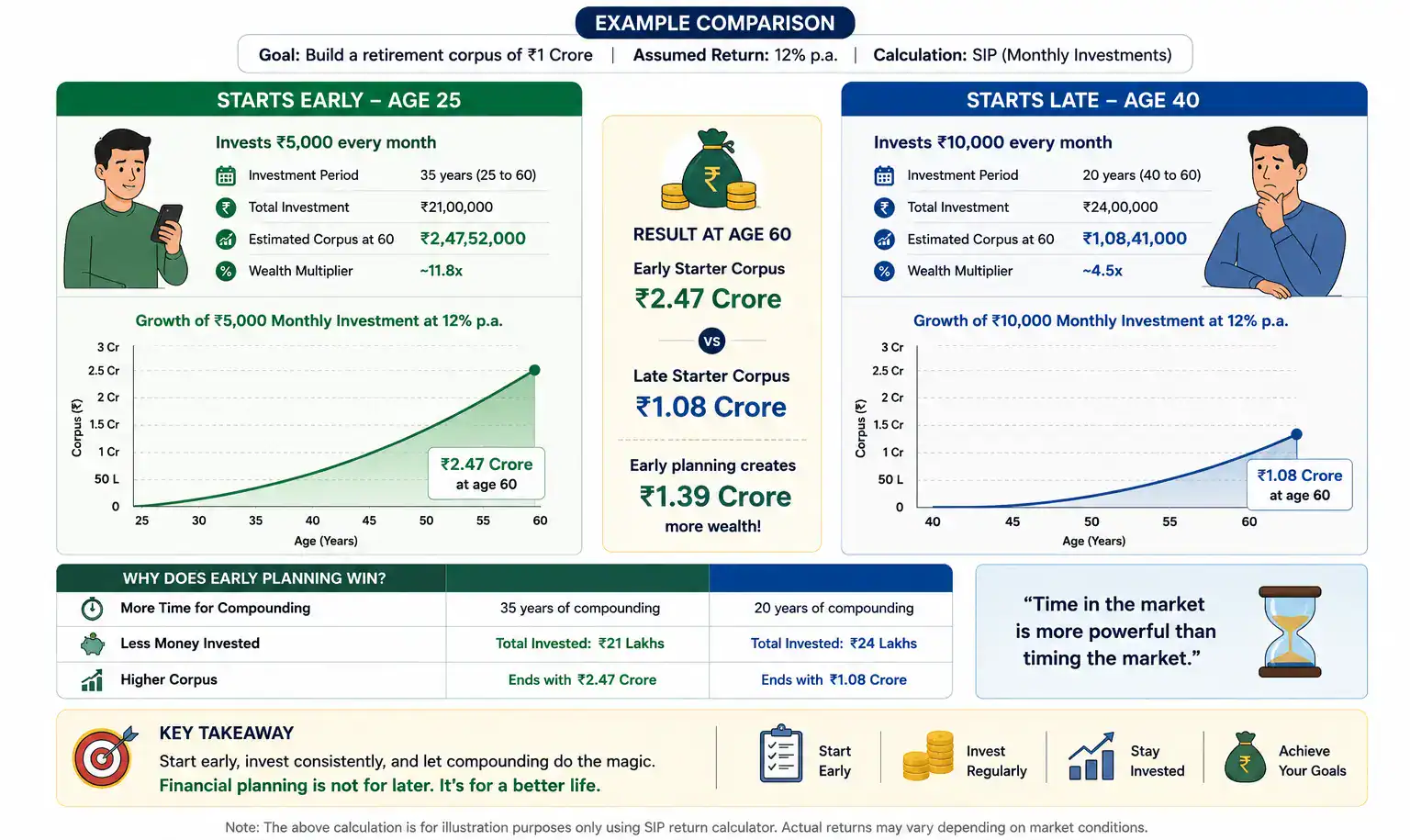

The major advantage young investors have is ‘Time’, which plays a decisive role in building wealth. Starting early allows even small amounts to grow through compounding, reducing the need for large contributions later. Delaying planning means nothing but playing catch-up, which requires higher savings and carries greater pressure.

Here is an example of two individuals, one who started at the age of 25 with a ₹5,000 investment per month and another who started at 40 with ₹10,000 every month.

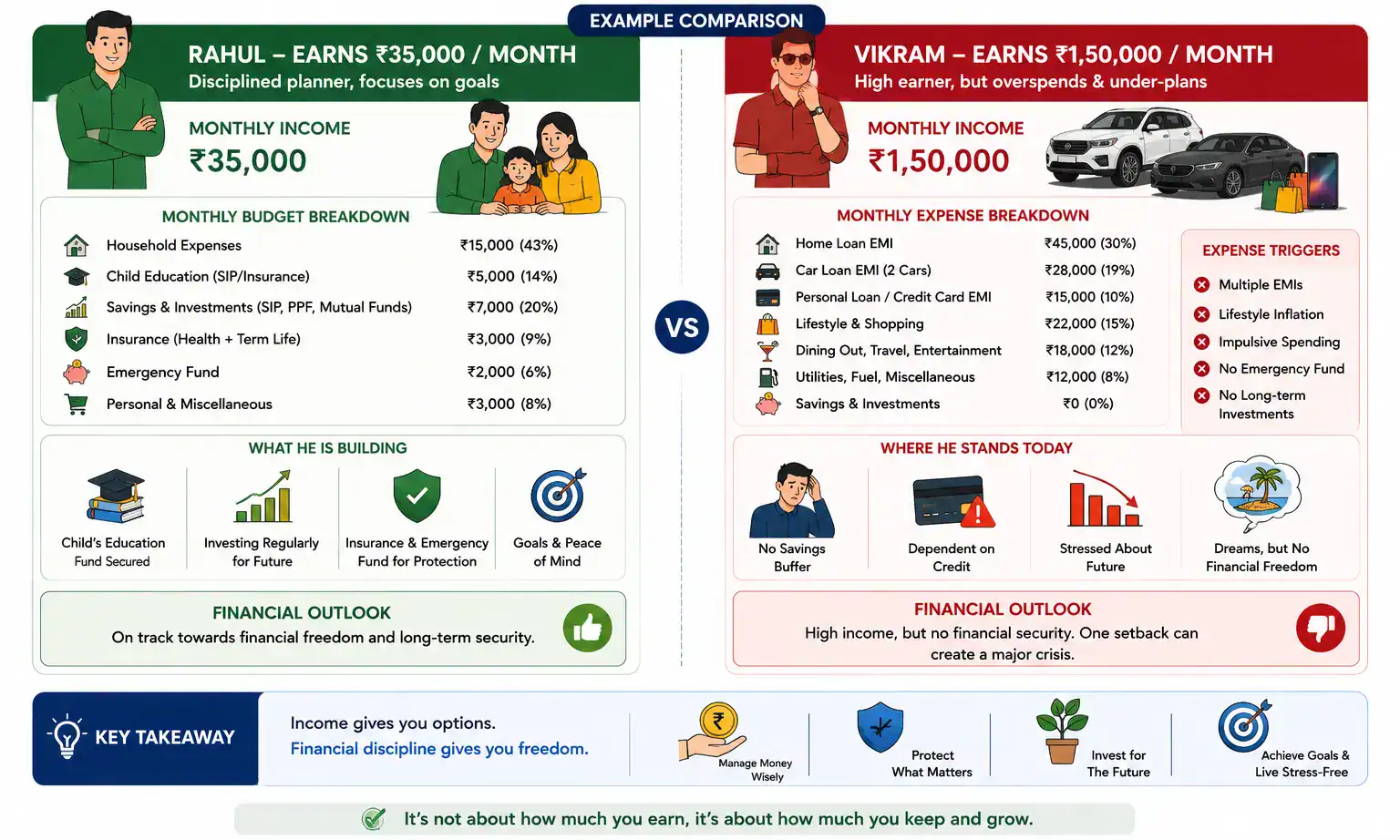

Myth 9: High Salary Means Financial Security

A higher or rising salary mostly creates the impression that financial security is automatically in place. The assumption is simple: earn more, and concerns related to money disappear. However, this belief tends to overlook how income is actually managed.

Financial security does not depend on just how much one earns, but on how much is saved, invested, and protected. The high income can easily be offset by lifestyle inflation, rising expenses, and lack of planning. Without disciplined money management, even a strong salary might fail to translate into long-term stability.

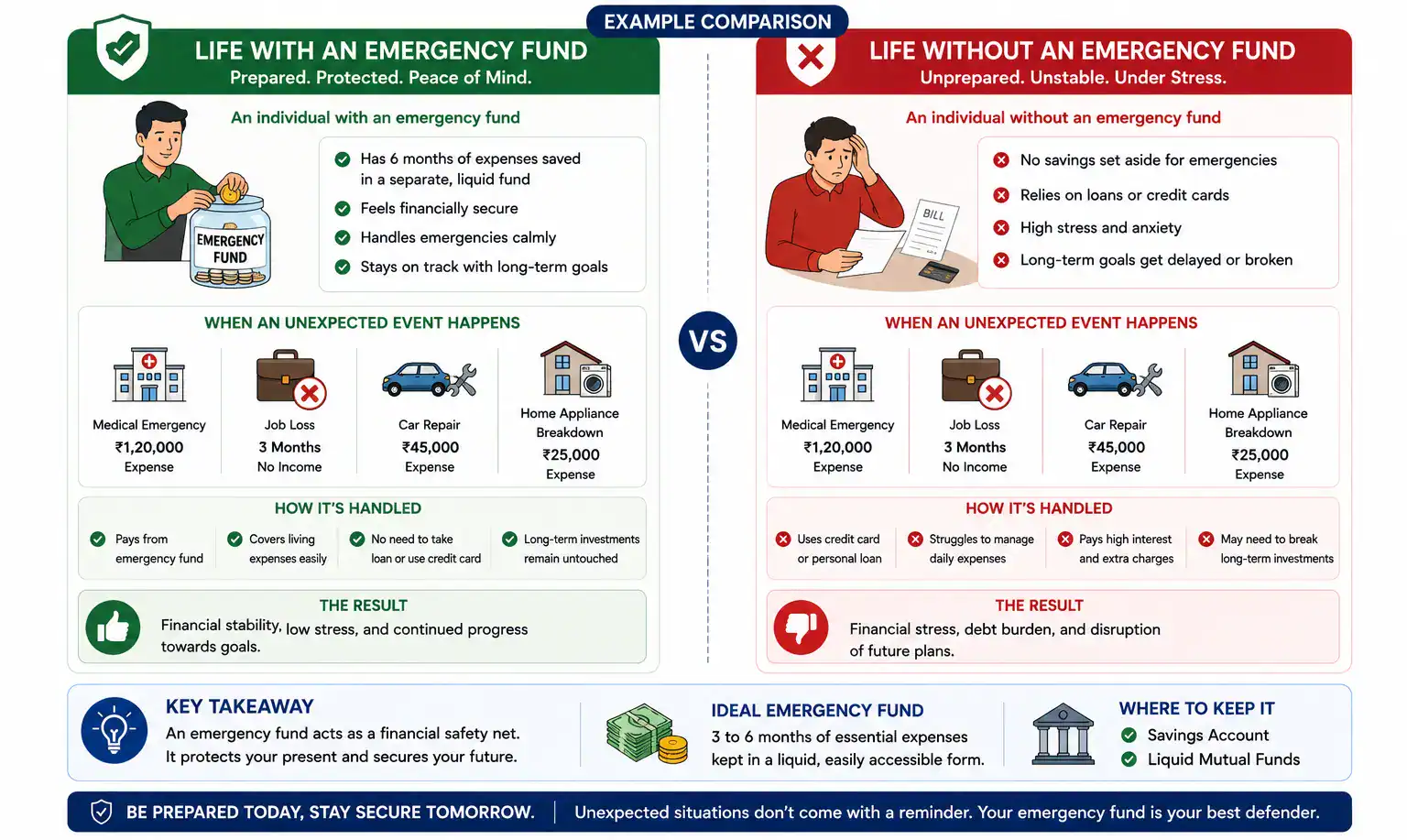

Myth 10: You Don’t Need an Emergency Fund

When income is stable and expenses are predictable, setting aside money for emergencies might feel unnecessary. Many assume that savings or credit options can handle any unexpected situation when it arises.

However, unexpected events such as medical expenses, job loss, or urgent repairs rarely come with warning. Without a dedicated emergency fund, individuals are forced to rely on high-interest debt or disturb long-term investments. This can create financial stress and disrupt future plans.

Therefore, building an emergency fund should be treated as a priority. Ideally, setting aside six months to 1 year of essential expenses in a liquid and easily accessible form provides a financial buffer.

Common Reasons Why People Believe These Myths

These beliefs did not appear out of nowhere. Over time, they have been shaped slowly through repetition, familiarity, and limited financial awareness.

- Inherited beliefs: Financial habits are passed down through families, where advice is based on past experiences rather than current realities.

- Social influence: Conversations with peers and content on social media can reinforce simplified or misleading money ideas.

- Lack of financial literacy: Without basic financial knowledge, it becomes difficult to question or verify commonly accepted beliefs.

- Emotional decision-making: The fear of loss and preference for safety have led individuals to accept ideas that feel secure rather than logical.

- Selective examples: People tend to remember extreme success or failure stories, which distorts a balanced understanding of financial decisions.

How to Build a Strong Personal Finance Mindset?

Once these myths are recognised, the next step is not just correction, but building a mindset that supports consistent and informed financial decisions. A strong financial mindset is built through clarity, discipline, and consistency, allowing individuals to make decisions that support long-term stability and growth.

- Clarity of goals: Financial decisions become easier when there is an understanding of short-term needs and long-term objectives.

- Habit over income: Consistent saving and investing habits are more important than income levels in building lasting financial strength.

- Informed decision-making: Individuals should rely on verified information rather than assumptions, which helps to avoid costly mistakes over time.

- Balance between risk and safety: A thoughtful mix of protection, savings, and investments can create both stability and growth.

- Long-term perspective: Patience and consistency allow compounding to work effectively, reducing the impact of short-term market movements.

Final Thoughts:

The decisions regarding finances fail because they are built on assumptions that appear familiar but lack depth. The shift, therefore, is not about rejecting everything you have heard, but about questioning it.

In the end, personal finance is about disciplined behaviour rather than complex strategies. The sooner these myths are replaced with practical understanding, the stronger and more stable your financial journey becomes.