India’s evolving infrastructure and construction story extends far beyond sheer volume growth in basic building materials. The real opportunity lies in the rapid modernization of building practices, as developers and architects increasingly trade up to versatile, sustainable, and aesthetically pleasing structural steel tubes.

As government capital expenditure accelerates, urbanization demands faster project turnarounds, and eco-friendly construction practices gain traction, modern tubular steel is rapidly capturing value share from traditional materials like concrete, wood, and conventional steel sections. In this backdrop, APL Apollo Tubes Ltd. has emerged as India’s undisputed leader in the structural steel tubing market, driving industry innovation with a rapidly growing, high-margin portfolio of value-added and heavy structural products.

But does APL Apollo Tubes Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | APLAPOLLO |

| Industry/Sector | Steel and Iron Products |

| CMP | 1872.50 |

| Market Cap (₹ Cr.) | 51,525 |

| P/E | 43.16 (Vs Industry P/E of 43.97) |

| 52 W High/Low | 2301.40 / 1492.00 |

| EPS (TTM) | 43.33 |

| Dividend Yield | 0.45% |

About APL Apollo Tubes Ltd.

Headquartered in the Delhi-NCR region, APL Apollo Tubes Limited is a premier manufacturer of branded steel products in India. The company operates 10 sophisticated manufacturing facilities, producing an extensive portfolio of over 1,500 variants, including MS Black Pipes, structural ERW steel tubes, and hollow sections, tailored for diverse sectors such as urban infrastructure, modern housing, solar energy, and large-scale engineering projects.

Key business segments

APL Apollo Tubes Ltd. maintains its market leadership through several core operational verticals:

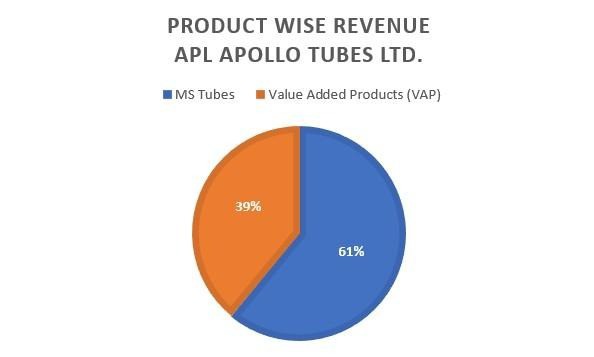

- High-Margin Value-Added Portfolio: Focusing on corrosion-resistant innovations such as Apollo Z pre-galvanised tubes and Apollo Tricoat, catering to high-end architectural aesthetics.

- Infrastructure & Heavy Structural: Deploying superior strength, large-scale Apollo Column solutions for iconic developments, including airports and advanced pre-engineered structures.

- Volume-Driven General Structural: Capturing mass-market demand through a robust supply of hollow steel sections for residential and commercial engineering projects.

- Modern Building Solutions: Driving material substitution with contemporary steel alternatives like Apollo Chaukhat, designed to replace traditional wood in door and window frames.

- Agri & Essential Plumbing: Supporting critical water transportation and irrigation sectors with a durable range of black steel and hot-dipped galvanized pipes.

Primary growth factors for APL Apollo Tubes Ltd.

Key growth factors for APL Apollo Tubes Ltd.:

- Accelerating Value-Addition: Leveraging the structural shift in real estate and infrastructure toward modern, corrosion-resistant, and aesthetically versatile steel tubing solutions.

- Strategic Portfolio Rebalancing: Driving margin expansion by prioritising high-end Value-Added Products (VAP), including Apollo Z and Apollo Tricoat, over conventional volume-led commodity segments.

- Supply Chain & Manufacturing Synergies: Optimising operational yields through a sophisticated, decentralised pan-India manufacturing footprint that enhances logistical efficiencies and raw material procurement.

- Pioneering Niche Verticals: Capturing long-term market share by scaling innovative building materials like Apollo Column and Apollo Chaukhat, designed to replace traditional concrete and wood.

- Regional & Global Proliferation: Scaling its formidable distribution network to deepen presence in domestic tier-2/3 markets and accelerate growth across high-potential international geographies.

Detailed competition analysis for APL Apollo Tubes Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| APL Apollo Tubes Ltd. | 23079.00 | 1801.82 | 7.81% | 1203.08 | 5.21% | 43.16 |

| Shyam Metallics Ltd. | 18,552.21 | 2333.04 | 12.58% | 1060.07 | 5.71% | 25.49 |

| Welspun Corp Ltd. | 16770.14 | 2235.64 | 13.33% | 1278.15 | 7.62% | 23.13 |

| Jindal Stainless Ltd. | 42954.66 | 5560.43 | 12.94% | 3167.84 | 7.37% | 18.04 |

| JSW Steel Ltd. | 185470.00 | 29821.00 | 16.08% | 25983.00 | 14.01% | 12.35 |

Key insights on APL Apollo Tubes Ltd.

- Dominant Market Leadership: The company commands a formidable presence in the domestic structural steel tubing landscape, securing a market share exceeding 50%.

- Unparalleled Pan-India Presence: Utilising a sophisticated decentralised manufacturing network and a deep multi-tier distribution engine to ensure comprehensive nationwide reach.

- Capitalising on Modernisation: Strategically positioned to benefit from surging government infrastructure spending and a structural shift toward sustainable, tubular-led construction practices.

- Premium Portfolio Expansion: Aggressively scaling its Value-Added Products (VAP) vertical to enhance structural margins and distance itself from commoditised market alternatives.

- Diversified Revenue Streams: Maintaining operational resilience through broad exposure across residential housing, commercial real estate, agriculture, and high-scale industrial projects.

- Lucrative Global Acceleration: Fueling long-term growth through disciplined capacity expansion and a high-margin export strategy, particularly across high-potential Middle Eastern geographies.

- Technological Innovation: Prioritizing cutting-edge advancements like Direct Forming Technology (DFT) to pioneer niche building solutions and specialized structural offerings.

Recent financial performance of APL Apollo Tubes Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 5509.00 | 5982.00 | 6269.00 | 4.80% | 13.80% |

| EBITDA (₹ Cr.) | 414.00 | 472.00 | 511.00 | 8.26% | 23.43% |

| EBITDA Margin (%) | 7.51% | 7.89% | 8.15% | 26 bps | 64 bps |

| PAT (₹ Cr.) | 293.00 | 310.00 | 354.00 | 14.19% | 20.82% |

| PAT Margin (%) | 5.32% | 5.18% | 5.65% | 47 bps | 33 bps |

| Adjusted EPS (₹) | 10.56 | 11.17 | 12.76 | 14.23% | 20.83% |

APL Apollo Tubes Ltd. financial update (Q4 FY26)

Financial performance:

- Top-line Momentum: Operational revenue reached ₹6,269 Crores, marking a healthy 13.80% YoY expansion and 4.80% sequential growth, fueled by strong domestic appetite and a higher mix of premium Value-Added Products.

- Operational Efficiency: EBITDA surged 23.43% YoY to ₹511 Crores, supported by an optimised brand portfolio and logistical synergies across its decentralised manufacturing footprint.

- Margin Progression: Operating margins improved to 8.15%, reflecting a 64 bps YoY recovery as the company continues to distance itself from commoditised segments.

- Bottom-line Strength: Reported PAT climbed 20.82% YoY to ₹354 Crores, demonstrating robust earnings compounding and a solid 14.19% rebound from the preceding quarter.

- Shareholder Value: EPS expanded to ₹12.76, highlighting underlying resilience and the successful scaling of its undisputed market leadership in the structural tubing landscape.

Key business highlights

- Record-Breaking Portfolio Momentum: The company registered unprecedented quarterly volumes of 924,881 tons during Q4 FY26, underpinned by a structural pivot toward high-margin segments that propelled EBITDA per ton to a historic peak of ₹5,525.

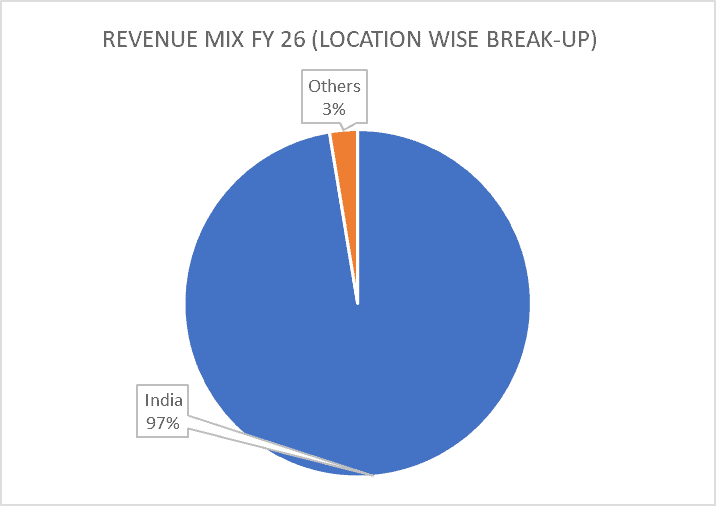

- Global Footprint Acceleration: Strengthening its international presence, the group exports specialised structural steel solutions to more than 20 countries, supported by a state-of-the-art UAE facility with a 0.4 million MTPA capacity tailored for global markets.

- Unrivalled Distribution Engine: Leveraging a formidable three-tier network, APL Apollo maintains deep nationwide penetration across 800 distributors, 50,000 retail touchpoints, and 200,000 fabricators, managed through 29 regional branch offices.

- Strategic Premiumization Focus: Prioritising margin-accretive growth over commodity volumes, the company is aggressively scaling high-value verticals such as Apollo Structural, Apollo Z rust-proof tubes, and specialised coated products.

- Infrastructural Scaling Roadmap: A multi-year expansion strategy is underway to elevate annual installed capacity to 5 million tons, featuring new localised manufacturing hubs in East India and Bangalore to optimise logistical yields and structural costs.

Future growth outlook

- Ambitious Volume & Revenue Targets: Management anticipates a robust double-digit volume expansion of 10-15% CAGR over the coming three to four years, supported by a strategic roadmap to scale total annual capacity to 10 MTPA by FY30.

- Profitability & Margin Roadmap: By optimising operational yields and enriching the product mix, the group aims to achieve industry-leading EBITDA benchmarks of ₹5,500 to ₹6,000 per ton, pivoting from volume-led growth toward sustained bottom-line strength.

- Accelerated Premiumization Momentum: The company is targeting a dominant 70% volume contribution from its high-margin Value-Added Products (VAP) vertical, capitalising on the structural consumer migration toward modern, aesthetic, and corrosion-resistant building solutions.

- High-Yield Category Penetration: Deepening its presence in specialized segments like solar tracker structures, while broadening its global and domestic reach through localised East India expansions and a high-potential export strategy via its Dubai hub.

- Resilient Structural Foundation: Strong infrastructure appetite, a shift away from unorganised secondary players, and superior operating cash flow generation provide a solid floor for disciplined, self-funded capacity growth.

Recent developments – APL Apollo Tubes Ltd.

- Strategic Product Premiumization: Aggressively deploying high-margin innovations, including massive 1000x1000mm structural sections, specialised solar tracker components, and advanced rust-proof solutions to drive margin expansion.

- Record-Breaking Operational Milestones: Capitalising on robust domestic infrastructure appetite to achieve a formidable 5 MTPA installed capacity, while propelling EBITDA per ton to an unprecedented peak of ₹5,525 during Q4 FY26.

- Pan-India Capacity Scaling: Strengthening the group’s decentralised manufacturing engine through strategic debottlenecking and high-impact greenfield expansions across Bhuj, New Malur, and Gorakhpur hubs.

- High-Tech Segment Penetration: Pioneering niche structural verticals by targeting super-speciality applications across high-growth sectors, including aerospace, electric vehicles, and the oil and gas landscape.

- Global Footprint Proliferation: Accelerating international growth through a high-capacity Dubai manufacturing base and a robust European logistical network featuring key distribution warehouses in Antwerp and Liverpool.

Company Valuation Insights: APL Apollo Tubes Ltd.

At present, APL Apollo Tubes Ltd. commands a TTM P/E valuation of nearly 43.2x, representing a premium over the peer group median of 42.9x. This elevated rating underscores investor confidence in the group’s aggressive shift toward value-addition and premiumized product verticals. Over the preceding twelve months, the stock has demonstrated formidable structural resilience, outperforming conventional commodity-led steel peers despite a backdrop of macroeconomic volatility and fluctuating input costs.

The fundamental investment case is anchored by the company’s unrivalled dominance in India’s structural steel tubing landscape and a rapidly proliferating global footprint. Utilizing an expansive distribution engine of 50,000 retail touchpoints, the group is capturing market share by leveraging powerful tailwinds, including surging government infrastructure outlays, accelerating urbanisation, and a structural migration toward sustainable, tubular-led building practices. Growth is expected to be propelled by the high-margin Value-Added Products (VAP) vertical, supported by a robust appetite for specialised Apollo Z rust-proof tubes, colour-coated solutions, and heavy structural sections. By pioneering Direct Forming Technology (DFT), management is prioritising margin-accretive expansion through an enriched mix and specialised niche offerings like heavy industrial columns. Furthermore, a disciplined capacity scaling roadmap, featuring new localised hubs in East India and a state-of-the-art Dubai facility, is set to optimise logistical yields and structural efficiencies. With an undisputed 55% domestic market share, exports reaching diverse international geographies, and a superior three-year average ROCE of 21.5%, APL Apollo remains perfectly positioned to capitalize on India’s multi-year modernization narrative.

Reflecting anticipated earnings compounding and volume acceleration for FY27, we maintain a 3-month base-case target price of ₹2,000, implying a potential upside of 6% from the current market price. Our 12 month target is at ₹2,320 (24% upside), contingent on sustained momentum within the premium portfolio, enhanced operating leverage as installed capacity scales toward 5 MTPA, and deepened global penetration via its Middle Eastern manufacturing hub.

Potential risk factors for APL Apollo Tubes Ltd.

- Raw Material Price Sensitivity: Significant fluctuations in Hot Rolled Coils (HRC) pricing and supply chain constraints for essential inputs remain primary threats to operational margins and inventory valuations.

- Fragmented Market Rivalry: Navigating a highly competitive landscape against unorganised local players, regional manufacturers, and major steel producers aggressively expanding their tubular footprints.

- Systemic & Policy Exposures: Operational performance is sensitive to shifts in government infrastructure capital outlays, domestic tariff adjustments, and increasingly stringent environmental manufacturing mandates.

- Execution of Premium Pivot: Effectively converting traditional engineering preferences toward high-margin innovations like Apollo Chaukhat and heavy columns across inherently conservative construction segments.

- Capacity Scaling Risks: Managing potential timeline slippages or cost escalations during the rollout of multi-year greenfield and brownfield capacity expansions across domestic and international territories.

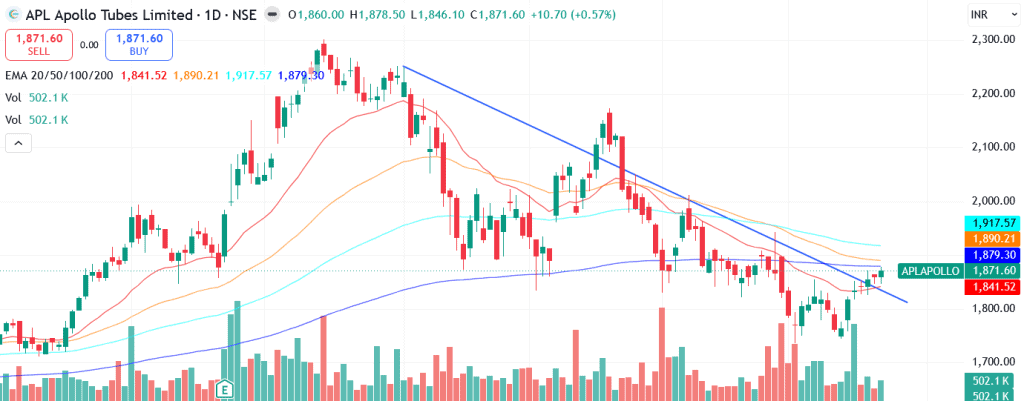

Technical analysis of APL Apollo Tubes Ltd.

APL Apollo Tubes is currently undergoing a phase of consolidation after a prolonged correction, but the stock appears to be stabilizing near an important support zone with technical indicators showing early signs of improvement. The stock has moved above its 20-day EMA and is approaching a potential crossover above its 50-day EMA, indicating that near-term momentum is gradually turning positive. While the broader trend remains corrective, sustained price action above key support levels could offer an attractive entry opportunity for investors looking to participate in the next leg of the recovery. A decisive breakout above ₹2,000 could act as the next trigger for renewed buying interest and pave the way towards ₹2,320, in line with our 12-month fundamental target.

Momentum indicators suggest improving technical conditions. The MACD at -14.81 remains in negative territory but has recently crossed above its signal line, indicating a positive momentum shift and the possibility of a trend reversal. The RSI at 53.74 reflects healthy buying interest and suggests that the stock has regained neutral-to-positive momentum after an extended period of weakness. Additionally, the Relative RSI over the 21-day and 55-day periods stands at -0.01 and -0.10 respectively, indicating mild underperformance against the broader benchmark, although the relative strength trend has been steadily improving in recent weeks.

Trend strength remains modest, with the ADX at 15.21 indicating a range-bound market rather than a strong directional trend. However, if the stock continues to respect its support zone and successfully breaks above key resistance levels, trend strength could improve significantly and attract incremental participation. A sustained move above ₹2,000 would strengthen the bullish case and increase the probability of a medium-term uptrend. On the downside, ₹1,740 remains a critical support level and serves as an important stop-loss level for the bullish view.

- RSI: 53.74 (Decent buying interest)

- ADX: 15.21 (Range Bound)

- MACD: -14.81 (Negative; above signal line)

- Resistance: ₹2,000

- Support: ₹1,740

APL Apollo Tubes Ltd. stock recommendation

Current Stance: Buy, with a 3-month target price of ₹2,000 (6% upside) and a 12-month target price of ₹2,320 (24% upside).

Why buy now?

Rising investments in infrastructure, real estate, warehousing, renewable energy, industrial construction and urban development continue to support long-term demand for structural steel tubes in India.

APL Apollo remains the market leader in structural steel tubes with an extensive manufacturing footprint, strong distribution network and significant scale advantages over peers.

The company's increasing focus on value-added products, heavy structural tubes and branded offerings is expected to support margin expansion and improve profitability over time.

Continued substitution of conventional steel sections, wood and concrete with advanced tubular solutions is creating a large structural growth opportunity for the industry.

Capacity expansion initiatives, operational efficiencies and deeper penetration into under-served markets position the company to capture a larger share of India's evolving construction ecosystem.

Improving demand from infrastructure, housing and industrial capex, coupled with the company's strong execution capabilities, provides visibility for sustainable earnings growth over the medium to long term.

Portfolio fit

APL Apollo Tubes offers exposure to India's infrastructure, urbanisation and industrial growth themes through its leadership in the structural steel tubing market. Supported by a strong brand, nationwide distribution network, expanding value-added product portfolio and favourable industry tailwinds, the company is well positioned to benefit from rising steel tube adoption across construction and infrastructure projects, making it a suitable addition to growth-oriented portfolios.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebBudget 2026-27 Opportunities: APL Apollo Tubes Ltd.

- Enhanced Fiscal Efficiency & Reinvestment: The strategic reduction of the MAT benchmark to 14% significantly amplifies net profitability, unlocking vital internal liquidity to accelerate the group’s ambitious multi-year capex strategy, cutting-edge technology integration, and its roadmap to surpass 5 MTPA in annual capacity.

- Logistic Synergies & Project Pipelines: Robust sovereign outlays for high-impact transportation networks and urban transit corridors are set to optimize logistical yields for heavy structural movements, while catalysing a formidable institutional pipeline for specialised, large-scale Apollo Column solutions.

- Urbanisation & Premium Migration: Sustained policy impetus for modern residential and commercial development provides a resilient demand floor, propelling the structural shift toward high-margin, corrosion-resistant, and aesthetically versatile tubular alternatives over conventional building materials.

- Ancillary Ecosystem Strengthening: Targeted manufacturing incentives for the MSME landscape fortify the broader supply chain, delivering direct operational and financial tailwinds to APL Apollo’s unrivalled domestic engine of over 200,000 certified fabricators and retail partners.

- Global Distribution & Trade Corridors: Constructive international trade frameworks and optimised cross-border logistics perfectly complement the company’s aggressive global proliferation via its state-of-the-art Dubai manufacturing hub, reinforcing its commitment to high-margin international branding.

Final Thoughts

APL Apollo Tubes Limited remains uniquely situated at the intersection of powerful structural tailwinds, capitalising on India’s multi-year infrastructure modernisation, a structural pivot toward pre-engineered architectural designs, and the surging real estate appetite for sustainable building solutions. Commanding an unrivaled 55% domestic market share and an expanding vertical of high-margin Value-Added Products (VAP), the group utilises its formidable nationwide distribution engine to anchor its leadership across India’s evolving construction landscape. Moreover, its commitment to pioneering Direct Forming Technology (DFT) and a decentralised manufacturing footprint ensures sustainable cost advantages and unmatched operational resilience.

For long-term investors seeking exposure to the nation’s secular infrastructure narrative and the lucrative transition toward specialised engineering solutions, APL Apollo offers a compelling investment case. The company’s unique blend of undisputed market dominance, improving operational benchmarks, and a highly scalable, self-funded roadmap provides a robust foundation for consistent earnings compounding and significant shareholder value creation.