India’s hospitality sector is experiencing one of its strongest growth phases in recent years. Rising domestic travel, increasing corporate activity, expansion of the meetings and events industry, and growing international tourism are driving occupancy rates and room tariffs higher across major cities.

Unlike traditional hotel operators that depend solely on room revenues, integrated hospitality companies with premium assets and mixed-use developments enjoy multiple growth avenues. Chalet Hotels Ltd. stands out in this category, combining marquee hospitality assets with commercial real estate developments in prime urban locations.

But does Chalet Hotels Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | CHALET |

| Industry/Sector | Hospitality |

| CMP | 794.10 |

| Market Cap (₹ Cr.) | 17,390 |

| P/E | 26.99 (Vs Industry P/E of 34.97) |

| 52 W High/Low | 1082.00 / 691.35 |

| EPS (TTM) | 29.45 |

| Dividend Yield | 0.25% |

About Chalet Hotels Ltd.

Chalet Hotels Limited is a leading owner, developer, and asset manager of high-end hotels in India. The company is promoted by the K Raheja Corp Group and owns premium hospitality assets operated under globally recognized brands such as Marriott, Westin, Novotel, and Hyatt.

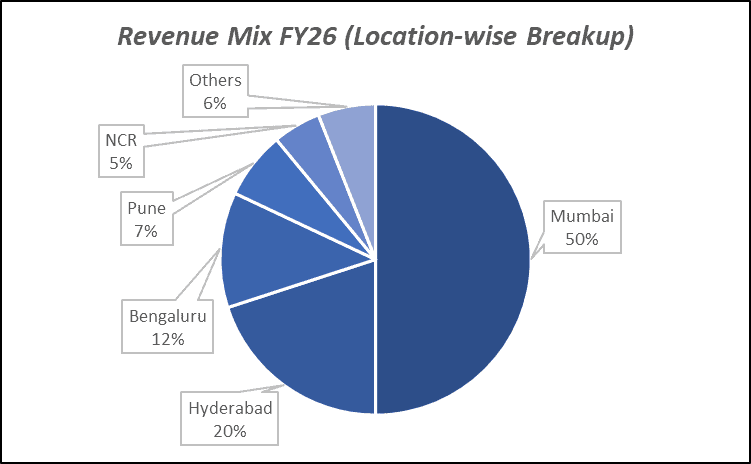

The company has strategically built a portfolio concentrated in key business districts and gateway cities, benefiting from both business and leisure travel demand. Apart from hospitality assets, Chalet has been expanding its presence in commercial and mixed-use developments, creating additional revenue streams.

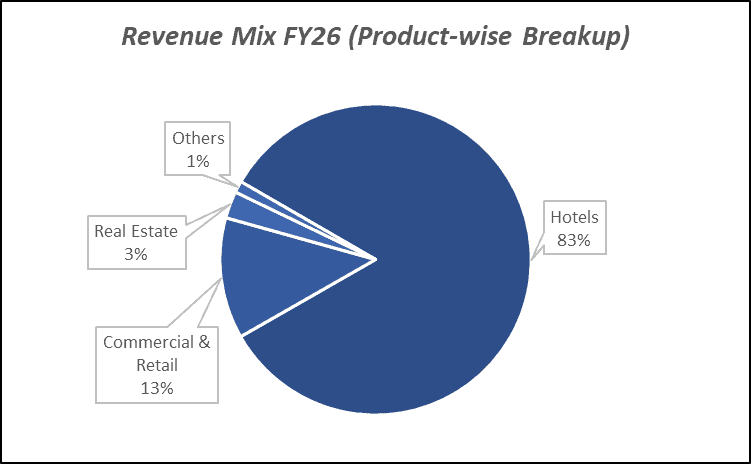

Key business segments

Chalet Hotels Ltd. operates primarily in the following key business segments:

- Hospitality Operations: Luxury and upper-upscale hotels operated under global brands.

- Food & Beverage Services: Restaurants, banquets, events, and catering operations.

- Commercial Real Estate: Office and mixed-use developments adjacent to hotel assets.

- Meetings & Events: Conferences, weddings, corporate events, and banqueting services.

- Asset Development & Management: Development and optimization of hospitality-led real estate assets.

Primary growth factors for Chalet Hotels Ltd.

Chalet Hotels Ltd. key growth drivers:

- Strong Domestic Travel Demand: Rising business and leisure travel supporting occupancy growth.

- Higher Average Room Rates (ARRs): Industry-wide pricing power improving profitability.

- Commercial Real Estate Monetization: Growth from office and mixed-use developments.

- Premium Hospitality Positioning: Exposure to high-end customers and corporate travelers.

- Limited New Supply in Key Markets: Demand outpacing supply supporting sustained pricing strength.

Detailed competition analysis for Chalet Hotels Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Chalet Hotels Ltd. | 2769.75 | 1187.40 | 42.87% | 645.02 | 23.29% | 26.99 |

| ITC Hotels Ltd. | 4139.40 | 1423.78 | 34.40% | 809.39 | 19.55% | 39.15 |

| EIH Ltd. | 2871.86 | 1040.60 | 36.23% | 606.23 | 21.11% | 29.78 |

| Leela Palaces Hotels Ltd. | 1527.29 | 742.85 | 48.64% | 405.72 | 26.56% | 34.38 |

| LemonTree Hotels Ltd. | 1406.61 | 680.03 | 48.35% | 281.01 | 19.98% | 32.10 |

Key insights on Chalet Hotels Ltd.

- Owns premium hospitality assets in strategic urban locations.

- Partnerships with globally recognized hotel brands.

- Beneficiary of India’s hospitality upcycle.

- Diversified revenue streams beyond room rentals.

- Strong exposure to business travel and corporate demand.

- Embedded value from commercial real estate developments.

- Asset ownership model creates long-term value appreciation potential.

Recent financial performance of Chalet Hotels Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 521.97 | 581.68 | 558.22 | -4.03% | 6.94% |

| EBITDA (₹ Cr.) | 241.45 | 265.10 | 265.79 | 0.26% | 10.08% |

| EBITDA Margin (%) | 46.26% | 45.57% | 47.61% | 204 bps | 135 bps |

| PAT (₹ Cr.) | 123.83 | 124.07 | 163.00 | 31.38% | 31.63% |

| PAT Margin (%) | 23.72% | 21.33% | 29.20% | 787 bps | 548 bps |

| Adjusted EPS (₹) | 5.67 | 5.67 | 7.44 | 31.22% | 31.22% |

Chalet Hotels Ltd. financial update (Q4 FY26)

Financial performance

- Revenue surged 61% YoY to ₹2,770 crore in FY26, supported by strong hospitality performance and substantial revenue recognition from the residential segment.

- EBITDA increased 61% YoY to ₹1,187 crore in FY26, reflecting robust operating leverage and resilient demand across key hospitality assets.

- EBITDA margin improved to 42.9% in FY26, demonstrating strong pricing power, disciplined cost management and a favourable business mix.

- Adjusted PAT jumped 354% YoY to ₹646 crore in FY26, driven by higher operating profitability, residential project execution and lower effective financing costs.

- Return ratios strengthened significantly, with ROE at 19.2% and ROCE at 15.6%, highlighting improved profitability and efficient capital utilisation.

Business highlights

- Hospitality revenue grew 14% YoY in FY26, supported by a 5.1% increase in RevPAR and a 13.5% rise in Average Daily Rate (ADR) to ₹13,727.

- Chalet crossed the 5,000-key milestone, with 3,389 operational keys and a development pipeline of 1,655 keys across seven upcoming projects.

- The company expanded its leisure portfolio through the acquisition of Inder Residency Resort & Spa, Udaipur, strengthening its presence in the high-growth luxury leisure segment.

- Chalet announced the development of a 330-key Ritz-Carlton hotel in Hyderabad, reinforcing its premium hospitality strategy and long-term growth visibility.

- The commercial real estate portfolio continued to generate stable cash flows, with monthly rental income reaching approximately ₹28 crore, supported by improving occupancy levels.

Outlook

- Management remains optimistic on the hospitality sector, supported by favourable demand-supply dynamics, rising domestic travel, increasing wedding demand and India’s expanding economic footprint.

- The upcoming Ritz-Carlton Hyderabad, Udaipur resort redevelopment and additional inventory additions are expected to drive long-term revenue and earnings growth.

- Rental income from the commercial real estate portfolio is expected to increase further as occupancy improves across key properties in Bengaluru and Powai.

- Several growth projects, including Cignus II Powai and the Taj Delhi Airport expansion, are progressing as planned and are expected to contribute meaningfully from FY27 onwards.

- Long-term growth remains supported by premiumisation, expanding room inventory, disciplined capital allocation, healthy cash generation and continued investments across hospitality and commercial real estate assets.

Recent Updates on Chalet Hotels Ltd.

- Continued expansion of commercial office developments.

- Focus on enhancing occupancy and revenue per available room (RevPAR).

- Investments in premium guest experiences and asset upgrades.

- Strengthening mixed-use real estate portfolio.

- Growing demand from corporate travel and events segments.

Company valuation insights – Chalet Hotels Ltd.

Chalet Hotels Ltd. is currently trading at an EV/EBITDA of 19x, while the stock has delivered a -13.2% return over the last one year, compared to the NIFTY 50’s -5.1% return during the same period.

The investment case for Chalet Hotels is supported by its premium hospitality portfolio, strong pricing power, and expanding presence across high-growth business and leisure destinations. The company continues to benefit from favourable demand-supply dynamics in the Indian hospitality sector, driven by rising domestic travel, increasing wedding demand, and sustained growth in corporate travel. Chalet has successfully crossed the 5,000-key milestone and is strengthening its long-term growth runway through strategic initiatives such as the acquisition of the Udaipur resort property and the development of the ultra-luxury Ritz-Carlton Hyderabad project. Its commercial real estate portfolio provides stable, high-margin annuity income, while disciplined capital allocation and strong operating cash flows have enabled the company to reduce net debt despite significant expansion investments. With continued premiumisation, growing room inventory, improving rental income, and multiple growth projects nearing completion, Chalet Hotels remains well positioned to deliver sustainable earnings growth and long-term shareholder value.

From a valuation perspective, valuing the company at 21x FY28E EV/EBITDA, we arrive at a 12-month target price of ₹990, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹845, indicating a 6% upside potential, supported by strong ADR growth, improving occupancy trends, ramp-up of newly commissioned assets, increasing commercial rental income, and progress on key expansion projects including Ritz-Carlton Hyderabad and the Udaipur redevelopment.

Major risk factors affecting Chalet Hotels Ltd.

- Economic Slowdown Risk: Weak corporate and leisure travel impacting occupancy.

- Hospitality Cyclicality: Hotel demand linked to economic activity and tourism.

- High Capex Requirements: Continuous investments needed for asset upgrades and expansion.

- Competition: Increasing hotel supply in key markets.

- Interest Rate Risk: Higher financing costs affecting expansion and profitability.

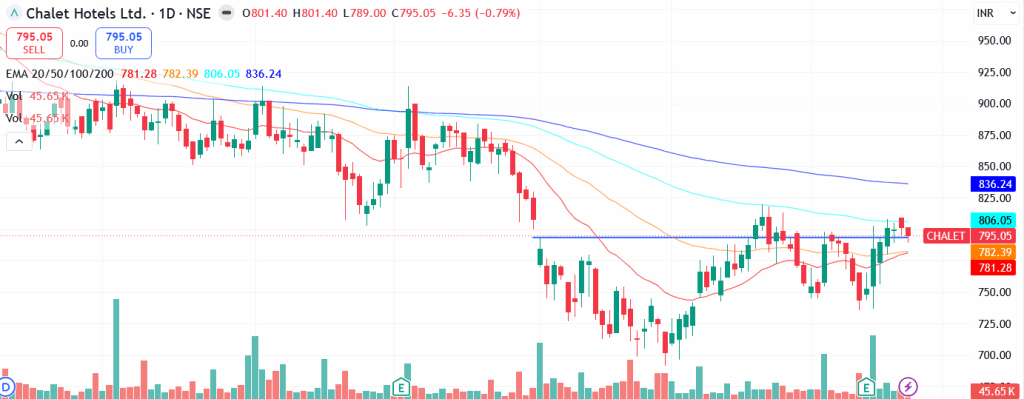

Technical analysis of Chalet Hotels Ltd. share

Chalet Hotels Ltd. is currently hovering around the neckline of a well-formed cup-and-handle pattern, a bullish continuation setup that often precedes a meaningful upward move upon breakout. The stock has recovered steadily from its recent lows and is displaying improving price action, indicating renewed buying interest. It is currently trading above its 20-day and 50-day EMAs, reflecting strengthening short- and medium-term momentum, while remaining below its long-term moving averages. This suggests that although the stock is in the early stages of a recovery, there remains considerable room for upside if the breakout sustains.

Momentum indicators are gradually turning favourable. The MACD at 6.47 remains positive and above its signal line, indicating improving bullish momentum and supporting the possibility of a breakout from the current consolidation zone. The RSI at 55.61 reflects healthy buying interest without entering overbought territory, providing sufficient headroom for further gains. Additionally, the Relative RSI over the 21-day and 55-day periods stands at 0.01 and 0.04 respectively, indicating modest outperformance against the broader benchmark and suggesting improving relative strength within the hospitality sector.

Trend strength remains relatively subdued for now, with the ADX at 13.22 indicating a rangebound market and the absence of a strong directional trend. However, this is typical during the handle formation phase of a cup-and-handle pattern. A decisive breakout above ₹845, which acts as the immediate resistance and neckline level, could significantly improve trend strength, attract fresh momentum buying, and potentially pave the way towards ₹990, in line with our 12-month fundamental target. On the downside, ₹750 remains a key support level, below which the current bullish setup may weaken.

- RSI: 55.61 (Good buying interest)

- ADX: 13.22 (Rangebound, breakout awaited)

- MACD: 6.47 (Positive; above signal line)

- Resistance: ₹845

- Support: ₹750

Chalet Hotels Ltd. stock recommendation

Current Stance: Buy, with a 3-month target price of ₹845 (6% upside) and a 12-month target price of ₹990 (24% upside), based on a valuation of 21x FY28E EV/EBITDA.

Why buy now?

Strong pricing power and premium positioning, reflected in sustained ADR growth despite temporary occupancy-related challenges.

Expanding hospitality portfolio with strategic projects such as Ritz-Carlton Hyderabad and the redevelopment of the Udaipur resort strengthening long-term growth visibility.

Robust demand outlook driven by domestic travel, weddings, corporate travel and favourable industry demand-supply dynamics.

Stable and growing annuity income from the commercial real estate portfolio, providing high-margin and predictable cash flows.

Disciplined capital allocation and strong cash generation supporting expansion while maintaining a healthy balance sheet and reducing net debt.

Portfolio fit

Chalet Hotels offers exposure to India’s premium hospitality sector through a high-quality portfolio of business and leisure hotels complemented by stable commercial real estate assets. Its strong brand partnerships, expanding room inventory, growing annuity income and disciplined execution position the company well to benefit from the long-term growth in travel, tourism and hospitality demand, making it a suitable addition to growth-oriented portfolios.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebChalet Hotels Ltd.: Budget 2026-27 opportunities

- Tourism Infrastructure Development: Increased travel demand supporting hotel occupancy.

- Business District Expansion: Growth in commercial hubs boosting corporate travel.

- Convention & Events Promotion: Higher demand for meetings, conferences, and exhibitions.

- Urban Infrastructure Investments: Improved connectivity supporting hospitality demand.

- Real Estate Development Incentives: Opportunities for mixed-use and commercial projects.

Final thoughts

Chalet Hotels Limited stands at the intersection of two powerful long-term themes — India’s growing travel economy and urban commercial real estate expansion. With a portfolio of premium hospitality assets, strong global brand partnerships, and increasing contribution from commercial developments, the company is well positioned to benefit from rising travel demand and urbanization.

For investors seeking exposure to India’s hospitality sector with the added advantage of real estate value creation, Chalet Hotels offers a compelling blend of premium assets, operating leverage, and long-term growth opportunities.