India’s healthcare sector is witnessing a structural transformation driven by rising health awareness, increasing insurance penetration, growing lifestyle diseases, and improving access to quality medical care. As demand shifts from fragmented healthcare providers to organized hospital chains, scalable healthcare platforms are gaining market share across the country.

Among the emerging leaders in this space is KIMS Ltd., which has built a strong presence across South India through a network of multi-specialty hospitals focused on affordability, clinical excellence, and operational efficiency.

But does Krishna Institute of Medical Sciences Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | KIMS |

| Industry/Sector | Healthcare & Pharma |

| CMP | 758.35 |

| Market Cap (₹ Cr.) | 30,345 |

| P/E | 126.29 (Vs Industry P/E of 60.46) |

| 52 W High/Low | 798.40 / 575.80 |

| EPS (TTM) | 6.05 |

| Dividend Yield | 0.00% |

About Krishna Institute of Medical Sciences Ltd.

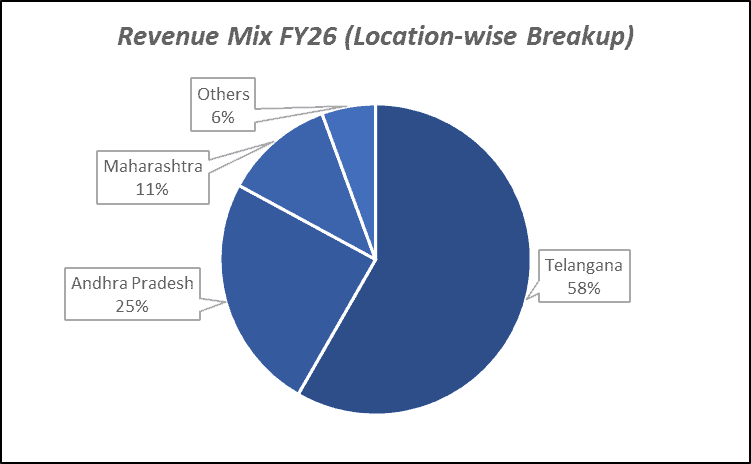

Krishna Institute of Medical Sciences Limited is one of India’s leading healthcare providers, operating a network of multi-specialty hospitals primarily across Telangana, Andhra Pradesh, Maharashtra, Kerala, and other regions.

The company offers tertiary and quaternary healthcare services across specialties including cardiology, oncology, neurosciences, organ transplantation, orthopedics, and critical care. KIMS has developed a reputation for delivering quality healthcare while maintaining cost efficiencies, allowing it to serve a broad patient base.

Its hub-and-spoke model, strong doctor network, and disciplined capital allocation have enabled the company to scale operations while maintaining healthy profitability.

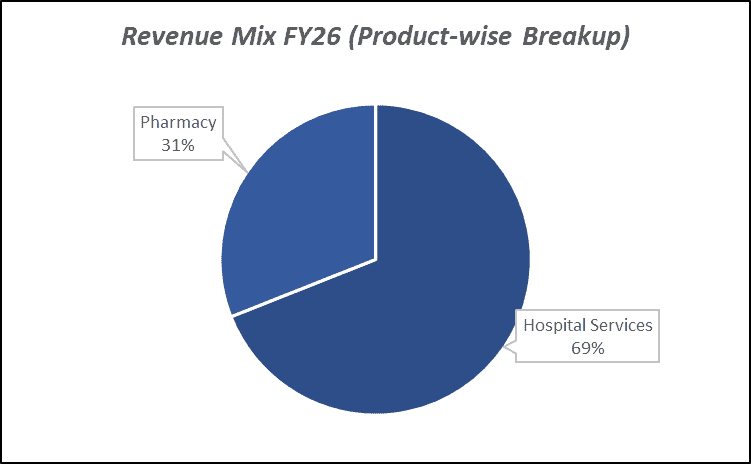

Key business segments

Krishna Institute of Medical Sciences Ltd. operates primarily in the following key business segments:

- Multi-Specialty Hospitals: Tertiary and quaternary healthcare services across specialties.

- Cardiac Sciences: Cardiology and cardiovascular surgery treatments.

- Oncology Services: Cancer diagnosis, treatment, and related healthcare services.

- Transplant & Critical Care: Organ transplantation and intensive care services.

- Diagnostics & Ancillary Services: Laboratory, imaging, pharmacy, and support services.

Primary growth factors for Krishna Institute of Medical Sciences Ltd.

Krishna Institute of Medical Sciences Ltd. key growth drivers:

- Rising Healthcare Demand: Increasing incidence of chronic diseases and higher healthcare awareness.

- Expansion into New Geographies: Capacity additions and acquisitions supporting network growth.

- Higher Occupancy & ARPOB Growth: Improving utilization and revenue per occupied bed.

- Medical Tourism Opportunities: Growing inflow of domestic and international patients.

- Insurance Penetration Growth: Greater affordability supporting higher healthcare spending.

Detailed competition analysis for Krishna Institute of Medical Sciences Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| KIMS Ltd. | 3904.60 | 802.00 | 20.54% | 239.40 | 6.13% | 126.29 |

| Narayana Hrudayalaya Ltd. | 7896.04 | 1616.67 | 20.47% | 816.04 | 10.33% | 48.63 |

| Global Health Ltd. | 4410.27 | 919.10 | 20.84% | 554.07 | 12.56% | 60.09 |

| Dr. Lal Pathlabs Ltd. | 2762.90 | 782.50 | 28.32% | 509.80 | 18.45% | 53.50 |

| Aster DM Healthcare Ltd. | 4643.22 | 901.03 | 19.41% | 464.10 | 10.00% | 91.78 |

Key insights on Krishna Institute of Medical Sciences Ltd.

- One of the leading hospital chains in South India.

- Strong presence in tertiary and quaternary care services.

- Asset-light expansion through acquisitions and brownfield additions.

- Consistently healthy operating margins compared to industry peers.

- Strong doctor retention and clinical excellence driving patient trust.

- Beneficiary of increasing health insurance penetration.

- Significant opportunity to scale beyond core markets.

Recent financial performance of Krishna Institute of Medical Sciences Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 796.90 | 997.70 | 1074.60 | 7.71% | 34.85% |

| EBITDA (₹ Cr.) | 198.00 | 198.90 | 206.50 | 3.82% | 4.29% |

| EBITDA Margin (%) | 24.85% | 19.94% | 19.22% | -72 bps | -563 bps |

| PAT (₹ Cr.) | 106.10 | 51.90 | 30.50 | -41.23% | -71.25% |

| PAT Margin (%) | 13.31% | 5.20% | 2.84% | -236 bps | -1047 bps |

| Adjusted EPS (₹) | 2.55 | 1.33 | 1.06 | -20.30% | -58.43% |

Krishna Institute of Medical Sciences Ltd. financial update (Q4 FY26)

Financial performance

- Revenue grew 29% YoY to ₹3,905 crore in FY26, driven by strong growth across Telangana, Andhra Pradesh, Maharashtra, Kerala and the newly added Bangalore cluster.

- EBITDA increased 2% YoY to ₹802 crore in FY26, despite losses from newly commissioned hospitals, highlighting the resilience of the core business and mature hospital network.

- EBITDA margin moderated to 20.5% in FY26 from 25.8% in FY25, primarily due to start-up losses associated with greenfield expansions in Bangalore, Maharashtra and Kerala.

- Adjusted PAT stood at ₹241 crore in FY26, impacted by higher depreciation and interest costs arising from ongoing capacity expansion and new facility additions.

- Return ratios remained healthy with ROE at 11.5% and ROCE at 10.9%, providing a solid foundation for earnings improvement as new hospitals mature and achieve operational scale.

Business highlights

- KIMS added 1,285 beds during FY26 across Bangalore, Thane, Vizag, Kannur, Kollam and Nashik, significantly expanding its footprint across key healthcare markets.

- Average Revenue Per Occupied Bed (ARPOB) increased 14% YoY to ₹44,644 per day, driven by an improved case mix and higher contribution from complex procedures.

- Mature hospitals continued to deliver strong profitability, generating EBITDA margins of 28–29%, highlighting the strength of KIMS’ operating model and execution capabilities.

- Maharashtra and Kerala clusters showed improving performance, with losses narrowing significantly and several facilities moving closer to EBITDA breakeven.

- The company strengthened its specialty care offerings through new initiatives, including the launch of KIMS Cuddles at Nellore and the inauguration of a dedicated cancer block at Ongole.

Outlook

- Management remains focused on scaling its new clusters across Karnataka, Kerala and Maharashtra, with the objective of achieving EBITDA margins above 25% over the next 3–4 years.

- The new 800-bed Kondapur facility is scheduled to commence operations in FY27, providing a significant growth runway and strengthening KIMS’ leadership position in Telangana.

- Several recently commissioned hospitals are expected to achieve EBITDA breakeven over the next 12–18 months, supporting margin expansion and operating leverage.

- The company continues to evaluate strategic acquisitions alongside greenfield expansions, targeting further capacity additions across South and West India.

- Long-term growth remains supported by increasing healthcare demand, rising occupancy levels, improving ARPOB, strong execution capabilities and a scalable multi-cluster hospital expansion strategy.

Recent Updates on Krishna Institute of Medical Sciences Ltd.

- Continued expansion through acquisitions and capacity additions.

- Focus on strengthening presence in high-growth healthcare markets.

- Investments in advanced medical technologies and specialty services.

- Expansion of oncology, transplant, and critical care capabilities.

- Increased emphasis on operational efficiency and patient experience.

Company valuation insights – Krishna Institute of Medical Sciences Ltd.

Krishna Institute of Medical Sciences (KIMS) Ltd. is currently trading at an EV/EBITDA of 35x, while the stock has delivered a 13% return over the last one year, outperforming the NIFTY 50’s -5.1% return during the same period.

The investment case for KIMS is driven by its successful multi-cluster hospital expansion strategy, strong execution capabilities, and scalable low-cost operating model. The company continues to strengthen its presence beyond its core Telangana and Andhra Pradesh markets through rapid expansion across Karnataka, Maharashtra, and Kerala, where recently commissioned hospitals are demonstrating encouraging ramp-up trends. Mature hospitals continue to deliver industry-leading profitability, supported by healthy occupancy levels, improving case mix, and strong growth in Average Revenue Per Occupied Bed (ARPOB). KIMS has added significant capacity over the last year and is set to further accelerate growth with the commissioning of the new 800-bed Kondapur facility. As newer hospitals move towards breakeven and operating leverage improves, margins are expected to recover steadily. Backed by strong clinical leadership, increasing healthcare demand, strategic expansion opportunities, and a proven ability to scale new facilities efficiently, KIMS remains well positioned to deliver sustainable earnings growth and long-term shareholder value.

From a valuation perspective, valuing the company at 30x FY28E EV/EBITDA, we arrive at a 12-month target price of ₹940, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹805, indicating a 6% upside potential, supported by continued ramp-up of new hospitals, improving profitability across emerging clusters, commissioning of the Kondapur facility, and increasing operating leverage as recently added capacities mature.

Major risk factors affecting Krishna Institute of Medical Sciences Ltd.

- Execution Risk: Timely ramp-up of newly acquired and expanded hospitals.

- Doctor Retention Risk: Dependence on specialist doctors and medical talent.

- Regulatory Risks: Changes in healthcare pricing regulations and compliance requirements.

- Competition: Intensifying competition from national and regional hospital chains.

- High Capex Nature: Continuous investments required for healthcare infrastructure expansion.

Technical analysis of Krishna Institute of Medical Sciences Ltd. share

Krishna Institute of Medical Sciences (KIMS) Ltd. continues to exhibit a strong positive price structure, with the stock trading comfortably above all its key moving averages (20, 50, 100, and 200-day EMAs), reflecting sustained strength across short, medium, and long-term timeframes. The stock has been maintaining a steady uptrend, supported by consistent buying interest and resilient price action, indicating that investors remain constructive on the company’s growth prospects. The overall technical setup remains favourable, with higher highs and higher lows reinforcing the ongoing bullish trend.

Momentum indicators continue to support the positive outlook. The MACD at 24.73 remains firmly in positive territory and above its signal line, indicating sustained bullish momentum and confirming the strength of the prevailing uptrend. The RSI at 61.12 reflects healthy buying interest without entering overbought territory, leaving room for further upside if momentum continues. Additionally, the Relative RSI over the 21-day and 55-day periods stands at 0.15 and 0.11 respectively, highlighting consistent outperformance against the broader benchmark and demonstrating relative strength within the healthcare sector.

Trend strength remains robust, with the ADX at 31.48 indicating a strong and established trend. This suggests that the ongoing up move is supported by meaningful directional strength rather than short-term fluctuations. A sustained move above ₹805, which acts as the immediate resistance level, could attract fresh buying interest and potentially pave the way towards ₹940, in line with our 12-month fundamental target. On the downside, ₹710 remains a crucial support level, below which the current bullish structure may weaken.

- RSI: 61.12 (Strong buying interest)

- ADX: 31.48 (Strong trend)

- MACD: 24.73 (Positive; above signal line)

- Resistance: ₹805

- Support: ₹710

Krishna Institute of Medical Sciences Ltd. stock recommendation

Current Stance: Buy, with a 3-month target price of ₹805 (6% upside) and a 12-month target price of ₹940 (24% upside), based on a valuation of 30x FY28E EV/EBITDA.

Why buy now?

Strong hospital expansion pipeline across Karnataka, Maharashtra and Kerala, supported by rapid ramp-up of newly commissioned facilities.

Industry-leading profitability in mature hospitals, driven by a lean operating model, healthy occupancy levels and strong ARPOB growth.

Upcoming commissioning of the 800-bed Kondapur facility, providing a significant growth runway in its core Telangana market.

Improving profitability across new clusters, with several hospitals expected to achieve EBITDA breakeven over the next 12–18 months.

Rising healthcare demand, expanding specialty care offerings and strong execution capabilities supporting long-term earnings growth.

Portfolio fit

KIMS provides exposure to India’s growing healthcare and hospital sector through a scalable multi-cluster expansion strategy and a proven track record of operational execution. Its combination of strong mature-hospital profitability, improving returns from new facilities, expanding bed capacity and increasing revenue intensity positions it well for sustained growth, making it a suitable addition to long-term healthcare-focused portfolios.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebKrishna Institute of Medical Sciences Ltd.: Budget 2026-27 opportunities

- Healthcare Infrastructure Spending: Increased investments supporting hospital sector growth.

- Expansion of Health Insurance Coverage: Greater affordability driving patient volumes.

- Medical Tourism Promotion: Higher inflow of international patients.

- Digital Healthcare Initiatives: Improved healthcare accessibility and patient engagement.

- Tier-II & Tier-III Healthcare Development: Growing demand for quality healthcare services beyond metros.

Final thoughts

Krishna Institute of Medical Sciences Limited stands at an attractive point in India’s healthcare growth journey. With strong clinical capabilities, expanding hospital infrastructure, healthy profitability, and increasing demand for quality healthcare services, the company is well positioned to benefit from long-term structural healthcare trends.

For investors seeking exposure to India’s healthcare sector with a blend of defensive earnings, scalable growth, and operational excellence, KIMS offers a compelling combination of strong execution, expansion opportunities, and sustainable long-term demand drivers.