India’s pharmaceutical sector has evolved from being the “pharmacy of the world” to becoming a hub for complex generics, specialty medicines, biologics, and innovation-led healthcare solutions. As healthcare access expands globally and demand for affordable medicines continues to rise, companies with strong R&D capabilities and diversified product portfolios stand to benefit significantly.

Among India’s leading pharmaceutical players, Zydus Lifesciences Ltd. has built a strong presence across domestic formulations, global generics, APIs, vaccines, and specialty products. The company is increasingly positioning itself as a diversified healthcare platform with both scale and innovation capabilities.

But does Zydus Lifesciences Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | ZYDUSLIFE |

| Industry/Sector | Healthcare & Pharma |

| CMP | 1038.60 |

| Market Cap (₹ Cr.) | 1,04,507 |

| P/E | 20.40 (Vs Industry P/E of 34.13) |

| 52 W High/Low | 1093.65 / 835.50 |

| EPS (TTM) | 50.92 |

| Dividend Yield | 0.10% |

About Zydus Lifesciences Ltd.

Zydus Lifesciences Limited is one of India’s leading pharmaceutical companies engaged in the research, development, manufacturing, and marketing of pharmaceutical formulations, active pharmaceutical ingredients (APIs), biologics, vaccines, and specialty products.

Headquartered in Ahmedabad, the company has a significant presence across India, the United States, Europe, Latin America, and emerging markets. Over the years, Zydus has developed strong capabilities in complex generics, specialty therapies, and differentiated pharmaceutical products.

Key business segments

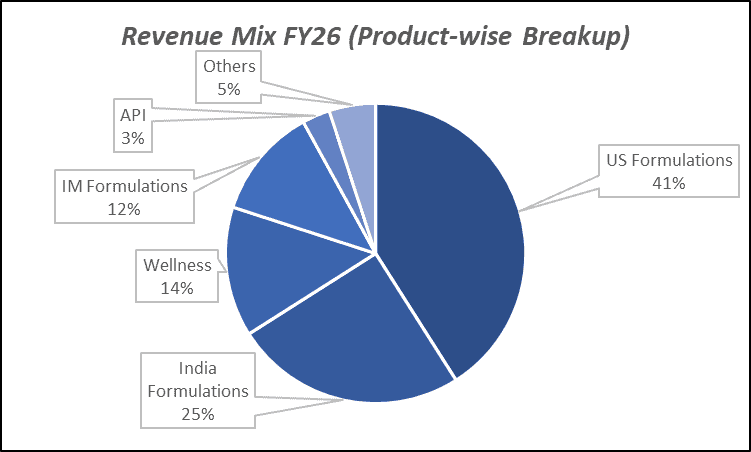

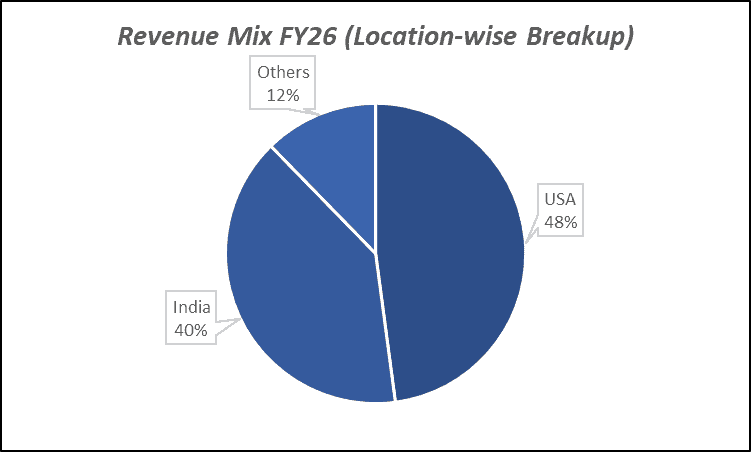

Zydus Lifesciences Ltd. operates primarily in the following key business segments:

- Domestic Formulations: Branded prescription medicines across multiple therapeutic categories.

- US Generics Business: Generic pharmaceuticals for the United States market.

- International Formulations: Medicines supplied to Europe, Latin America, and emerging markets.

- Active Pharmaceutical Ingredients (APIs): Manufacturing of pharmaceutical raw materials.

- Biologics & Vaccines: Innovative biologics, vaccines, and specialty healthcare products.

Primary growth factors for Zydus Lifesciences Ltd.

Zydus Lifesciences Ltd. key growth drivers:

- Strong US Generics Pipeline: New product launches supporting export growth and market share gains.

- Domestic Formulation Expansion: Rising healthcare penetration driving prescription growth.

- Specialty & Complex Generics Portfolio: Higher-margin products improving profitability.

- Biologics and Innovation Pipeline: Long-term opportunities from differentiated therapies.

- Global Market Diversification: Reduced dependence on any single geography or product category.

Detailed competition analysis for Zydus Lifesciences Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Zydus Lifesciences Ltd. | 27148.40 | 7194.60 | 26.50% | 5026.40 | 18.51% | 20.40 |

| Gland Pharma Ltd. | 6430.65 | 1629.54 | 25.34% | 1027.32 | 15.98% | 35.62 |

| JB Chemicals Ltd. | 4147.79 | 1107.43 | 26.70% | 709.47 | 17.10% | 48.89 |

| Sai Life Sciences Ltd. | 2192.49 | 631.16 | 28.79% | 348.91 | 15.91% | 69.37 |

| Piramal Pharma Ltd. | 8869.08 | 921.62 | 10.39% | -383.14 | -4.32% | NA |

Key insights on Zydus Lifesciences Ltd.

- One of India’s most diversified pharmaceutical companies.

- Strong balance between domestic and international businesses.

- Growing focus on specialty products and complex generics.

- Significant manufacturing and R&D infrastructure.

- Strong track record of regulatory compliance and product development.

- Exposure to multiple therapeutic segments reduces concentration risk.

- Increasing contribution from differentiated and value-added products.

Recent financial performance of Zydus Lifesciences Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 6527.90 | 6864.50 | 7587.00 | 10.53% | 16.22% |

| EBITDA (₹ Cr.) | 2125.50 | 1816.40 | 1909.50 | 5.13% | -10.16% |

| EBITDA Margin (%) | 32.56% | 26.46% | 25.17% | -129 bps | -739 bps |

| PAT (₹ Cr.) | 1248.80 | 965.10 | 1341.30 | 38.98% | 7.41% |

| PAT Margin (%) | 19.13% | 14.06% | 17.68% | 362 bps | -145 bps |

| Adjusted EPS (₹) | 11.64 | 10.36 | 12.65 | 22.10% | 8.68% |

Zydus Lifesciences Ltd. financial update (Q4 FY26)

Financial performance

- Revenue grew 17% YoY to ₹27,148 crore in FY26, driven by strong performance in Domestic Formulations, Consumer Wellness and Emerging Markets, offsetting softness in the US generics business.

- EBITDA increased 3% YoY to ₹7,195 crore in FY26, supported by healthy revenue growth, although profitability was impacted by higher R&D investments and increased operating expenses.

- EBITDA margin moderated to 26.5% in FY26 from 30.1% in FY25 due to elevated employee costs, R&D expenditure and marketing investments aimed at strengthening future growth drivers.

- Adjusted PAT stood at ₹4,496 crore in FY26, reflecting a marginal decline of 3% YoY despite strong operational growth, owing to higher depreciation, finance costs and investments in specialty initiatives.

- Return ratios remained healthy with ROE at 17.6% and ROCE at 13.9%, underlining the company’s strong earnings profile and capital allocation discipline.

Business highlights

- Domestic Formulations business grew 12% YoY in FY26, outperforming the Indian Pharmaceutical Market, supported by strong traction in chronic therapies and multiple specialty product launches.

- The company strengthened its biologics and specialty portfolio through launches such as Tishtha (Nivolumab biosimilar), Anyra (Aflibercept biosimilar) and Semaglutide across diabetes and obesity segments.

- Emerging Markets delivered robust 46% YoY growth in FY26, benefiting from a therapy-focused strategy and increasing market penetration across key geographies.

- The US business maintained a stable base despite generic pricing pressures, while the specialty franchise continued to expand through Sentynl, 505(b)(2) products and rare disease therapies.

- Zydus advanced its innovation pipeline with regulatory approval for Desidustat in China, initiation of Phase III trials for a biosimilar ADC and continued progress in novel biologics and specialty therapies.

Outlook

- Management has guided for high-teen revenue growth in FY27, supported by continued momentum in India, Emerging Markets, specialty products and new launches.

- Consolidated EBITDA margin is expected to remain above 24% in FY27, aided by improving product mix and operating leverage despite elevated R&D spending.

- The US specialty business, including rare disease products and the 505(b)(2) portfolio, is expected to scale meaningfully over the next 3–4 years, becoming an important growth engine.

- Domestic Formulations is expected to continue outperforming the industry by 200–400 bps, supported by a richer chronic portfolio and specialty launches.

- Long-term growth remains underpinned by sustained investments in innovation, biologics, specialty products and manufacturing capabilities, with FY27 capex guidance of approximately ₹1,500 crore.

Recent Updates on Zydus Lifesciences Ltd.

- Continued expansion of specialty and differentiated product portfolio.

- Increased focus on biologics and novel healthcare solutions.

- Capacity expansion and manufacturing modernization initiatives.

- Strengthening presence in regulated international markets.

- Ongoing investments in research and product development pipeline.

Company valuation insights – Zydus Lifesciences Ltd.

Zydus LifeSciences Ltd. is currently trading at a TTM P/E of 20.40x, significantly below the industry average of 34.13x, while the stock has delivered a 13.8% return over the last one year, outperforming the NIFTY 50’s -5.1% return during the same period.

The investment case for Zydus LifeSciences is supported by its diversified growth drivers across domestic formulations, specialty pharmaceuticals, biologics, consumer wellness, and emerging markets. The company continues to outperform the Indian pharmaceutical market through a growing chronic therapy portfolio, strong brand franchise, and a steady stream of specialty product launches, including biosimilars and GLP-1 therapies. In the US market, Zydus is expanding its differentiated specialty and rare disease portfolio through Sentynl and its 505(b)(2) pipeline, while maintaining a stable base generics business. The company is also strengthening its innovation-led growth platform with advancing biologics, novel drug candidates, and a robust R&D pipeline spanning oncology, immunology, nephrology, and rare diseases. Strong traction in emerging markets, increasing contribution from higher-margin specialty products, strategic acquisitions such as Amplitude Surgical, and continued investments in manufacturing and research capabilities position Zydus well to deliver sustainable earnings growth and create long-term shareholder value.

From a valuation perspective, valuing the company at 21x FY28E EPS of ₹62, we arrive at a 12-month target price of ₹1,300, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹1,100, indicating a 6% upside potential, supported by continued growth in domestic formulations, improving traction in specialty products and biosimilars, expansion of the US specialty portfolio, and sustained momentum across emerging markets.

Major risk factors affecting Zydus Lifesciences Ltd.

- US Pricing Pressure: Competitive generic markets can impact profitability.

- Regulatory Risk: Observations from global regulatory authorities affecting operations.

- Currency Risk: Exchange rate fluctuations impacting export revenues.

- R&D Execution Risk: Delays or failures in product development programs.

- Competitive Intensity: Increasing competition across key therapeutic segments.

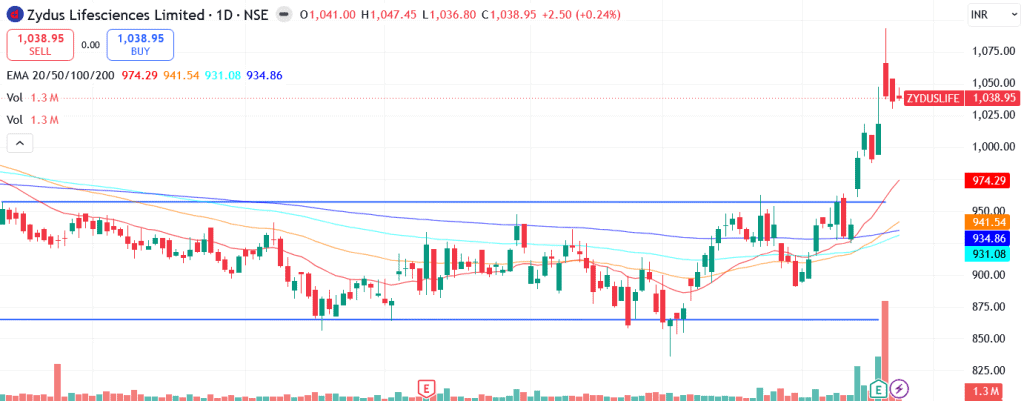

Technical analysis of Zydus Lifesciences Ltd. share

Zydus LifeSciences Ltd. has recently broken out of a prolonged sideways consolidation channel, signalling a resumption of the broader uptrend and indicating strengthening bullish momentum. The stock is currently trading above all its key moving averages (20, 50, 100, and 200-day EMAs), reflecting strong price structure and sustained strength across short, medium, and long-term timeframes. The breakout is accompanied by improving volumes and positive price action, suggesting renewed investor interest and the potential for further upside.

Momentum indicators remain firmly supportive. The MACD at 31.48 is positive and trading above its signal line, indicating strengthening bullish momentum and confirming the recent breakout. The RSI at 69.40 reflects strong buying interest and robust momentum, while still remaining below extreme overbought levels. Additionally, the Relative RSI over the 21-day and 55-day periods stands at 0.15 and 0.19 respectively, highlighting consistent outperformance against the broader benchmark and underscoring the stock’s relative strength within the pharmaceutical sector.

Trend strength has improved significantly, with the ADX at 36.86 indicating a strong and established uptrend. This suggests that the recent breakout is supported by meaningful directional strength rather than short-term price volatility. A sustained move above ₹1,100, which acts as the immediate resistance level, could trigger fresh momentum buying and pave the way towards ₹1,300, in line with our 12-month fundamental target. On the downside, ₹960 remains a key support level, below which the current bullish setup may weaken.

- RSI: 69.40 (Strong buying interest)

- ADX: 36.86 (Strong trend)

- MACD: 31.48 (Positive; above signal line)

- Resistance: ₹1,100

- Support: ₹960

Zydus Lifesciences Ltd. stock recommendation

Current Stance: Buy, with a 3-month target price of ₹1,100 (6% upside) and a 12-month target price of ₹1,300 (24% upside), based on a valuation of 21x FY28E EPS of ₹62.

Why buy now?

Strong growth in domestic formulations, supported by a rising chronic therapy mix, market share gains, and specialty product launches.

Expanding specialty and biologics portfolio, including biosimilars and GLP-1 therapies, providing access to high-growth therapeutic segments.

Growing US specialty and rare disease business, backed by differentiated products and a robust innovation pipeline.

Sustained investments in R&D, biologics, and novel therapies creating multiple long-term growth opportunities.

Strong momentum in emerging markets and improving product mix supporting sustainable earnings growth and profitability.

Portfolio fit

Zydus LifeSciences provides exposure to a diversified pharmaceutical business with strong positions across domestic formulations, specialty products, biologics, and global markets. Its expanding innovation pipeline, improving product mix, and multiple growth drivers across India, the US, and emerging markets support long-term earnings growth and make it a suitable addition to growth-oriented healthcare portfolios.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebZydus Lifesciences Ltd.: Budget 2026-27 opportunities

- PLI Scheme for Pharmaceuticals: Incentives supporting domestic manufacturing and exports.

- Healthcare Infrastructure Expansion: Increased medicine demand through improved healthcare access.

- API Self-Reliance Initiatives: Government focus on reducing import dependence.

- Biotechnology & Innovation Support: Incentives for research-led pharmaceutical development.

- Export Promotion Policies: Strengthening India’s position as a global pharmaceutical hub.

Final thoughts

Zydus Lifesciences Limited stands at an important phase of evolution, transitioning from a traditional generics-led business toward a more diversified healthcare platform encompassing specialty products, biologics, and innovation-led therapies. With a strong domestic franchise, expanding international presence, and growing focus on differentiated products, the company is well positioned to benefit from long-term healthcare demand.

For investors seeking exposure to India’s pharmaceutical sector with a blend of defensive earnings, global growth opportunities, and innovation optionality, Zydus Lifesciences offers a compelling combination of scale, diversification, and future growth potential.