The specialty chemicals industry has become one of the most exciting segments within India’s manufacturing ecosystem. Global supply chain diversification, increasing demand for high-performance chemicals, and the rising importance of domestic manufacturing are creating long-term opportunities for specialized chemical producers.

Unlike commodity chemical companies that largely compete on pricing, specialty chemical manufacturers benefit from technological expertise, customer relationships, product customization, and higher entry barriers. Companies capable of delivering consistent quality and innovation can create long-lasting competitive advantages.

Acutaas Chemicals Ltd. is positioning itself within this evolving landscape, focusing on value-added chemical solutions and expanding opportunities across domestic and international markets.

But does Acutaas Chemicals Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | ACUTAAS |

| Industry/Sector | Healthcare & Pharma |

| CMP | 2953.20 |

| Market Cap (₹ Cr.) | 24,449 |

| P/E | 66.29 (Vs Industry P/E of 34.63) |

| 52 W High/Low | 3015.00 / 1059.00 |

| EPS (TTM) | 43.53 |

| Dividend Yield | 0.09% |

About Acutaas Chemicals Ltd.

Acutaas Chemicals Limited is engaged in the manufacturing and supply of specialty chemical products catering to diverse industrial applications. The company focuses on delivering customized chemical solutions and serving customers across multiple end-use industries.

With increasing emphasis on product innovation, operational efficiency, and customer-centric manufacturing, Acutaas aims to strengthen its presence within India’s growing specialty chemicals ecosystem while expanding opportunities in export markets.

Key business segments

Acutaas Chemicals Ltd. operates primarily in the following key business segments:

- Specialty Chemicals: High-value chemical products for industrial applications.

- Custom Manufacturing: Tailor-made chemical solutions for specific customer requirements.

- Industrial Chemicals: Products catering to manufacturing and process industries.

- Export Business: Supply of chemical products to international customers.

- Value-Added Chemical Solutions: Specialized formulations and advanced chemical products.

Primary growth factors for Acutaas Chemicals Ltd.

Acutaas Chemicals Ltd. key growth drivers:

- China+1 Supply Chain Opportunity: Global customers increasingly diversifying sourcing toward Indian manufacturers.

- Expansion of Specialty Chemical Portfolio: Higher-value products supporting margin improvement.

- Export Market Growth: Increasing opportunities across regulated and emerging markets.

- Capacity Expansion Initiatives: Enhanced manufacturing capabilities supporting future growth.

- Rising Industrial Demand: Strong demand from pharmaceuticals, agrochemicals, and industrial sectors.

Detailed competition analysis for Acutaas Chemicals Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Acutaas Chemicals Ltd. | 1339.37 | 480.40 | 35.87% | 356.37 | 26.61% | 66.29 |

| Gland Pharma Ltd. | 6430.65 | 1629.54 | 25.34% | 1027.32 | 15.98% | 35.62 |

| JB Chemicals Ltd. | 4147.79 | 1107.43 | 26.70% | 709.47 | 17.10% | 48.89 |

| Sai Life Sciences Ltd. | 2192.49 | 631.16 | 28.79% | 348.91 | 15.91% | 69.37 |

| Piramal Pharma Ltd. | 8869.08 | 921.62 | 10.39% | -383.14 | -4.32% | NA |

Key insights on Acutaas Chemicals Ltd.

- Operates within the high-growth specialty chemicals segment.

- Beneficiary of India’s growing role in global chemical manufacturing.

- Focus on value-added products rather than pure commodity chemicals.

- Potential operating leverage from higher capacity utilization.

- Diversified industrial applications reduce dependence on a single sector.

- Increasing opportunities from export diversification.

- Specialty chemistry expertise can support long-term margin sustainability.

Recent financial performance of Acutaas Chemicals Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 308.48 | 393.18 | 432.75 | 10.06% | 40.28% |

| EBITDA (₹ Cr.) | 84.96 | 150.66 | 183.51 | 21.80% | 116.00% |

| EBITDA Margin (%) | 27.54% | 38.32% | 42.41% | 409 bps | 1487 bps |

| PAT (₹ Cr.) | 62.72 | 106.22 | 134.28 | 26.42% | 114.09% |

| PAT Margin (%) | 20.33% | 27.02% | 31.03% | 401 bps | 1070 bps |

| Adjusted EPS (₹) | 3.82 | 13.19 | 16.09 | 21.99% | 321.20% |

Acutaas Chemicals Ltd. financial update (Q4 FY26)

Financial performance

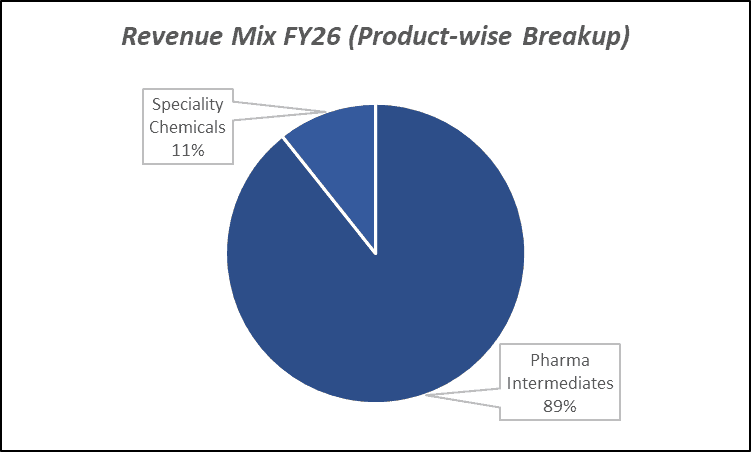

- Revenue grew 33% YoY to ₹1,339 crore in FY26, driven by strong growth in the API business and increasing CDMO contribution.

- EBITDA surged 107% YoY to ₹480 crore in FY26, supported by a favourable product mix, cost optimisation and operating leverage.

- EBITDA margin expanded sharply to 35.9% in FY26, reflecting higher share of value-added products and improved efficiencies.

- PAT more than doubled, rising 124% YoY to ₹356 crore in FY26, marking the company’s highest-ever annual profit.

- Return ratios strengthened significantly, with ROCE at 29% and ROE at 24%, highlighting improved profitability and capital efficiency.

Business highlights

- The API segment delivered strong growth, led by robust traction in the Fermion contract and expanding CDMO operations.

- Specialty Chemicals witnessed healthy recovery, aided by improved demand for semiconductor chemicals and higher-margin products.

- The company invested ₹195 crore in FY26 capex, focusing on battery chemicals, pilot facilities and growth projects.

- Phase-1 of the electrolyte additive project was completed, with Phase-2 expected to be commissioned in FY27.

- Acutaas announced a 10x expansion of its R&D centre to support innovation across pharma, battery, semiconductor and cosmetic chemicals.

Outlook

- Management has guided for 25% revenue growth and 35% EBITDA margins in FY27, supported by a strong business pipeline.

- The company remains on track to achieve its ₹1,000 crore CDMO revenue target by FY28 through scale-up and new customer additions.

- Battery chemicals, semiconductor chemicals and the Indichem JV are expected to become meaningful growth contributors over the next two years.

- Margin sustainability is expected through a richer product mix, cost optimisation and a shift towards differentiated products.

- Long-term growth remains supported by expanding CDMO capabilities, strong R&D investments and increasing presence in high-growth specialty chemical segments.

Recent Updates on Acutaas Chemicals Ltd.

- Continued focus on expanding specialty chemical product offerings.

- Strengthening customer relationships across industrial segments.

- Operational initiatives aimed at improving manufacturing efficiencies.

- Increasing emphasis on export opportunities and international markets.

- Investments in product development and process optimization.

Company valuation insights – Acutaas Chemicals Ltd.

Acutaas Chemicals Ltd. is currently trading at a TTM P/E of 66.29x, significantly higher than the industry average of 34.63x, with the stock delivering an exceptional 166.1% return over the last one year, substantially outperforming the NIFTY 50’s -4.8% return during the same period.

The investment case for Acutaas Chemicals is driven by its rapidly expanding CDMO business, which continues to witness strong traction from existing contracts such as Fermion and a growing pipeline of high-value opportunities. The company is benefiting from robust growth in its Advanced Pharmaceutical Intermediates segment, improving profitability through favorable product mix, cost optimization initiatives, and a strategic shift away from commodity chemicals toward differentiated specialty products. Acutaas is also building multiple long-term growth engines through investments in battery chemicals, semiconductor chemicals, and the Indichem South Korea joint venture, while significantly expanding its R&D capabilities to support innovation across pharmaceuticals, electronics, energy storage, and cosmetics. With management targeting ₹1,000 crore CDMO revenue by FY28, strong demand visibility across key molecules, scalable manufacturing infrastructure, and industry-leading margins, Acutaas remains well positioned to deliver sustained earnings growth and long-term value creation.

From a valuation perspective, valuing the company at 55x FY28E EPS of ₹68, we arrive at a 12-month target price of ₹3,740, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹3,170, indicating a 6% upside, supported by continued CDMO ramp-up, strong margin profile, improving product mix, and increasing contributions from emerging growth verticals such as battery and semiconductor chemicals.

Major risk factors affecting Acutaas Chemicals Ltd.

- Raw Material Volatility: Fluctuations in feedstock prices can affect margins.

- Execution Risk: Delays in capacity expansion or commercialization of new products.

- Global Demand Risk: Slowdown in industrial demand impacting export growth.

- Environmental & Regulatory Risk: Compliance requirements in chemical manufacturing.

- Competition: Presence of established domestic and global specialty chemical players.

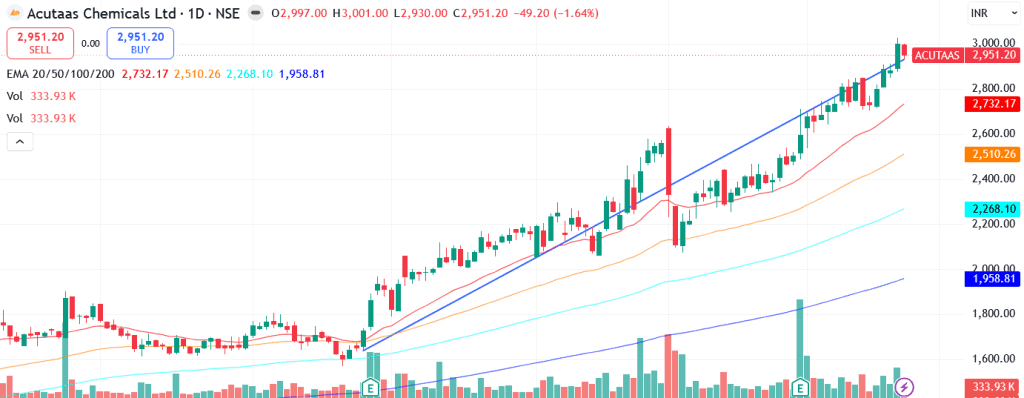

Technical analysis of Acutaas Chemicals Ltd. share

Acutaas Chemicals Ltd remains in a well-established long-term uptrend, supported by a strong price structure and sustained buying interest. The stock is currently trading above all its key moving averages (20, 50, 100, and 200-day EMAs), reflecting strength across short, medium, and long-term timeframes and indicating that the broader bullish trend remains firmly intact.

Momentum indicators continue to support the positive outlook. The MACD at 138.89 remains comfortably in positive territory and above its signal line, highlighting strong bullish momentum and confirming the continuation of the prevailing uptrend. The RSI at 68.25 indicates healthy buying interest and strong price strength, while still remaining below extreme overbought levels, suggesting that the rally could have further room to extend.

The stock is also demonstrating significant relative strength against the broader market. The Relative RSI over the 21-day and 55-day periods stands at 0.25 and 0.45 respectively, indicating consistent outperformance versus the benchmark and reflecting strong investor preference for the stock. Furthermore, the ADX at 39.45 signals a strong and established trend, reinforcing the strength of the ongoing upward move and suggesting that bullish momentum remains firmly in place.

A decisive move above ₹3,170, which acts as a key resistance level, could trigger the next leg of the uptrend and potentially pave the way towards ₹3,740, in line with our 12-month fundamental target. On the downside, ₹2,640 remains a crucial support level, below which the current bullish setup could weaken.

- RSI: 68.25 (Good buying interest)

- ADX: 39.45 (Strong Trend)

- MACD: 138.89 (Positive; above signal line)

- Resistance: ₹3,170

- Support: ₹2,640

Acutaas Chemicals Ltd. stock recommendation

Current Stance: Buy, with a 3-month target price of ₹3,170 (6% upside) and a 12-month target price of ₹3,740 (24% upside), based on a valuation of 55x FY28E EPS of ₹68.

Why buy now?

Rapidly scaling CDMO business, supported by strong traction in the Fermion contract, a growing customer pipeline, and management’s target of achieving ₹1,000 crore CDMO revenue by FY28.

Strong margin profile and earnings growth, driven by favourable product mix, cost optimisation initiatives, and a strategic shift towards differentiated high-value specialty products.

Multiple emerging growth drivers through battery chemicals, semiconductor chemicals, electrolyte additives, and the Indichem South Korea JV, creating diversified long-term revenue streams.

Significant investments in manufacturing and R&D capabilities, including expansion of the Ankleshwar facility and a 10x increase in R&D capacity to support innovation-led growth.

Robust demand environment and strong execution, with management guiding for 25% revenue growth while maintaining industry-leading EBITDA margins of around 35%.

Portfolio fit

Acutaas Chemicals offers a compelling opportunity to participate in the fast-growing specialty chemicals and pharmaceutical outsourcing ecosystem. The company is transforming from a traditional chemical manufacturer into a high-margin, innovation-driven platform with increasing exposure to CDMO, semiconductor, and battery chemical opportunities. Its strong earnings visibility, expanding product portfolio, improving margin profile, and sustained investments in R&D and capacity expansion provide a solid foundation for long-term growth. With scalable manufacturing capabilities, healthy return ratios, and multiple structural growth drivers, Acutaas Chemicals fits well in portfolios seeking exposure to high-growth specialty chemical businesses with strong profitability and long-term value creation potential.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebAcutaas Chemicals Ltd.: Budget 2026-27 opportunities

- Manufacturing-Led Growth Initiatives: Government support for domestic industrial production.

- Export Promotion Policies: Increased competitiveness in international markets.

- Chemical Sector Incentives: Support for specialty and advanced chemical manufacturing.

- Infrastructure & Industrial Expansion: Rising demand for industrial chemical products.

- Research & Innovation Support: Encouragement for technology-driven chemical production.

Final thoughts

Acutaas Chemicals Limited operates within one of India’s most promising manufacturing sectors. Supported by structural tailwinds such as China+1 sourcing, export diversification, and rising specialty chemical demand, the company has opportunities to strengthen its position over the coming years.

For investors seeking exposure to India’s specialty chemicals growth story, Acutaas Chemicals offers a combination of manufacturing expansion, value-added product opportunities, and long-term participation in global supply chain realignment.