In an FMCG landscape dominated by aggressive brand spends and fast-changing consumer preferences, consistency and cash discipline often go unnoticed. Bajaj Consumer Care Ltd (BCCL) represents a quieter FMCG story, built around strong legacy brands, deep rural reach, and a focus on capital efficiency rather than hyper-growth. As consumption gradually broadens beyond metros, such staples-led FMCG players remain relevant long-term compounders.

But does Bajaj Consumer Care Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | BAJAJCON |

| Industry/Sector | FMCG/CD/Services |

| CMP | 298 |

| Market Cap (₹ Cr.) | 3,892 |

| P/E | 25.41 (Vs Industry P/E of 51.97) |

| 52 W High/Low | 319.40 / 151.00 |

| EPS (TTM) | 12.06 |

| Dividend Yield | 0.00% |

About Bajaj Consumer Care Ltd.

Bajaj Consumer Care Ltd is a part of the Bajaj Group and primarily operates in the hair care segment, with a strong presence in light hair oils. The company’s flagship brand, Bajaj Almond Drops, enjoys high recall across urban and rural India. Over time, BCCL has also expanded into ayurvedic and natural hair care, leveraging distribution strength and a conservative balance sheet approach.

Key business segments

Bajaj Consumer Care Ltd. operates primarily in the following key business segments:

- Hair Oils: Light hair oils and almond-based oils under the Bajaj Almond Drops franchise.

- Ayurvedic & Natural Products: Amla, Brahmi, and herbal hair oils targeting wellness-focused consumers.

- International Markets: Presence in select overseas markets, mainly in the Middle East and Africa.

Primary growth factors for Bajaj Consumer Care Ltd.

Bajaj Consumer Care Ltd. key growth drivers:

- Urban & Rural Consumption: Recovery in discretionary FMCG demand supports volume growth.

- Premiumisation: Shift toward light hair oils and value-added formulations improves realizations.

- Brand Strength: Strong legacy brand recall aids repeat consumption and pricing power.

- Distribution Leverage: Deep rural penetration supports incremental volume expansion.

- Cost Discipline: Focus on margins and cash flows over aggressive expansion.

Detailed competition analysis for Bajaj Consumer Care Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Bajaj Consumer Care Ltd. | 1088.55 | 176.35 | 16.20% | 156.81 | 14.41% | 25.41 |

| Safari Industries Ltd. | 1925.15 | 264.56 | 13.74% | 166.16 | 8.63% | 58.38 |

| Emami Ltd. | 3715.13 | 950.88 | 25.59% | 762.78 | 20.53% | 29.23 |

| Gillette India Ltd. | 2970.55 | 826.48 | 27.82% | 573.99 | 19.32% | 45.23 |

| Cupid Ltd. | 252.03 | 74.57 | 29.59% | 61.69 | 24.48% | 172.85 |

Key insights on Bajaj Consumer Care Ltd.

- Category Concentration: Hair oils dominate revenues, limiting diversification.

- Cash-Rich Balance Sheet: Strong cash generation with minimal leverage.

- Moderate Growth Profile: Growth lags larger FMCG peers but remains stable.

- Margin Sensitivity: Input costs (almond oil, packaging) influence near-term margins.

- Defensive Nature: Staples-led portfolio offers resilience during demand slowdowns.

Recent financial performance of Bajaj Consumer Care Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 234.42 | 265.27 | 306.09 | 15.39% | 30.57% |

| EBITDA (₹ Cr.) | 26.22 | 47.83 | 56.08 | 17.25% | 113.88% |

| EBITDA Margin (%) | 11.19% | 18.03% | 18.32% | 29 bps | 713 bps |

| PAT (₹ Cr.) | 25.31 | 42.29 | 46.37 | 9.65% | 83.21% |

| PAT Margin (%) | 10.80% | 15.94% | 15.15% | -79 bps | 435 bps |

| Adjusted EPS(₹) | 1.85 | 3.24 | 3.55 | 9.57% | 91.89% |

Bajaj Consumer Care Ltd. financial update (Q3 FY26)

Financial performance

- Revenue rose 31% YoY to ₹306 crore (consolidated), driven by strong volume-led growth in Almond Drops Hair Oil (ADHO), recovery in general trade, and improved rural traction.

- Gross margin expanded sharply by ~800 bps YoY to 60.0%, supported by strategic pricing actions, improved mix, and easing input cost pressures.

- EBITDA surged 114% YoY to ₹56 crore, with EBITDA margin improving to 18.3%, reflecting operating leverage and disciplined cost control.

- PAT increased 83% YoY to ₹46 crore, underscoring a sharp profitability turnaround.

- For 9M FY26, revenue grew 12% YoY, while PAT rose 31% YoY, indicating sustained earnings momentum beyond a single quarter.

Business highlights

- ADHO delivered strong double-digit volume growth, supported by higher advertising spends, digital-led campaigns, and continued market share gains across pack sizes.

- General Trade rebounded, aided by urban and rural recovery, while Organized Trade remained robust with modern trade and e-commerce showing healthy traction.

- Coconut oil portfolio recorded high single-digit value growth; pricing and discount correction versus the market leader weighed on near-term volumes but significantly improved profitability.

- Banjara brand (Vishal Personal Care acquisition) posted mid-teens growth, with integration progressing as planned and operating margins stable in the mid-teens.

- International business remained weak YoY due to GCC/Africa softness, though Nepal recovered sequentially and Bangladesh achieved operational breakeven.

Outlook

- Management expects consumption momentum to remain supportive, aided by easing inflation, improving rural demand, and stable macro conditions.

- Gross margins are likely to remain elevated, with copra prices softening sequentially and other key inputs largely range-bound.

- Advertising intensity will remain high, supporting brand salience and sustained volume growth, particularly for ADHO.

- Distribution transformation under the Aarohan program is progressing well, with direct reach already expanded by over 10% and further productivity gains expected.

- Strong cash generation, negligible debt, and improving return ratios position Bajaj Consumer Care well for sustainable earnings growth and margin stability over FY26-27.

Recent Updates on Bajaj Consumer Care Ltd.

- Brand Investments: Continued marketing support for Almond Drops to defend market share.

- Product Refresh: Incremental innovation in natural and ayurvedic variants.

- Operational Focus: Emphasis on supply-chain efficiency and cost optimisation.

- Distribution Strengthening: Gradual expansion of rural and semi-urban reach.

Company valuation insights – Bajaj Consumer Care Ltd.

Bajaj Consumer Care is trading at a TTM P/E of 25.4x, at a meaningful discount to the FMCG peer average of 52.0x, despite delivering a 66.7% return over the past year, significantly outperforming the NIFTY 50’s 9.7% gain. The recent rerating has been driven by a sharp earnings recovery rather than aggressive multiple expansion, with improved growth visibility, margin expansion, and execution-led performance supporting the current valuation.

The investment case is anchored in a structural turnaround in operating performance, led by strong double-digit volume growth in Almond Drops Hair Oil, margin expansion driven by strategic pricing and mix optimisation, and easing input cost pressures, particularly in copra. As highlighted in the concall and investor presentation, the Aarohan distribution transformation has materially improved urban and rural execution, while elevated advertising and digital spends are strengthening brand salience. The coconut oil portfolio has shifted towards profitability-led, brand-driven growth, and the balance sheet remains debt-free with healthy cash generation, supporting sustained investments and calibrated expansion.

From a valuation perspective, applying a 25x multiple to FY27E EPS of ₹14.8, we arrive at a 12-month target price of ₹370, implying an upside of 24% from current levels. On a shorter-term basis, we assign a 3-month target price of ₹316, offering a 6% upside, supported by continued volume momentum, stable input costs, operating leverage, and improving consumption sentiment.

Major risk factors affecting Bajaj Consumer Care Ltd.

- Category Dependence: Heavy reliance on hair oil segment.

- Competitive Intensity: Aggressive pricing and promotions from larger FMCG peers.

- Input Cost Volatility: Almond oil and packaging costs impact margins.

- Limited New-Age Categories: Slower entry into fast-growing personal care segments.

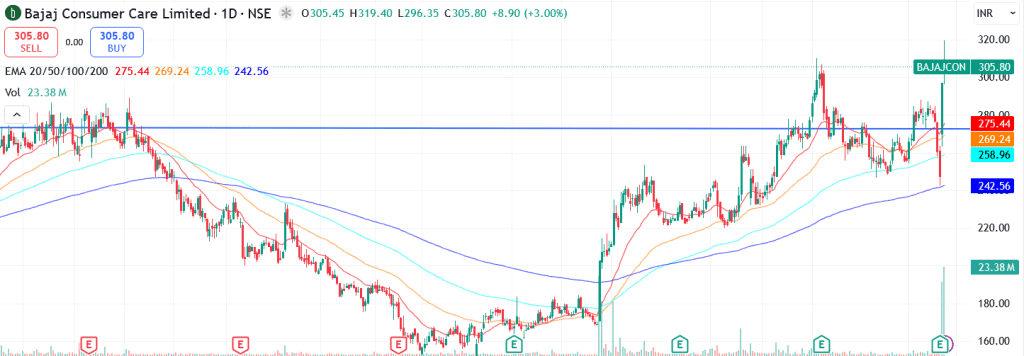

Technical analysis of Bajaj Consumer Care Ltd. share

Bajaj Consumer Care has formed a long-term rounding bottom and has recently delivered a decisive breakout above the neckline, followed by a sharp ~20% post–Q3 FY26 results move, signalling a potential start of a fresh medium- to long-term uptrend. This breakout reflects a clear shift in market sentiment, backed by strong volumes and improving participation, increasing the probability of sustained upside if momentum continues.

The stock is comfortably trading above its 50-, 100-, and 200-day EMAs, indicating that the short-, medium-, and long-term trends are firmly aligned to the upside. This alignment suggests structural strength and reduces downside risk, with pullbacks towards key moving averages likely to attract buying interest from a positional perspective.

Momentum indicators remain constructive. MACD at 5.21 is positive and above the signal line, pointing to continued upside acceleration. RSI at 65.02 reflects strong buying momentum without entering extreme overbought territory, while Relative RSI (0.20 and 0.07 over 21- and 55-day periods) highlights consistent outperformance versus the broader market. ADX at 21.93 indicates a developing trend, with directional strength gradually building.

A decisive move above ₹316 could open the path towards ₹370 (12-month target). On the downside, ₹270 remains a key support level; holding above this zone keeps the bullish structure intact.

- RSI: 65.02 (Strong Buying Momentum)

- ADX: 21.93 (Developing Trend Strength)

- MACD: 5.21 (Positive, above the signal line)

- Resistance: ₹316

- Support: ₹270

Bajaj Consumer Care Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹316 (6% upside) and a 12-month target of ₹370 (24% upside), based on 25x FY27E EPS of ₹14.8.

Why buy now?

Earnings upcycle underway: Strong double-digit volume growth in Almond Drops Hair Oil, operating leverage, and structurally higher gross margins are driving a sustained earnings recovery.

Execution-led growth visibility: The Aarohan distribution transformation has improved urban and rural execution, while elevated advertising and digital spends are strengthening brand salience and market share.

Margin tailwinds: Strategic pricing actions, favourable product mix, and easing copra prices support margin stability despite competitive intensity.

Balance sheet strength: Debt-free status and healthy cash generation provide flexibility to sustain brand investments and pursue calibrated portfolio expansion.

Portfolio fit

Bajaj Consumer Care offers quality FMCG exposure with improving growth and margin visibility, combining a resilient core brand franchise with an ongoing execution turnaround. Trading at a discount to FMCG peers despite superior recent performance, the stock fits well in portfolios seeking earnings recovery stories, consumption-led growth plays, and disciplined compounders, complementing core holdings in large-cap FMCG and discretionary consumption.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebBajaj Consumer Care Ltd.: Budget 2025-26 opportunities

- Rural Consumption Push: Higher rural spending and income support boost FMCG demand.

- Tax Relief for Consumers: Increased disposable income aids discretionary consumption.

- Agri & Farmer Support: Stronger farm incomes support rural FMCG volumes.

- Logistics & Infra Spend: Better connectivity improves distribution efficiency.

- MSME & Manufacturing Support: Lower operating costs across supply chains.

Final thoughts

Bajaj Consumer Care is not a flashy FMCG growth story, it is a cash-generating, brand-led, defensive business anchored in a core category. For investors seeking stability, predictable cash flows, and downside protection rather than rapid expansion, BCCL offers a steady seat in India’s everyday consumption journey, with optional upside from premiumisation and rural demand recovery.