India’s growth is powered not just by large-scale infrastructure but also by reliable, decentralized energy solutions, from factories and construction sites to agriculture and backup power needs. In an economy where uninterrupted power is still evolving, engines and generator sets remain indispensable.

At the intersection of industrial demand, rural applications, and infrastructure growth stands Kirloskar Oil Engines Ltd. (KOEL), a legacy engineering company adapting to modern energy needs.

But does Kirloskar Oil Engines Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | KIRLOSENG |

| Industry/Sector | Capital Goods |

| CMP | 1410.00 |

| Market Cap (₹ Cr.) | 20,496 |

| P/E | 37.79 (Vs Industry P/E of 33.81) |

| 52 W High/Low | 1530.00 / 578.50 |

| EPS (TTM) | 36.72 |

| Dividend Yield | 0.47% |

About Kirloskar Oil Engines Ltd.

Kirloskar Oil Engines Limited is one of India’s leading manufacturers of diesel engines, generator sets, and power solutions. Part of the Kirloskar Group, the company has a strong presence across industrial, agricultural, and infrastructure segments.

With decades of engineering expertise, KOEL has built a diversified portfolio catering to domestic and global markets. The company is also gradually transitioning toward cleaner fuel technologies, including gas-based engines, aligning with evolving emission norms and sustainability trends.

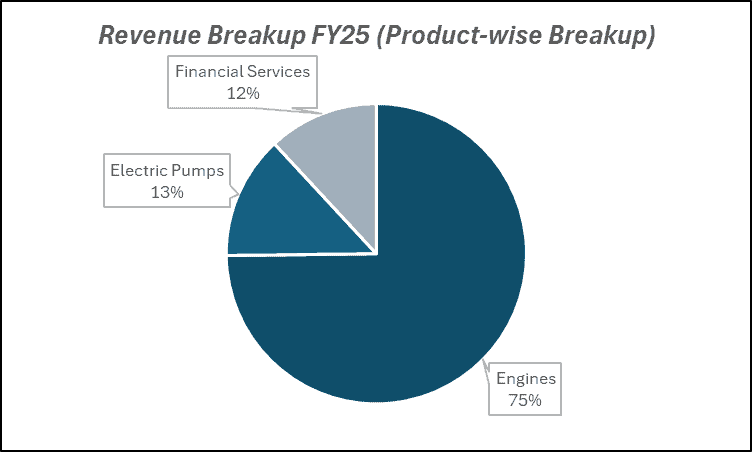

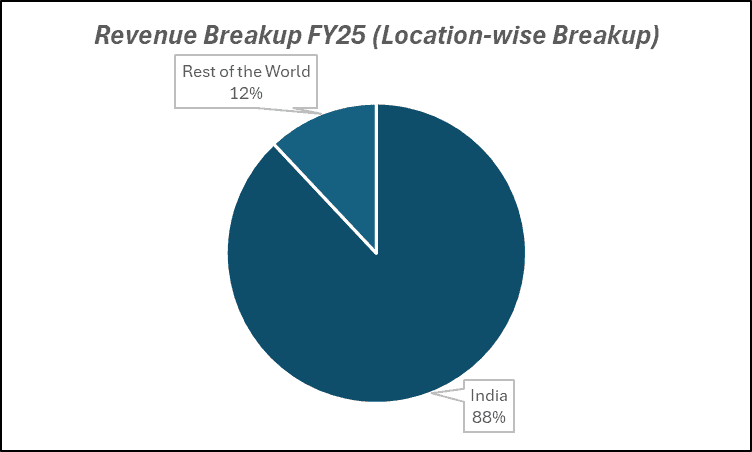

Key business segments

Kirloskar Oil Engines Ltd. operates primarily in the following key business segments:

- Power Generation (Gensets): Diesel and gas-based generator sets for industrial and commercial use.

- Industrial Engines: Engines for construction, mining, and industrial applications.

- Agriculture Engines: Engines for irrigation pumps and rural applications.

- International Business: Export of engines and power solutions globally.

- Clean Energy Solutions: Gas-based and emission-compliant engine technologies.

Primary growth factors for Kirloskar Oil Engines Ltd.

Kirloskar Oil Engines Ltd. key growth drivers:

- Infrastructure & Capex Revival: Increased demand from construction, industrial, and infrastructure sectors.

- Backup Power Demand: Rising need for reliable power solutions across commercial and residential segments.

- Export Growth Opportunities: Expansion into international markets driving revenue diversification.

- Shift Toward Cleaner Technologies: Transition to gas-based and emission-compliant engines.

- Agriculture Mechanization Growth: Rising demand for irrigation and farm engines.

Detailed competition analysis for Kirloskar Oil Engines Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Kirloskar Oil Engines Ltd. | 7337.67 | 1353.12 | 18.44% | 529.06 | 7.21% | 37.79 |

| Bharat Heavy Electricals Ltd. | 30465.18 | 1420.77 | 4.66% | 760.05 | 2.49% | 106.00 |

| Thermax Ltd. | 10343.69 | 951.62 | 9.20% | 681.12 | 6.58% | 57.61 |

| Jyoti CNC Automation Ltd. | 2069.65 | 557.00 | 26.91% | 354.40 | 17.12% | 49.65 |

| Triveni Turbine Ltd. | 2039.50 | 442.70 | 21.71% | 343.10 | 16.82% | 42.79 |

Key insights on Kirloskar Oil Engines Ltd.

- Strong legacy brand with extensive distribution network.

- Diversified end-user base across industrial, rural, and export markets.

- Beneficiary of India’s capex and infrastructure cycle.

- Increasing focus on cleaner and compliant engine technologies.

- Operating leverage plays out strongly during demand upcycles.

Recent financial performance of Kirloskar Oil Engines Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 1449.31 | 1948.38 | 1872.60 | -3.89% | 29.21% |

| EBITDA (₹ Cr.) | 252.54 | 381.75 | 331.45 | -13.18% | 31.25% |

| EBITDA Margin (%) | 17.42% | 19.59% | 17.70% | -189 bps | 28 bps |

| PAT (₹ Cr.) | 66.56 | 159.19 | 109.13 | -31.45% | 63.96% |

| PAT Margin (%) | 4.59% | 8.17% | 5.83% | -234 bps | 124 bps |

| Adjusted EPS (₹) | 4.91 | 11.18 | 7.66 | -31.48% | 56.01% |

Kirloskar Oil Engines Ltd. financial update (Q3 FY26)

Financial performance

- Revenue grew 29% YoY to ₹1,873 Cr, driven by strong traction across Power Gen and Industrial segments.

- EBITDA increased 31% YoY to ₹331 Cr, with margins expanding 28 bps YoY to 17.7%, supported by operating leverage.

- PAT rose 64% YoY to ₹109 Cr, aided by strong operating performance and margin expansion.

- EBIT growth remained robust at 34% YoY, reflecting improved cost efficiencies and better product mix.

- Margins saw improvement across levels (EBITDA, EBIT, PAT), indicating gradual profitability enhancement despite RM cost pressures.

Business highlights

- Power Gen segment grew 44% YoY to ₹600 Cr, driven by strong retail demand and rising HHP contribution.

- The industrial segment delivered 41% YoY growth, led by defense, marine, and nuclear execution.

- HHP segment volumes surged 235% YoY, emerging as a key growth driver with strong infra and data center demand.

- International B2B business grew 26% YoY, reflecting improving export traction across key geographies.

- Distribution & aftermarket delivered steady double-digit growth, supporting margin stability and recurring revenue streams.

Outlook

- Revenue/EBITDA expected to grow at 16%/22% YoY in FY26E, supported by domestic capex upcycle.

- Strong focus on the High Horsepower (HHP) segment provides a long runway for growth and margin expansion.

- Rising demand from data centers, infrastructure, and real estate to drive sustained volume growth.

- Export expansion (SE Asia, US, Africa) under 3C strategy (Capability, Capacity, Coverage) to aid diversification.

- Healthy balance sheet and planned capex (₹7Bn) to support capacity expansion and long-term growth visibility.

Recent Updates on Kirloskar Oil Engines Ltd.

- Expansion of emission-compliant product portfolio.

- Increased focus on gas-based and alternative fuel engines.

- Strengthening export footprint in emerging markets.

- Capacity expansion and operational efficiency initiatives.

- Participation in infrastructure-led demand recovery.

Company valuation insights – Kirloskar Oil Engines Ltd.

Kirloskar Oil Engines is currently trading at a TTM P/E of 37.8x, slightly above the industry average of 33.8x, after delivering a strong 99% return over the last one year, significantly outperforming the NIFTY 50 which gained 3.6% during the same period.

The investment case for Kirloskar Oil Engines is supported by its strong presence across power generation and industrial segments, along with a focused strategy to scale up the high horsepower (HHP) segment, which offers significant growth headroom. The company is witnessing robust demand across infrastructure-led sectors such as real estate, defense, marine, and data centers, driving volume growth and improving product mix. Additionally, its expanding aftermarket and export business, coupled with a strategic push towards capability enhancement and service quality in the HHP segment, positions it well to benefit from the ongoing domestic capex upcycle. With improving margins, strong order pipeline, and increasing diversification across geographies, the company is well placed to deliver sustained earnings growth over the medium to long term.

From a valuation perspective, applying a 35x EV/EBITDA multiple to FY28E EPS of ₹50, we derive a 12-month target price of ₹1,750, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹1,500, indicating a 6% upside, supported by strong earnings momentum, improving mix towards HHP, and continued demand strength across key segments.

Major risk factors affecting Kirloskar Oil Engines Ltd.

- Cyclical Demand Risk: Dependence on infrastructure and industrial activity.

- Raw Material Cost Risk: Volatility in input prices affecting margins.

- Regulatory Risk: Stricter emission norms requiring continuous upgrades.

- Competition: Intense competition from domestic and global players.

- Energy Transition Risk: Shift toward electrification reducing diesel engine demand.

Technical analysis of Kirloskar Oil Engines Ltd. share

Kirloskar Oil Engines is currently in a structural uptrend, outperforming the broader market, with the stock trading comfortably above its key moving averages. This indicates sustained buying interest and a strong underlying trend, supported by improving fundamentals and sector tailwinds.

The stock is trading above its 20-, 50-, 100-, and 200-day EMAs, reflecting continued strength across short- to long-term timeframes. While the broader trend remains positive, the price is currently consolidating near key levels, suggesting a potential buildup before the next leg of the up move.

Momentum indicators remain constructive. The MACD at 2.48 is in positive territory but slightly below the signal line, indicating a potential bullish crossover in the near term. The RSI at 50.85 reflects decent buying interest without being overbought, while the 21-day and 55-day Relative RSI at 0.10 and 0.35 indicate relative outperformance against the broader market. Meanwhile, the ADX at 18.26 suggests that the trend is gradually strengthening, supporting the continuation of the uptrend.

A decisive move above ₹1,500 could trigger further upside towards ₹1,750, aligning with our 12-month fundamental target. On the downside, ₹1,320 acts as a key support level, below which the current bullish structure may weaken.

- RSI: 50.85 (Decent buying interest)

- ADX: 18.26 (Trend strengthening)

- MACD: 2.48 (Positive; bullish crossover likely)

- Resistance: ₹1,500

- Support: ₹1,320

Kirloskar Oil Engines Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹1,500 (6% upside) and a 12-month target of ₹1,750 (24% upside), based on 35x FY28E EPS.

Why buy now?

Strong growth visibility driven by the domestic capex upcycle, with rising demand across infrastructure, real estate, and industrial segments.

Rapid scale-up in the High Horsepower (HHP) segment, offering significant headroom for growth and margin expansion.

Robust demand from data centers, defense, marine, and nuclear segments, supporting diversified revenue streams.

Improving product mix and operating leverage, leading to steady margin expansion over the medium term.

Increasing traction in exports and aftermarket services, enhancing revenue stability and long-term profitability.

Portfolio fit

Kirloskar Oil Engines offers exposure to India’s industrial and infrastructure growth cycle, backed by strong positioning in power generation and industrial engines. With a clear strategic focus on scaling the high-margin HHP segment, expanding exports, and capitalising on demand from data centers and infrastructure, the company is well placed to benefit from the ongoing capex cycle. Supported by improving margins, strong execution across segments, and a diversified end-market presence, the stock fits well in portfolios seeking cyclical growth with structural tailwinds and improving return ratios.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebKirloskar Oil Engines Ltd.: Budget 2026-27 opportunities

- Infrastructure Spending Boost: Higher demand from construction and industrial projects.

- Rural Development Push: Increased mechanization supporting agriculture engine demand.

- Make in India Initiatives: Manufacturing incentives supporting domestic production.

- Energy Reliability Focus: Demand for backup power solutions across sectors.

- Cleaner Energy Incentives: Support for gas-based and low-emission technologies.

Final thoughts

Kirloskar Oil Engines Limited stands at an important transition point, balancing its legacy diesel engine business with emerging opportunities in cleaner energy solutions. With strong positioning across industrial, rural, and export markets, and clear tailwinds from India’s capex cycle, the company is well placed to deliver cyclical growth with long-term adaptability.

For investors seeking exposure to India’s infrastructure and industrial expansion with a blend of cyclical upside and gradual transition toward future-ready technologies, KOEL offers a compelling engineering-led growth story.