In a world transitioning toward clean energy, traditional energy companies often sit at the crossroads of opportunity and disruption. Amid global crude volatility, geopolitical shifts, and India’s push for energy security, upstream oil companies are once again drawing investor attention.

One such company is Oil India Limited (OIL), a PSU major that plays a critical role in India’s hydrocarbon ecosystem. With improving crude realizations, disciplined capex, strong dividend payouts, and strategic diversification into renewables and gas infrastructure, Oil India stands at an interesting valuation zone.

But does Oil India Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | OIL |

| Industry/Sector | Oil & Gas |

| CMP | 485.55 |

| Market Cap (₹ Cr.) | 78,980 |

| P/E | 11.88 (Vs Industry P/E of 9.90) |

| 52 W High/Low | 524.00 / 325.00 |

| EPS (TTM) | 40.72 |

| Dividend Yield | 2.38% |

About Oil India Ltd.

Oil India Limited is a Government of India-owned upstream oil and gas exploration and production company and the second-largest national oil producer in the country after Oil and Natural Gas Corporation in terms of output. Established in 1959 and headquartered in Noida, the company focuses on the exploration, development, and production of crude oil and natural gas.

With majority ownership held by the Government of India, Oil India plays a strategic role in strengthening the nation’s energy security. Its core operations are concentrated in Assam, Rajasthan, and select offshore fields, while it also maintains overseas exploration and production interests in countries such as Mozambique and Russia through consortium partnerships.

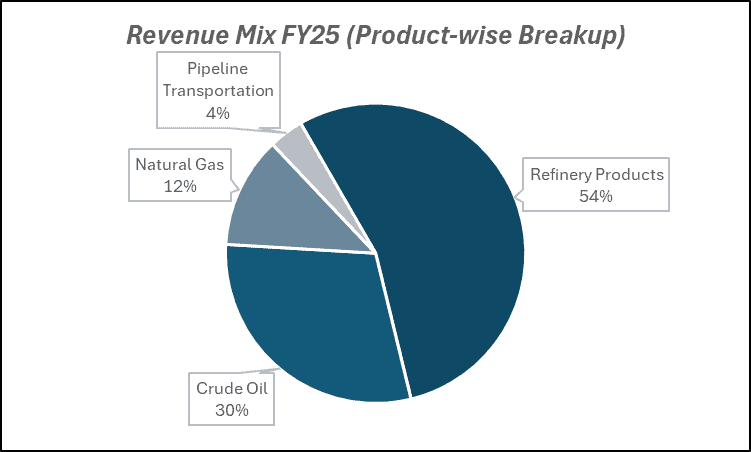

Key business segments

Oil India Ltd. operates primarily in the following key business segments:

- Crude Oil (India): Onshore & offshore exploration and production of crude oil.

- Natural Gas: Production and sale of gas to fertilizer, power, and CGD players.

- Pipelines: Transportation of crude oil and natural gas.

- Overseas E&P: International oil & gas assets through consortiums.

- Renewables: Investments in solar, wind, and clean energy projects.

Primary growth factors for Oil India Ltd.

Oil India Ltd. key growth drivers:

- Higher Crude Oil Realizations: Realizations linked to global crude benchmarks support profitability during favorable price cycles.

- Gas Monetization Opportunities: Rising domestic gas demand (fertilizers, CGD, power) improves volume visibility.

- Government Focus on Energy Security: India aims to reduce import dependency, which supports domestic E&P players.

- Capex-Led Production Expansion: Aggressive drilling programs and enhanced recovery techniques may improve output.

- Diversification into Renewables & Green Energy: Investments in solar and clean energy projects de-risk long-term transition risk.

Detailed competition analysis for Oil India Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Oil India Ltd. | 36624.60 | 10024.99 | 27.37% | 6190.99 | 16.90% | 11.88 |

| ONGC Ltd. | 659253.86 | 99848.28 | 15.15% | 44123.36 | 6.69% | 7.83 |

| Indian Oil Ltd. | 885913.61 | 67287.18 | 7.60% | 34263.00 | 3.87% | 7.18 |

| BPCL Ltd. | 514788.69 | 38862.22 | 7.55% | 22299.67 | 4.33% | 6.80 |

| Hindustan Petroleum Ltd. | 473646.66 | 27217.18 | 5.75% | 14845.74 | 3.13% | 6.07 |

Key insights on Oil India Ltd.

- Strong asset base with long reserve life.

- Historically high dividend payout, making it attractive for income-focused investors.

- Operating leverage benefits during crude upcycles.

- PSU status provides strategic importance but also regulatory sensitivity.

- Improving balance sheet over cycles, but capex remains ongoing.

Recent financial performance of Oil India Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 9089.14 | 9175.41 | 9111.43 | -0.70% | 0.25% |

| EBITDA (₹ Cr.) | 2678.11 | 2303.48 | 2510.19 | 8.97% | -6.27% |

| EBITDA Margin (%) | 29.46% | 25.10% | 27.55% | 245 bps | -191 bps |

| PAT (₹ Cr.) | 1593.17 | 1440.25 | 1659.42 | 15.22% | 4.16% |

| PAT Margin (%) | 17.53% | 15.70% | 18.21% | 251 bps | 68 bps |

| Adjusted EPS (₹) | 8.23 | 8.78 | 7.35 | -16.29% | -10.69% |

Oil India Ltd. financial update (Q3 FY26)

Financial performance

- Revenue flat at 0.25% YoY to ₹9111 Cr in Q3FY26, impacted by lower oil realizations (USD62.8/bbl vs USD68.2/bbl QoQ).

- EBITDA fell 6% YoY to ₹2510 Cr; margins contracted to 27.6% amid higher other expenses and one-offs.

- Adjusted PAT flat at 4% YoY to ₹1659 Cr due to lower realizations and elevated write-offs.

- 9MFY26 revenue fell 7% YoY to ₹153.9bn, while EBITDA dropped 38% YoY to ₹42.4bn.

- 9MFY26 adjusted PAT declined 41% YoY to ₹26.7bn, reflecting weaker price environment and provisions.

Business highlights

- Oil production rose 1.2% QoQ to 0.9mmt; gas production remained flat at 0.8bcm in Q3FY26.

- FY27/FY28 oil production guided at 3.8mmt/4.0mmt; gas ramp-up contingent on evacuation infrastructure.

- ~75 wells planned in FY26 and ~100 wells in FY27 to support medium-term volume growth.

- NRL reported strong GRM of USD16.3/bbl in Q3, sharply improving refining EBITDA.

- Expanded NRL capacity stabilization underway; meaningful refining contribution expected from FY28.

Outlook

- Management expects FY26 production to surpass FY25 levels despite near-term price volatility.

- Medium-term target of 4mmt oil and 5bcm gas, though timelines may see moderation.

- Elevated capex (₹88bn+ in FY26; higher in FY27) to support drilling and development activity.

- Strong NRL ramp-up and petchem commissioning by FY28–29 to diversify earnings mix.

- Improving realizations and volume growth could restore margins toward 38–42% over FY27–28.

Recent Updates on Oil India Ltd.

- Participation in new exploration blocks under OALP (Open Acreage Licensing Policy).

- Increased capex guidance for production enhancement.

- Strategic tie-ups for renewable energy expansion.

- Government policy changes around windfall tax adjustments.

- Progress in overseas asset development projects.

Company valuation insights – Oil India Ltd.

Oil India is currently trading at a TTM P/E of 11.88x, compared to the industry average of 9.90x, after delivering a strong 42.12% return over the last one year, significantly outperforming the NIFTY 50’s 13.83% gain. The re-rating reflects improving production visibility, resilient realizations, and growing confidence in medium-term volume recovery, despite near-term earnings moderation due to lower oil prices and elevated write-offs.

The investment case for Oil India is anchored in steady upstream production growth, improving refining contribution from NRL, and disciplined capital allocation. Management has guided crude production at 3.8mmt in FY27 and 4.0mmt in FY28, with gas volumes expected to ramp up subject to evacuation infrastructure. The company plans to drill 75 wells in FY26 and 100 wells in FY27 to support medium-term output growth. While recent earnings were impacted by lower oil realizations and one-off write-offs, operational momentum remains intact. Importantly, NRL has reported a sharp improvement in GRMs, strengthening refining profitability and diversifying earnings beyond core E&P. Capacity expansion and petrochemical commissioning by FY28–29 further enhance earnings visibility.

From a valuation standpoint, applying a 12x multiple to FY27E EPS of ₹50, we arrive at a 12-month target price of ₹600, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹515, indicating a 6% upside, supported by stable realizations, gradual production ramp-up, improving refining margins, and sustained capital discipline.

Major risk factors affecting Oil India Ltd.

- Commodity Price Risk: Earnings remain highly sensitive to crude oil and gas price volatility.

- Regulatory Risk: Windfall taxes, subsidy policies, and government pricing interventions can impact profitability.

- Production Risk: Delays in drilling, reserve replacement challenges, or lower-than-expected output growth.

- Geopolitical Exposure: Overseas assets may face political instability or operational disruptions.

- Capital Intensity: Sustained capex requirements for exploration and development can pressure free cash flows.

Technical analysis of Oil India Ltd. share

Oil India is forming a cup and handle pattern, signalling a constructive consolidation phase within a broader uptrend. The stock is currently trading near the neckline zone, and a decisive breakout above this level could trigger a strong upward move, confirming continuation of the primary trend.

Importantly, the price is trading above its 20-, 50-, 100-, and 200-day EMAs, indicating strong structural alignment across timeframes. This suggests that the broader trend remains positive, with moving averages likely to act as dynamic support during near-term volatility.

Momentum indicators suggest improving strength. The MACD at 4.39 is in positive territory but currently just below the signal line; a bullish crossover alongside a neckline breakout would strengthen the entry signal.

RSI at 57.15 reflects healthy buying interest without being overbought, leaving room for further upside. The 55-day Relative RSI at 0.24 indicates strong outperformance versus the broader market. Meanwhile, ADX at 17.55 signals that the trend is developing and could strengthen further upon breakout confirmation.

A sustained move above ₹515 (neckline resistance) could open the path toward ₹600 and beyond, aligning with our 12-month fundamental target. On the downside, ₹450 remains a crucial support level; holding above this zone preserves the cup and handle structure and limits downside risk.

- RSI: 57.15 (Bullish; healthy buying interest)

- ADX: 17.55 (Developing trend)

- MACD: 4.39 (Positive; crossover awaited)

- Resistance: ₹515

- Support: ₹450

Oil India Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹515 (6% upside) and a 12-month target of ₹600 (24% upside), based on 12x FY27E EPS of ₹50.

Why buy now?

Improving production visibility with crude guidance of 3.8–4.0 mmt over FY27–28 and steady gas ramp-up, supporting medium-term earnings stability.

Strong upstream asset base with increased drilling intensity (75–100 wells annually) enhancing reserve replacement and output growth.

Diversified earnings profile with improving refining contribution from NRL and upcoming petrochemical integration.

Healthy balance sheet with low leverage and strong operating cash flows, enabling sustained capex without stressing returns.

Attractive valuation relative to growth recovery potential, with earnings expected to normalize as realizations stabilize and volumes improve.

Portfolio fit

Oil India offers exposure to India’s energy security theme through a stable upstream franchise complemented by refining and petrochemical optionality. With disciplined capital allocation, improving return ratios over FY27–28, and reasonable valuations compared to broader markets, the stock fits well in portfolios seeking a blend of cyclical recovery, dividend yield, and strategic commodity exposure.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebOil India Ltd.: Budget 2026-27 opportunities

- Incentives for Domestic Hydrocarbon Exploration: Fiscal incentives for domestic E&P may boost investment returns.

- Gas Infrastructure Push: Expansion of CGD networks and gas-based economy initiatives.

- Strategic Petroleum Reserves Expansion: Strengthening domestic energy security frameworks.

- Tax Rationalization for Upstream Companies: Reduction or clarity on windfall taxes.

- Renewable Integration Incentives: Subsidies or viability gap funding for PSU-led renewable projects.

Final thoughts

Oil India Limited stands at a strategic crossroads, balancing its legacy role as a government-backed upstream producer with the evolving realities of energy transition and capital discipline. Supported by India’s focus on energy security, stable domestic production assets, and diversification into gas and renewables, the company is positioning itself to navigate commodity cycles with greater resilience.

For investors seeking exposure to India’s hydrocarbon value chain with strong dividend potential and cyclical upside during favorable crude cycles, Oil India offers a blend of cash-flow visibility, policy-backed strategic relevance, and long-term optionality from diversification initiatives.