Summary

The 7-5-3-1 rule in SIP is an investment approach designed to encourage long-term discipline and consistency. It is based on four principles: staying invested for at least 7 years, diversifying across 5 equity categories, preparing for 3 common investor emotions, and increasing SIP contributions by 10% each year. Understanding these principles can help you build a more organised and methodical way of investing for the long term.

What Is 7-5-3-1 Rule in SIP?

The 7-5-3-1 rule in SIP is a framework built around four principles: the right time period, the right diversification approach, the right mental preparation, and the right way to grow contributions over time. Together, these four numbers address the most common reasons SIP investors either underperform or exit too soon.

The 7-5-3-1 is a strategy that connects investment longevity, allocation spread, behavioural control, and contribution scaling within equity mutual fund investing. The approach highlights four core investing habits: remaining invested for longer durations, maintaining balanced exposure, managing emotional reactions, and gradually raising contribution amounts. Each number in the rule addresses a specific dimension of investing not just what to do, but how to think about it across the long investment cycle.

How the 7-5-3-1 Rule Works in Real Market Conditions

Each of the four numbers in the rule addresses a specific dimension of investing behaviour, as follows.

The 7: Invest for a minimum of 7 years

The first and most foundational principle is time. Equity markets have historically moved through recovery phases over a 7-year period despite intermittent corrections. Investing in equity SIPs for a minimum of seven years allows the power of compounding to take full effect.

In real market terms, the Indian equity market has gone through multiple sharp corrections, each of which shook investors with a short-term view. Those who stayed invested across those cycles saw portfolios recover and grow well beyond previous highs. Incorporating a seven-year duration gives the strategy enough time to move through both downturns and recovery phases. Compounding is largely invisible in the first three to four years, it becomes powerful from year five onward. Committing to seven years guarantees the investor stays long enough to see it work.

The 5: Diversify across 5 types of equity

The second principle is diversification not across random funds, but across five specific types of equity that serve different roles. The 5 Finger Framework recommends distributing investments across varied equity styles instead of concentrating exposure within a single segment. These segments include high-quality large cap stocks, value stocks, GARP stocks, midcap or small cap stocks, and global stocks.

Each category behaves differently across market conditions. Large cap stocks provide stability during downturns. Value stocks currently undervalued by the market tend to deliver strong returns when markets mean-revert. GARP (Growth at Reasonable Price) stocks are companies in emerging sectors growing faster than the market without extreme valuations. Midcap and small cap stocks carry higher risk but significant growth potential. Certain small-cap categories have, during expansionary market phases, recorded annual appreciation levels crossing 60%. Global stocks add geographical diversification, protecting the portfolio from purely domestic economic cycles.

For a retail investor, this translates practically into: one large cap or index fund, one value fund, one flexi cap fund, one small cap fund, and one international fund each serving a distinct function.

The 3: Prepare for 3 psychological phases

Among all parts, this factor is often neglected during portfolio planning discussions. Equity SIP investors typically face three challenging phases: the Disappointment Phase, the Irritation Phase, and the Panic Phase.

The Disappointment Phase arrives when returns are 7–10% positive but not as exciting as expected. Investors compare with peers or fixed deposit rates and feel their SIP is underperforming. The Irritation Phase follows when returns fall to 0–7% during a sideways market. Weak market phases sometimes increase investor preference for fixed-return alternatives over equity-linked participation. Recognising that market fluctuations are normal and SIPs are designed for long-term growth helps maintain perspective.

The Panic Phase suggests interrupted SIP journeys occur during the first sustained period of portfolio decline. The portfolio falls below the total invested amount. Emotional exits during drawdowns frequently damage continuity more than the correction itself. Recovery phases in equities have often emerged after correction cycles, benefiting investors who maintained contribution continuity.

Every long-term SIP investor passes through all three phases, sometimes more than once. Knowing they are coming in advance converts them from exit triggers into recognisable stages of a normal investment journey.

The 1: Increase SIP by 10% annually

The final principle is incremental growth. Increasing your SIP amount by 10% every year in line with income growth dramatically improves long-term outcomes without requiring a large upfront commitment. A flat SIP loses real value to inflation every year; the step-up corrects for this automatically.

For most working professionals whose income grows each year, a 10% annual increase is not a financial burden. It is simply redirecting a portion of the annual increment back into long-term compounding. The additional contributions happen precisely in the years when the portfolio has already been building value, making each step-up more impactful than the last.

Real-Life Investor Scenarios & Examples

Understanding these numbers in isolation is one thing. Seeing how they interact in practice makes the framework genuinely useful.

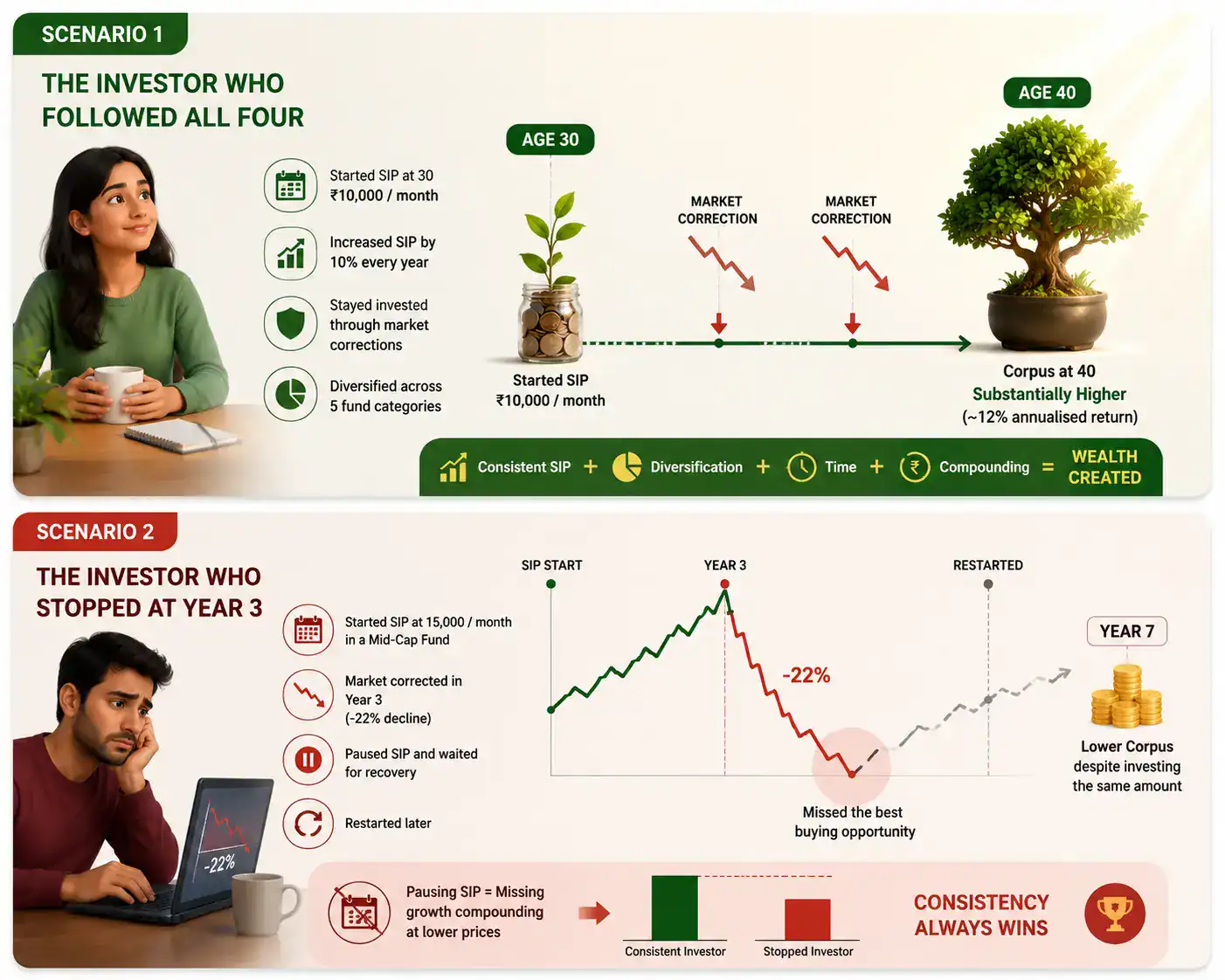

Scenario 1: The Investor Who Followed All Four

Reena started a ₹10,000 monthly SIP at age 30 across five fund categories: a large-cap fund, a flexi-cap fund, a mid-cap fund, a small-cap fund, and a hybrid fund. She increased her SIP by 10% every year and stayed invested through two significant market corrections over the following decade. By 40, her total invested amount was approximately ₹19 lakhs. Her corpus, assuming a blended 12% annualised return, would be substantially higher due to the combined effect of step-ups and compounding. She did not time the market once.

Scenario 2: The Investor Who Stopped at Year 3

Vikram started a ₹15,000 monthly SIP in a single mid-cap fund. When the market corrected sharply in year three, his portfolio showed a 22% decline. He paused the SIP and waited for the market to recover before restarting. By pausing, he missed buying units at lower prices during the recovery phase, the period where SIP investors historically gain the most units per rupee. His final corpus at year seven was noticeably lower than if he had stayed consistent, despite investing the same total amount.

The contrast between these two scenarios captures exactly what the 7-5-3-1 rule tries to prevent.

Benefits of Understanding the 7-5-3-1 Rule

The 7-5-3-1 rule offers SIP investors various advantages such as:

- It tells you exactly when not to exit: Most SIP investors exit at the wrong time during corrections or flat phases. The rule predefines three psychological phases so investors can identify where they are in the cycle rather than treating every downturn as a reason to stop.

- It prevents the most expensive mistake in SIP investing: Stopping a SIP during negative returns and restarting after recovery means buying high after selling low, the opposite of what compounding requires. The 7-year commitment removes this option from the investor’s mental toolkit.

- It makes diversification actionable, not theoretical: Most investors know diversification matters but do not know how to implement it. The five-category framework gives a specific, practical allocation structure rather than a vague instruction to spread risk.

- It turns income growth into wealth growth automatically: Without the annual step-up, a flat SIP becomes smaller in real terms every year as inflation rises. The annual increase ensures contributions remain meaningful relative to goals without requiring any active decision each year beyond executing the increase.

- It reframes market corrections as opportunities: Because the rule prepares investors for the panic phase in advance, a portfolio drawdown becomes an expected stage rather than an emergency. Investors who stay invested through corrections benefit from lower NAVs, buying more units at reduced prices before the recovery.

Common Mistakes Investors Make

Knowing the rule and following it through real market conditions are two different things. These are the gaps where most investors fall short:

- Treating 7 years as the exit point, not the starting point

The rule sets seven years as a floor. Investors who plan to exit exactly at year seven often do so just before a strong market phase.

- Diversifying within the same category

Holding five large cap funds is not the five-category system, it is concentration in disguise. Each of the five must serve a genuinely different risk-return function.

- Skipping the annual step-up

A flat SIP loses real value to inflation every year. The 10% step-up is not optional, it is what keeps contributions meaningful relative to financial goals over time.

- Exiting during the irritation phase

When SIPs return 3–5% in a sideways market, many investors conclude the strategy has failed. This is precisely the phase where stopping destroys future returns, the market recovery that follows rewards only those still invested.

- Starting without preparing for the panic phase

The most common SIP exit happens when portfolio value falls below invested amount. Investors who have not mentally prepared for this interpret temporary drawdown as permanent loss and sell at exactly the wrong moment.

Conclusion

Understanding what is 7-5-3-1 rule in SIP does not remove uncertainty from investing, it builds investor behaviour around it. Markets will correct, phases will test patience, and the step-up will feel unnecessary in a bad year. Investors who follow the framework anyway, consistently, across full market cycles are the ones who eventually look back and realise compounding did exactly what it was always meant to do.

FAQs

Yes, beginners can use the 7-5-3-1 rule because it offers a structured approach focused on diversification, gradual investing, realistic expectations, and future wealth building.

SIPs are generally a better choice for long-term investing because market volatility smooths out over time, allowing compounding and rupee-cost averaging to work more effectively.

The 7-5-3-1 rule helps SIP investors stay disciplined by combining long investment duration, diversification, emotional preparedness during volatility, and annual SIP increases for stronger wealth creation.

No, the 7-5-3-1 rule is not a guaranteed return formula. It is a planning framework designed to support consistent investing habits and realistic financial expectations.