Summary

A portfolio combines different investments such as stocks, mutual funds, bonds and ETFs to reduce risk and support long-term financial goals.

Building a strong portfolio requires clear goals, suitable asset allocation, sector diversification and regular rebalancing.

Investors should avoid concentrated bets, emotional decisions, frequent trading and ignoring costs, taxes or portfolio reviews.

What is a Portfolio in the Share Market

A portfolio in the share market is a collection of financial assets held by an investor typically spanning stocks, mutual funds, ETFs, bonds, and sometimes cash equivalents with the goal of generating returns while managing risk in a structured way.

The key word here is collection. A single stock is a bet. A portfolio is a strategy. When you own multiple assets across different sectors, market caps, and instrument types, the performance of one holding doesn’t determine your entire financial outcome. If your pharma stock falls 20% but your IT holdings are up 15% and your index fund is steady, your overall portfolio absorbs that shock far better than a concentrated position ever could.

In relation to the stock market, a portfolio reflects your investment philosophy, risk appetite, and financial goals all in one place. It’s not set in stone, it evolves as markets move, your life changes, and your understanding of investing deepens. The portfolio is, in essence, the operating structure of your wealth-building journey

Types of Portfolio in Share Market

Portfolio diversification is not simply about owning more, it’s about owning the right combination for your specific situation. The major portfolio types are:

- Growth portfolio

Focused entirely on capital appreciation. A growth portfolio primarily consists of high-growth stocks and equity funds where investors are willing to accept higher levels of risk for the possibility of earning higher returns. These portfolios are best suited for young investors with a long investment horizon who can absorb short-term volatility.

- Income portfolio

Designed to generate regular income rather than aggressive growth. These typically include dividend-paying stocks, bonds, REITs, and fixed-income instruments. Retirees and conservative investors tend to favour this structure.

- Balanced portfolio

A blend of equity and debt, typically in ratios like 60:40 or 70:30, depending on the investor’s age and goals. This is the most commonly recommended structure for retail investors who want growth with some downside protection.

- Aggressive portfolio

High allocation to equities, particularly small-caps and thematic or sectoral funds. Carries significant risk but targets maximum growth. Only suitable for investors with high risk tolerance and long investment periods.

- Defensive portfolio

Concentrated in sectors that hold up well during economic downturns, such as healthcare, utilities, and consumer staples. These portfolios sacrifice high returns in exchange for stability during volatile periods.

- Value portfolio

Built around stocks that appear undervalued relative to their fundamentals. The investor buys at a discount and waits for the market to correct the mispricing. This approach requires patience and strong fundamental analysis skills.

How to Build a Portfolio (Step-by-Step Guide)

Building a portfolio well requires more than just selecting the stocks, as the following steps show.

Step 1: Define the goal behind

Vague goals produce vague portfolios. A corpus for your child’s education in 12 years has a hard deadline, which means it needs a different risk profile than money you are growing without a fixed end date. The goal determines everything that follows.

Step 2: Allocate by sleep threshold, not just age

Standard age-based allocation rules are a starting point, not a prescription. The real test is whether you can hold your position through a 30% market drawdown without selling. If not, your equity allocation is too high regardless of what any formula suggests.

Step 3: Size sectors, not just stocks

Picking good stocks within one sector still leaves you exposed to a single economic cycle. Spreading across uncorrelated sectors, such as financials, pharmaceuticals, and consumption, means one sector downturn does not define your annual return.

Step 4: Treat the first rebalance as the real test

Anyone can build a portfolio in a rising market. Rebalancing when one asset class has surged means trimming what feels like a winner. That discipline, selling what has done well to buy what has lagged, is what separates structured investing from momentum chasing.

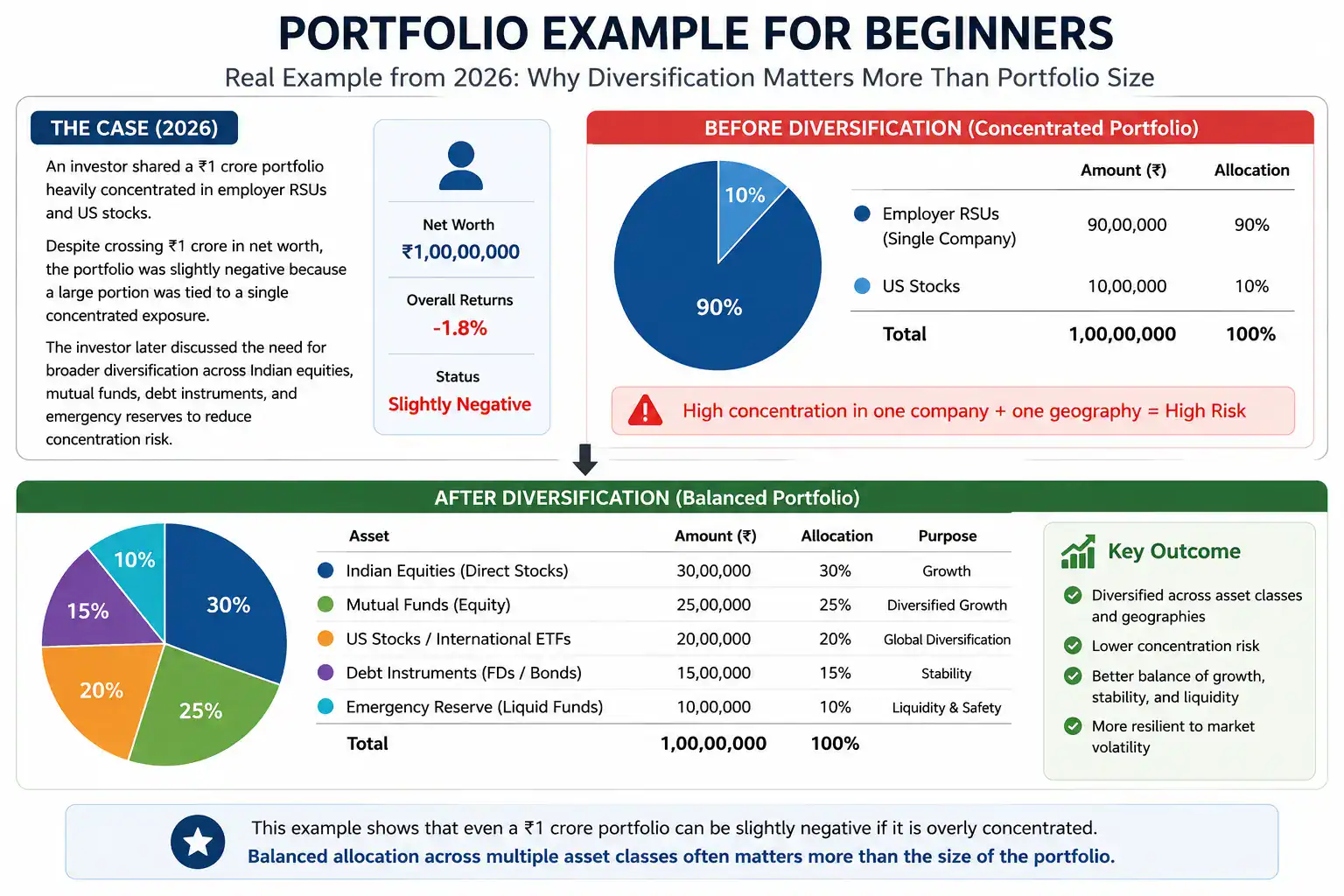

Portfolio Example for Beginners

A real-world portfolio diversification discussion gained attention in Indian investing communities during 2026 when an investor publicly shared a ₹1 crore portfolio heavily concentrated in employer RSUs and US stocks. Despite crossing ₹1 crore in net worth, the portfolio remained slightly negative because a large portion was tied to a single concentrated exposure. The investor later discussed the need for broader diversification across Indian equities, mutual funds, debt instruments, and emergency reserves to reduce concentration risk.

This became a practical example of why portfolio management matters beyond absolute portfolio size. Even large portfolios can struggle when allocation remains overly dependent on one stock, sector, or geography. The case also shows how balanced allocation across multiple asset classes often matters more than simply increasing investment amounts.

Importance of Portfolio Management in Trading & Investing

Effective portfolio management does more than keep your investments organised, as the following points illustrate.

- Preventing lifecycle mismatch: Several investors build a portfolio once and forget it. A 25-year-old and a 50-year-old with identical allocations are not both invested correctly. One is carrying far more risk than their life stage justifies, and periodic management is the only thing that catches this drift before it becomes costly.

- Quantifying underperformance: One bad quarter is noise. Five consecutive quarters of lagging the sector benchmark is a structural problem. Active management gives you the data to tell the difference, so decisions are based on evidence rather than the hope that things will eventually turn around.

- Catching silent concentration: A stock that triples quietly becomes 40% of your portfolio without a single deliberate decision. Without periodic review, you are carrying equity concentration risk you never consciously chose to take.

- Improving tax efficiency: Selling before completing 12 months triggers short-term capital gains tax at 20%. Investors without a portfolio management discipline churn holdings without accounting for this, silently reducing net returns across multiple financial years.

Common Portfolio Mistakes to Avoid

Most of these mistakes do not look like mistakes when you are making them, which is what makes them dangerous, such as the following.

- Overdependence on a single stock or sector: Depending heavily on one company or industry can increase losses during sharp declines. A major example was Yes Bank, where many retail investors held concentrated positions before the 2020 crash. According to Business Standard, retail investors collectively lost more than ₹3,300 crore after the stock collapsed.

- Investing based on market buzz: Social media-driven investing can result in buying stocks without understanding company fundamentals. During the GameStop meme stock rally, many investors entered after rapid price increases. Reports later estimated investor losses crossed $13 billion after the rally weakened and prices corrected sharply.

- Lack of proper diversification: Portfolios focused only on one sector may face larger losses during sector-specific downturns. During periods of banking and financial sector stress, investors with diversified holdings generally faced lower overall portfolio impact compared to sector-heavy portfolios.

- Emotional reactions during market volatility: Panic selling during market declines is a common investing mistake. During the 2020 market crash, many investors exited equity investments after steep declines, but markets later recovered strongly across major indices.

- Neglecting costs and tax impact: Frequent trading can increase brokerage charges, taxes, and transaction costs. Even profitable trades may generate lower final returns after accounting for repeated expenses and tax liabilities.

- Using sectoral funds as core holdings: Sectoral funds are designed to complement a portfolio during a specific cycle, not anchor it. Investors who placed the majority of their equity allocation into infrastructure or defence theme funds during peak inflows found themselves with concentrated, illiquid exposure when sentiment reversed.

- Ignoring expense ratio compounding: A 1% annual difference between a regular and direct plan of ₹10 lakh over 20 years at 12% returns compounds into a difference of several lakhs. Most investors never calculate this and spend decades paying distributor commissions on funds they could access cheaper directly.

- Selling winners, keeping losers: Research consistently shows retail investors exit profitable positions early and hold loss-making ones hoping for recovery. This pattern, known as the disposition effect, systematically removes compounders from portfolios while accumulating dead weight.

How StockGro Helps You Build & Test Your Portfolio

Building a portfolio requires more than understanding asset allocation in theory. StockGro allows users to apply investment ideas through platform currency, stock-tracking tools and market research without placing trades using their own money.

Practise portfolio construction: Users can use platform currency to buy or sell stocks and create a Stocks Tracker. This helps them understand how selecting companies from different sectors can affect the value and concentration of a portfolio.

Test long-term investment strategies: The Default Stocks Tracker can be used to build and review long-term stock strategies. Users can monitor their holdings, cash balance, invested amount and overall profit or loss as market prices change.

Use the Strategy Builder: Users can add stocks through the Strategy Builder and examine how different selections perform together. StockGro also displays an indicative transaction fee of 0.01% of the traded value, helping users understand how trading costs can affect returns.

Learn through research and community insights: StockGro combines investment research, market tools and interaction with other users. Insights from SEBI-registered research analysts can help users develop a more structured approach to evaluating stocks instead of relying only on unverified market tips.

These features can help beginners understand portfolio allocation, concentration and transaction costs before applying similar decisions to their actual investments.

Final Thoughts

Building wealth in the share market is rarely about finding the perfect stock. Understanding what is a portfolio in the share market, and structuring one with intention, is where the real edge lies. Thoughtful allocation can temper losses during downturns while allowing returns to accumulate when conditions improve. Begin with a measured approach, review the holdings at suitable intervals and let disciplined compounding strengthen financial progress over the long term.

FAQs

A portfolio is a collection of investments you own, such as stocks, mutual funds, or bonds, held together to grow your wealth while managing risk across different assets and sectors.

Most experts suggest 10 to 15 stocks across different sectors as a starting point. This provides meaningful diversification without making the portfolio too complex to monitor and manage effectively.

Yes. Mutual fund SIPs can be started with as little as ₹500 per month.

Once or twice a year is sufficient for most investors. Rebalancing more frequently increases transaction costs and tax events without meaningfully improving outcomes for long-term portfolios.

Diversification reduces unsystematic risk, but over-diversification can dilute returns and make a portfolio difficult to manage. The goal is meaningful diversification across sectors and asset classes, not simply owning as many assets as possible.

A trading portfolio is built for short-term gains through frequent buying and selling based on price movements. An investment portfolio is designed for long-term wealth creation through asset appreciation and compounding. The time period, risk profile, and strategy involved are fundamentally different between the two.