What Is a Long Put Option Strategy?

Buying a put option is the foremost part of this option trading strategy. The buyer pays a premium up front, and in return, avails the right to sell an asset at a decided price, called the strike price, before the contract expires.

The trade makes a profit when the respective asset falls below the strike price. If the asset stays flat or rises, the option expires worthless. The buyer walks away having lost only the premium, which is both the cost of the trade and its maximum possible loss.

Key Components of a Long Put Option

Before placing a long put trade, four elements must be clearly understood. Each one directly shapes the trade’s cost, risk, and potential return.

| Component | What It Means |

| Strike Price | The price at which you can sell the asset. This sets your break-even. |

| Premium | What you pay to buy the option. Your total downside is capped here. |

| Expiry Date | The deadline of the contract. After this, the option has no value if it hasn’t moved in your favour. |

| Underlying Asset | The stock or index the option is written on -for example, Reliance Industries or Nifty 50. |

How Long Put Options Work

When a trader buys a put option, they pay the premium upfront. This option entitles the holder to sell the underlying asset at the strike price, at any point within the contract’s validity period. In the event the asset price falls beneath the agreed strike price before contract expiry, the put option gains intrinsic value. The holder then has two choices- sell the option itself in the market at its appreciated value, or exercise it directly against the underlying asset.

If the asset doesn’t fall, or doesn’t fall enough, the option expires worthless, and you lose what you paid.

One factor that works constantly against the buyer is time decay, known in options as theta. Every passing day reduces the option’s time value. So even if the stock stays flat, your put is quietly losing value. This is why being right about direction but wrong about timing still results in a loss.

Example of a Long Put Option

Say Company X is trading at ₹500. A trader expects a fall and buys a put at a strike price of ₹480, with 30 days to expiry, paying a premium of ₹15 per share. Lot size is of 100 shares. Total outlay: ₹1,500.

Break-even = ₹480 – ₹15 = ₹465

| What Happens | Price at Expiry | Intrinsic Value | P&L per Share | Total P&L |

| Sharp fall | ₹440 | ₹40 | +₹25 | +₹2,500 |

| Modest fall | ₹470 | ₹10 | -₹5 | -₹500 |

| No fall | ₹490 | Nil | -₹15 | -₹1,500 |

The trade only starts making money once the stock crosses below ₹465. Above that, the premium is either fully or partially lost.

Implementing the Long Put Option Strategy

In options trading putting on a long put involves more than just picking a direction. Each decision compounds on the next, and a poor choice on any one of them can turn a correct directional call into a losing trade.

- Pick the right underlying: A long put needs a specific reason to exist, not just a general feeling that the market might fall. Weak earnings visibility, a sector in structural decline, or a technical breakdown at a key level all serve as better grounds.

- Decide on the strike: Far out-of-the-money strikes are cheap but need a larger move to generate profit. At-the-money strikes cost more but break even with a smaller price decline. The right strike depends on your expected magnitude of the move.

- Choose expiry carefully: A longer-dated option gives more time but costs more in premium. A shorter expiry is cheaper but punishing if the move is delayed even slightly.

- Know when to exit: If the stock has already made its expected move, close the position. Many buyers hold their position too long, waiting for bigger gains, while time decay quietly erodes the value they have already built.

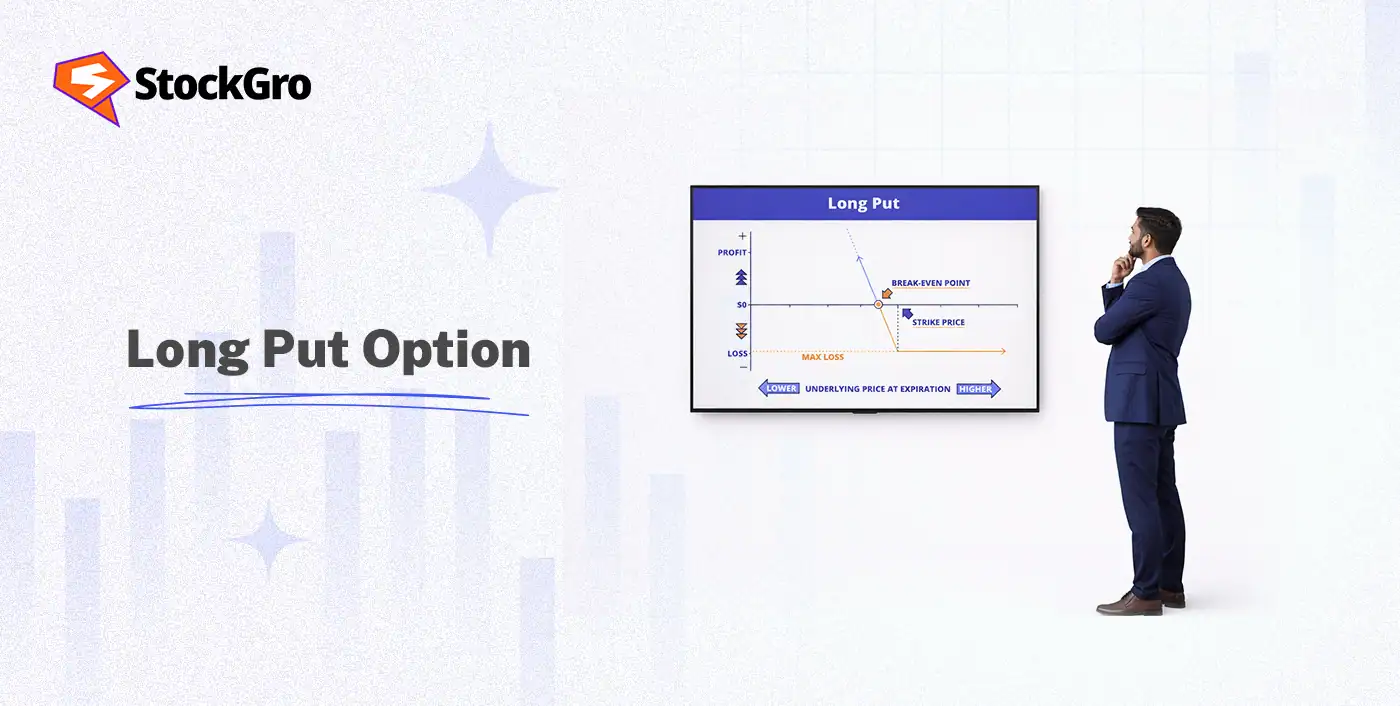

Profit and Loss Potential of a Long Put

The reward-to-risk structure of a long put is one-sided in a useful way as your loss is capped from the start.

| P&L Metric | Detail |

| Maximum loss | The premium paid- fixed from day one |

| Maximum profit | Strike price less premium (If underlying asset’s price drops to zero) |

| Break-even | Strike price less premium paid. |

| Time decay | Erodes value daily when the option is out of the money |

Advantages of the Long Put Option Strategy

There are specific structural benefits here that set the long put apart from most other bearish approaches.

- Loss is fixed: The moment you buy the put, your worst-case outcome is already defined. That changes how you manage the trade psychologically.

- Leverage without margin calls: A small premium gives you exposure to a much larger notional position. And unlike selling options, there is no broker margin requirement to maintain.

- Works as portfolio insurance: Investors sitting on equity positions can buy puts on the index or individual stocks to limit downside during uncertain periods. This use case, often called a protective put, is entirely separate from speculation.

- No uptick rule or borrowing constraints: Unlike short selling, buying puts does not require you to borrow shares. There are no restrictions tied to short-sale regulations.

Risks of the Long Put Option Strategy

The limited loss feature can create a false sense of safety. In practice, several things regularly go wrong even for traders with a correct directional view.

- The full premium disappears: If the stock doesn’t fall past the break-even before expiry, the entire premium is gone. Even a partial fall isn’t enough if it doesn’t cross the strike by more than the premium paid.

- Time works against you every day: The option loses time value continuously. A stock can be moving exactly as expected but simply too slowly, and the position can still end at a loss.

- Volatility drop hurts: Puts are priced partly on implied volatility. Buying when volatility is elevated means you are paying a higher premium. If volatility contracts after you enter, even with the stock moving lower, the option may not gain as much as expected.

- Expiry is a hard deadline: Short selling has no expiry. A long put does. If your thesis plays out six weeks after expiry, you have still lost your premium.

Long Put vs. Short Selling

Both, long put and short-selling, approaches benefit from a falling price, but they are built differently in terms of risk, capital, and time.

In short selling, a trader borrows shares and offloads them immediately, expecting to repurchase at a lower price. But if the stock climbs instead, losses keep mounting with no upper limit, for as long as the position stays open.

| Factor | Long Put | Short Selling |

| Maximum loss | Premium paid that is fixed | Unlimited if stock keeps rising |

| Capital needed | Premium only | Broker margin on borrowed shares |

| Works from a fall | Yes | Yes |

| Expiry constraint | Yes — fixed deadline | None — open-ended |

| Regulatory limits | Minimal | Can be restricted during volatility |

When the goal is limiting risk while staying exposed to downside, the long put is structurally sounder. Short selling is more appropriate when timing is uncertain and active daily management is part of the plan.

Conclusion

The long put is a straightforward, risk-defined strategy for traders who expect an asset to fall. The premium paid defines the absolute worst case before the trade is even placed. The upside is meaningful if the expected decline materialises in time.

The recurring pitfalls are time decay, late-moving price action, and entering when implied volatility is already stretched. A long put placed on the right underlying, at a sensible strike and expiry, with a clear exit plan is among the most disciplined ways to express a bearish view in any market.

FAQs

In a long put option, you pay a fee upfront for the right to sell an asset at a fixed price. If the asset falls below that price before the contract ends, you make money. If it doesn’t, your loss is limited to the amount you paid.

The maximum loss in a long put option is only the premium paid. The option expires worthless in the worst case, and no additional loss is possible after that.

A long put is bearish in nature. The position turns profitable when the underlying asset loses value before the contract reaches expiry.

Profit per share equals strike price minus current market price, minus premium paid. If the strike is ₹480, the stock is at ₹440, and the premium was ₹15 then profit per share is ₹25.