Every once in a while, a strategy comes along that makes you question why you were doing things the hard way. The synthetic long call is one of them. Same bullish exposure as owning a stock. Significantly less capital tied up. A cleaner entry in certain market conditions.

The timing is relevant too. According to SEBI data, 91% of retail derivatives traders incurred losses in FY25, with many struggling in premium-heavy option buying strategies. In this blog, we discuss how the synthetic call works from the ground up, walk through a real example, and break down the moments when this structure gives traders a genuine edge over conventional approaches.

What a Synthetic Long Call Means

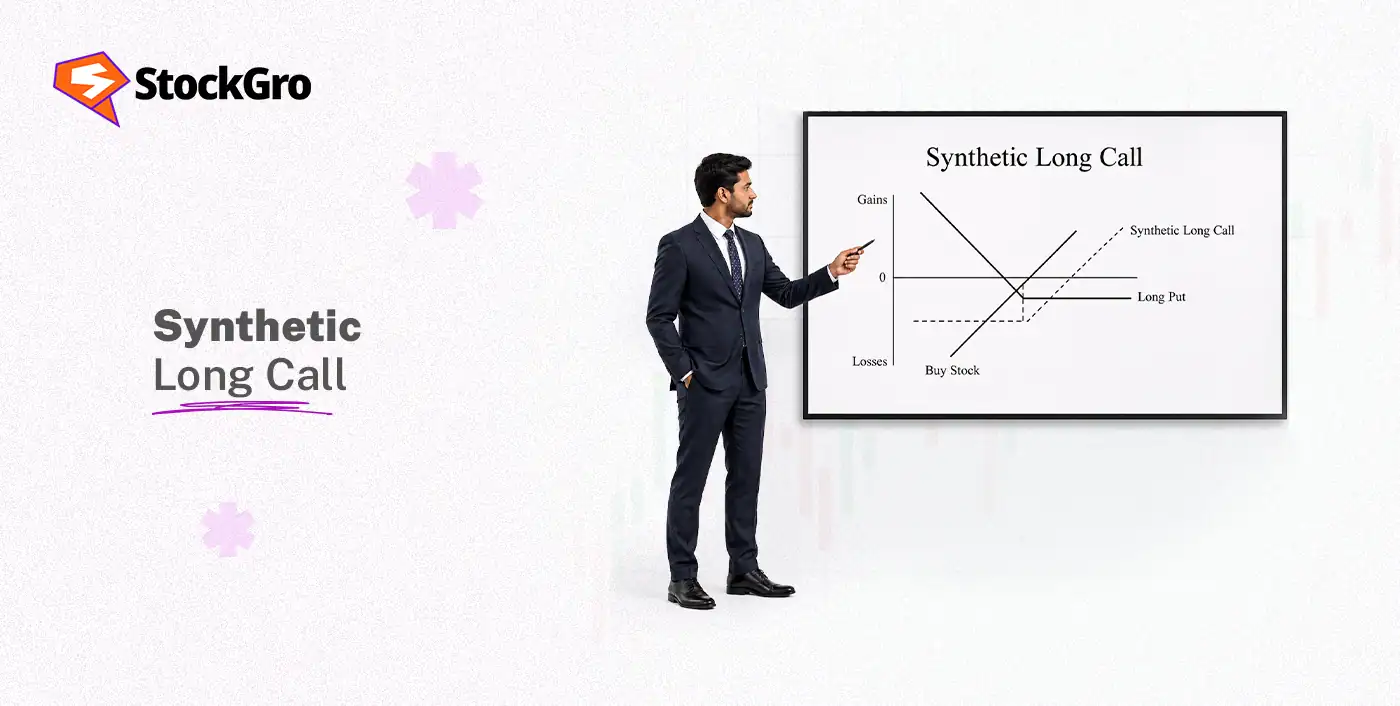

A synthetic long call is an options strategy that combines a long call option and a short put option at the same strike price and expiration date on the same underlying asset. Together, these two positions create a payoff profile that closely mirrors owning the stock outright.

The word ‘synthetic’ is the key here. You are not buying the stock. You are constructing a position using derivatives that behave like you did. When the stock rises, your position gains value similar to how a stock holding would. When the stock falls, your losses are also similar to what a stockholder would experience.

This strategy sits in a broader family of options hedging strategies and synthetic positions that professional traders use to manage exposure, reduce capital requirements, or replicate positions that would otherwise be more expensive or complex to establish directly. Strategies like the synthetic covered call and synthetic long call are often used when traders want to restructure exposure without relying entirely on direct stock ownership.

The synthetic long call is one of the cleaner expressions of a bullish view within that universe.

How the Strategy Is Created

The synthetic long call options has two components: both of which must be in place simultaneously for the strategy to function correctly:

Leg 1 — Long stock position: The investor buys or already holds shares of the underlying stock. This provides full exposure to upside price movement. Every rupee the stock gains above the current price translates directly into profit.

Leg 2 — Long put option: A protective put is acquired on the same underlying asset, carrying the same strike price and expiry as the synthetic call position. The strategy behaves much like a conventional call option, combining restricted downside exposure with theoretically unlimited profit potential on upward price movement.

The protective put works like insurance by offsetting stock-related losses when prices move under the strike level. If the stock rises, the put expires worthless, a cost paid for protection that is no longer needed and the long stock position generates profit freely.

As a result, synthetic calls can serve as an alternative when regular call options are difficult to access or priced too high. Additionally, by changing the protective put’s strike or expiration date, investors can customise the payoff setup in ways that regular call options may not allow.

The choice of strike price determines the level of protection. An at-the-money (ATM) put provides the tightest floor protecting from the current price downward. An out-of-the-money (OTM) put costs less but allows a larger loss before the floor activates.

Payoff Structure Explained

The payoff of a synthetic long call follows the classic hockey-stick shape seen in options trading flat and limited below the strike, then rising without a ceiling above it.

Below the strike price at expiry:

The long stock loses value. However, the put option gains an equal and offsetting amount. The net loss is capped limited to the premium paid for the put, plus any gap between the stock’s entry price and the put’s strike price. This represents the highest possible loss irrespective of the extent of the stock’s fall.

At the strike price:

The put expires worthless. The stock position is at or near its entry cost. The total loss equals the premium paid, the cost of the insurance.

At the strike level, the put expires without value:

The put expires worthless. The long stock position generates unlimited profit. Every point of gain above the strike flows directly to the investor, with no ceiling on the upside.

This setup creates a payoff similar to a call option sharing the same strike price as the purchased put. Any price below the strike results in a fixed maximum loss. Once above the strike price, the payoff curve slopes upward and indicates theoretically uncapped gains.

Breakeven point: Entry price of the stock + put premium paid. The stock must rise above this combined cost for the position to show net profit.

Example of a Synthetic Long Call

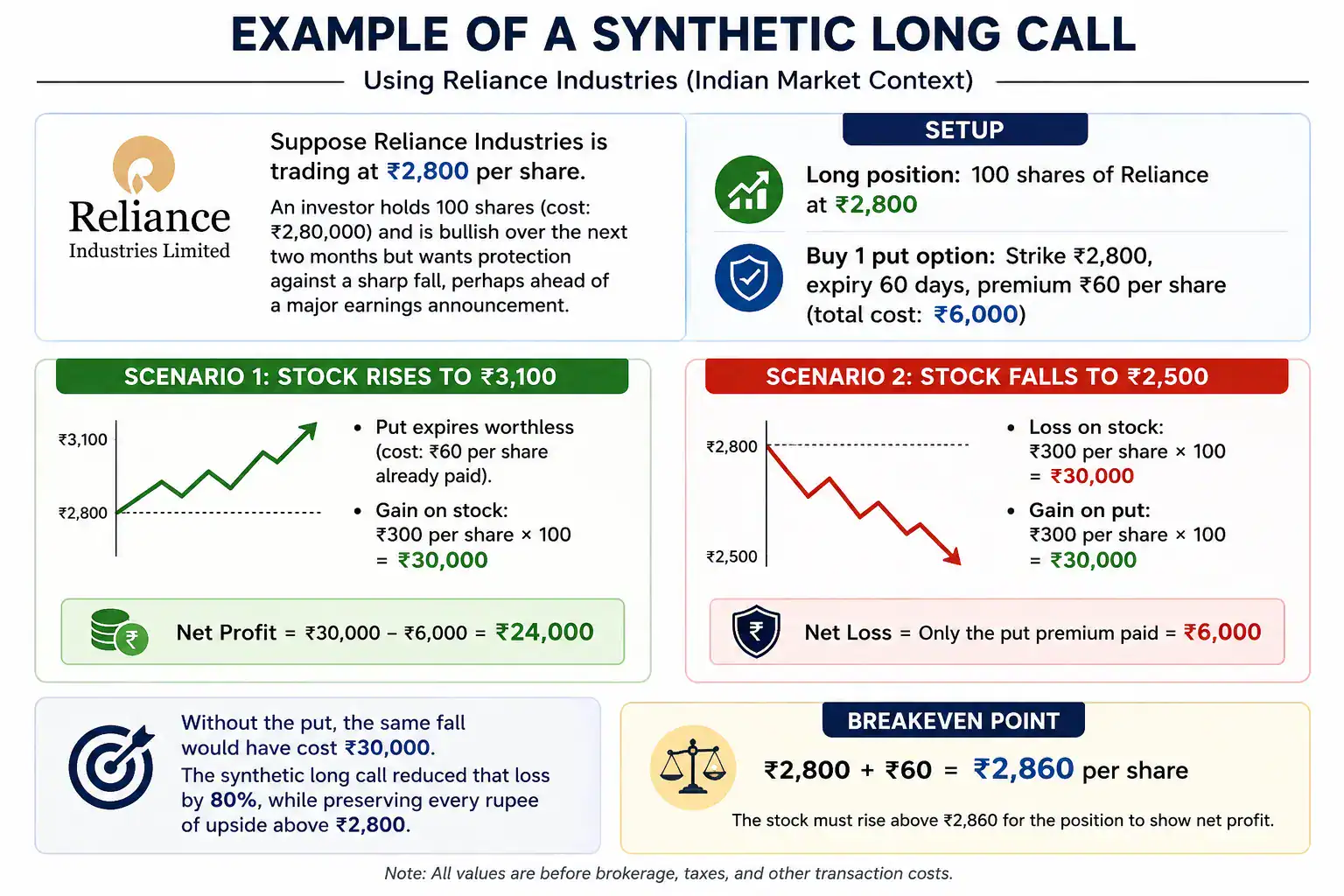

Here is a concrete options trading example using Indian market context:

Suppose Reliance Industries is trading at ₹2,800 per share. An investor holds 100 shares (cost: ₹2,80,000) and is bullish over the next two months but wants protection against a sharp fall perhaps ahead of a major earnings announcement.

Setup:

- Long position: 100 shares of Reliance at ₹2,800

- Buy 1 put option: Strike ₹2,800, expiry 60 days, premium ₹60 per share (total cost: ₹6,000)

Scenario 1: Stock rises to ₹3,100

Put expires worthless (cost: ₹60 per share already paid).

Gain on stock: ₹300 per share × 100 = ₹30,000.

Net profit: ₹30,000 − ₹6,000 = ₹24,000.

Scenario 2: Stock falls to ₹2,500

Loss on stock: ₹300 per share × 100 = ₹30,000.

Gain on put: ₹300 per share × 100 = ₹30,000 (put rises in value as stock falls below ₹2,800 strike).

Net loss: Only the put premium paid = ₹6,000.

Without the put, the same fall would have cost ₹30,000. The synthetic long call reduced that loss by 80%, while preserving every rupee of upside above ₹2,800.

Breakeven: ₹2,800 + ₹60 = ₹2,860 per share.

Why Traders Use This Strategy

Traders turn to the synthetic long call for several practical reasons that go beyond simple cost savings, which include the following.

- Capital efficiency: Rather than blocking full capital to own shares, traders gain equivalent exposure using a fraction of that amount. This frees up capital for other positions running simultaneously, which is particularly valuable for traders managing multiple strategies across a portfolio.

- Hedging existing positions: Traders who are already short a stock or managing a complex portfolio use this as an options hedging strategy to balance directional exposure without unwinding existing positions. The flexibility this offers is especially relevant in volatile markets where restructuring positions quickly matters.

- Cost reduction on bullish views: When implied volatility is high, put premiums are elevated. Selling the put at the same strike actively subsidises the cost of the long call, sometimes bringing the net debit close to zero. This makes expressing a bullish view considerably cheaper than buying a standalone call.

- Index and ETF applications: The strategy is not limited to individual stocks. Its application extends to both ETFs and market indices,making it useful across multiple areas of the market.

Advantages of Synthetic Long Call

The options strategy benefits is accompanied across various segments which include:

- Flexibility to roll positions: In comparison to owning stock, both legs of this strategy can be adjusted. Traders can roll the strike prices or expiration dates forward to adapt to changing market conditions without fully closing and rebuilding from scratch.

- Versatility across instruments: The strategy works on individual stocks, indices, and ETFs, making it applicable across a wide range of market setups and trading styles.

- Unlimited upside potential: The profit potential on the long call leg is theoretically unlimited. As the stock climbs above the strike price, gains accumulate with no ceiling, identical to what a direct shareholder would experience.

- Lower capital requirement: Compared to buying shares outright, the net cost of entry is significantly reduced. The premium collected from the short put offsets part or all of the call premium paid, freeing up capital that would otherwise be locked in a stock purchase.

Risks and Limitations

The main risks and limitations of the synthetic call option strategy are as follows:

- Large losses during sharp declines

Although the protective put limits downside risk, losses can still become substantial if the underlying asset experiences a steep fall before adjustments are made. Synthetic positions often behave similarly to holding the underlying asset itself. This became evident during the March 2020 COVID-19 market crash, when several leveraged bullish derivative positions across global markets suffered heavy drawdowns within days despite hedging structures being in place.

- Time decay impact on protective puts

The put option used for downside protection gradually loses value as expiry approaches. If the underlying asset remains sideways for long periods, the declining premium value can reduce the overall effectiveness of the hedge. During low-volatility phases in index markets, many traders experienced falling hedge values despite limited price movement in the underlying asset.

- Assignment and liquidity risk

Some synthetic structures involving short puts can expose traders to early assignment risk, especially near expiry or during sudden market declines. This may create unexpected stock delivery obligations and additional margin pressure. During high-volatility meme stock phases like the GameStop rally in 2021, many synthetic and leveraged options positions faced liquidity stress, rapid margin changes, and assignment-related complications.

- Complexity in position management

Synthetic call strategies require active monitoring of option expiry, strike selection, hedge effectiveness, and margin requirements. Incorrect adjustments or delayed decisions can impact the intended payoff structure and increase exposure during volatile market conditions.

- Mark-to-market pressure in futures-based setups:

When synthetic calls are created using futures contracts instead of stocks, traders face daily mark-to-market (MTM) settlements. Even if the hedge exists, temporary price declines can create cash flow pressure and margin calls. For example, the Knight Capital Group trading incident in 2012 highlighted how rapid automated order activity and leveraged positions can create severe liquidity and margin stress within minutes during volatile market conditions.

Synthetic Long Call vs Buying a Call Option

The key differences between a synthetic long call and buying a call option directly are as follows:

| Factor | Synthetic long call | Long call option |

| Meaning | Buying stock and a protective put to replicate a call option payoff | Buying a call option for upside exposure without owning shares |

| Construction | Long stock + long put | Call premium only |

| Capital required | High (full stock value + put premium) | Low (premium only) |

| Maximum loss | Put premium + stock/strike gap | Call premium paid |

| Maximum profit | Unlimited | Unlimited |

| Dividends received | Yes | No |

| Ownership rights | Yes (voting, corporate actions) | No |

| Best used when | Already holding stock; calls are expensive or illiquid | Leveraged upside needed with minimal capital outlay |

Final Takeaway for Traders

Markets do not always offer clean conditions, calls get expensive, liquidity dries up, and event risk arrives without warning. The synthetic long call exists precisely for these moments. Mastering it means having a reliable, structured response ready when standard options routes close. Long-term readiness often marks the difference between strategic trading and purely emotional decision-making.

FAQs

A synthetic long call is used to create call-like upside exposure while also holding the stock. It can help protect downside risk through the put option while retaining ownership benefits.

A synthetic long call is usually not cheaper than buying a call because it requires purchasing the stock along with a put option. However, it may help when call options are expensive.

A synthetic long call carries risk because the stock value can fall significantly. The long put limits downside losses, but the strategy still needs higher capital than regular call buying.

A synthetic long call is generally used by traders or investors who already want stock ownership but also need downside protection through put options during volatile market conditions.

The opposite of a synthetic long call is a synthetic short call. It combines a short stock position with a short put option to create bearish exposure.