What Is Gamma Scalping?

Gamma scalping is an active options trading strategy where traders maintain a delta-neutral position and repeatedly buy or sell the underlying asset to profit from small price swings. Rather than betting on market direction, the strategy profits from volatility itself specifically, from the way an option’s delta shifts as the underlying price moves.

In practice, traders generally create a long gamma setup through ATM options combinations and rebalance the position each time the market makes a sizable move.

Each rebalancing is a small buy-low, sell-high trade on the underlying. Over time, if these hedge profits are large enough to outpace the cost of time decay and transaction charges, the strategy generates a net profit.

Gamma scalping operates as both an options risk management method and a volatility-driven trading approach. It does not require the market to move in a specific direction. It requires the market to move, period.

Understanding Gamma in Options

To understand gamma scalping strategy, you first need to understand what gamma actually measures and why it matters in options trading basics.

Delta reflects how sensitive an option premium is to a small price change in the underlying instrument. If a call option has a delta of 0.50, it gains ₹0.50 for every ₹1 rise in the stock. Gamma tracks the speed at which delta changes as the underlying asset price fluctuates. The hedge is reset by trading the underlying instrument until the position returns close to zero delta.

As the underlying moves, delta shifts rapidly, and this is precisely what gamma scalpers want. A long gamma position means delta accelerates in your favour with every move up or down as long as you rebalance quickly enough to lock in those gains.

The four Greeks that govern gamma scalping outcomes are Gamma (the engine), Delta (what you are constantly neutralising), Theta (the daily cost you are fighting against), and Vega (your sensitivity to changes in implied volatility). Balancing these four forces is the ongoing challenge of dynamic hedging in this strategy.

How Gamma Scalping Works

The mechanics of gamma scalping follow a repeating cycle. You open a delta-neutral position with positive gamma. The underlying moves. Your delta drifts away from zero because of gamma. The hedge is reset by trading the underlying instrument until the position returns close to zero delta. You repeat this every time the price moves enough to warrant a hedge.

The formula that ties it together is straightforward. The P&L from each hedge is approximately:

Scalp Profit = 0.5 × Gamma × (Price Move)²

This means the profit from each rebalancing is proportional to the square of the move. Larger moves generate disproportionately bigger scalp profits. Smaller, frequent moves generate smaller but accumulating gains. In both cases, the trader profits as long as the sum of all scalp profits exceeds the total theta decay and transaction costs over the holding period.

This is also why the strategy is classified as a volatility trading strategy. You are not predicting direction. You are expressing a view that realised volatility will be high enough to make the hedging profitable relative to what you paid for the options.

Example of Gamma Scalping

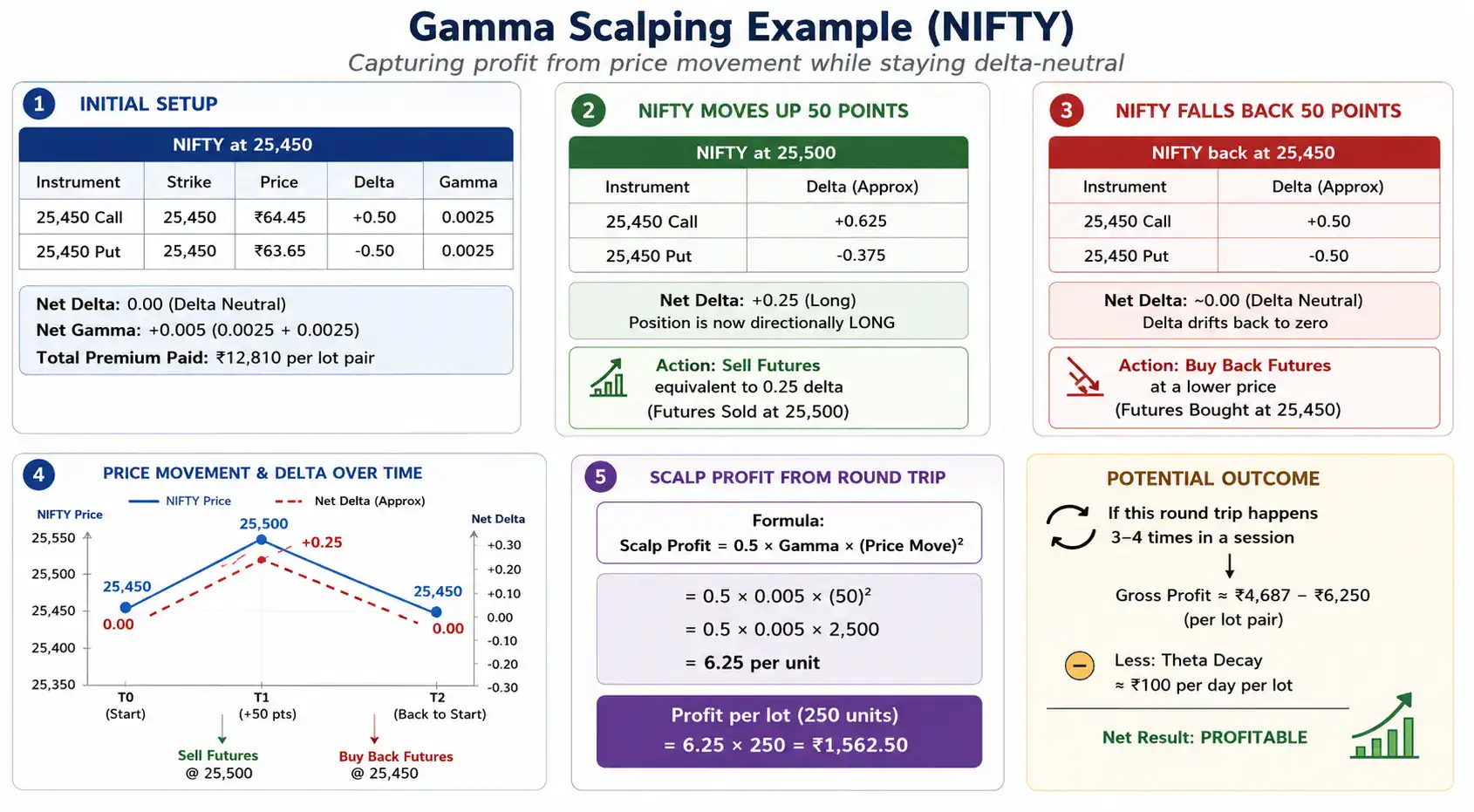

Here is a step-by-step example using NIFTY options to show how gamma scalping works in practice.

Suppose NIFTY is trading at 25,450. You buy one lot each of the 25,450 Call at ₹64.45 (Delta +0.50, Gamma 0.0025) and the 25,450 Put at ₹63.65 (Delta -0.50, Gamma 0.0025). Your net delta is zero and your net gamma is +0.005. Total premium paid: ₹12,810 per lot pair.

Now NIFTY moves up 50 points to 25,500. Because of gamma, the call delta rises to approximately +0.625 and the put delta falls to approximately -0.375. Your net delta is now +0.25. Your position has become directionally long.

To restore delta neutrality, you sell futures equivalent to 0.25 delta, effectively locking in a gain from the upward move.

Now NIFTY falls back to 25,450. Your delta drifts back toward zero as the move reverses. You buy back the futures at a lower price, booking a small

but real profit on the round trip.

That round trip sell futures at 25,500, buy back at 25,450 generates a scalp profit. With a 50-point move and a gamma of 0.005, the approximate scalp profit per lot pair is: 0.5 × 0.005 × 50² = ₹6.25 per unit, or ₹1,562.50 per lot (250 units). If this happens three or four times in a session and theta is ₹100 per day per lot, the net position is profitable.

The strategy’s edge lies entirely in the frequency and magnitude of these oscillations relative to the premium paid and daily decay.

When Traders Use This Strategy

The situations where traders generally use this strategy are as follows:

- Around major economic announcements

This strategy is frequently used during RBI policy decisions, inflation data releases, crude oil inventory reports, or U.S. Federal Reserve announcements because these events often create sharp and fast price movement in equities, commodities, and currencies.

- During the market opening phase

Many intraday traders prefer this strategy in the first 15–30 minutes after the market opens because volatility and institutional activity are highest during this period. A documented ORB trade example from March 5, 2026 showed Nifty 50 breaking above its opening range near 9:45 AM with heavy volume, resulting in a 130-point move before midday.

- In highly liquid instruments

Many traders prefer using this strategy in actively traded instruments such as Nifty 50, Bank Nifty, crude oil, gold, or large-cap stocks because higher liquidity generally allows smoother entries and exits with lower slippage.

- When volume confirms price movement

Traders often wait for unusually high trading volume before entering because breakouts without participation fail more frequently. A Reliance Industries breakout case study showcased how the stock crossed ₹2,600 in 2024 with heavy institutional buying and strong volume after quarterly results and new energy announcements, eventually extending beyond ₹3,000.

Benefits of Gamma Scalping

The main advantages of gamma scalping are as follows:

- Direction-neutral: The strategy does not depend on the market going up or down. Profits come from movement itself, making it useful when traders have a volatility view but no directional conviction.

- Defined entry structure: Starting with a straddle or strangle gives a clear and measurable position from which all subsequent adjustments are made.

- Compounding small gains: In a choppy, volatile market, repeated small scalps can generate meaningful cumulative returns without relying on any single large move.

- Hedging function: For options market makers and institutional desks, gamma scalping is also a risk management tool, it keeps large options books delta-neutral while extracting value from market movement.

Risks and Limitations

The major risks and limitations attached to gamma scalping are as follows:

- Theta decay is constant: The primary danger comes from theta reducing option value faster than scalping activity can recover profits. Near expiration, weekly NIFTY options often experience daily premium erosion ranging from roughly ₹100 to ₹200 per lot. In low-volatility periods, scalping gains simply do not cover this cost.

- Transaction costs compound: Each hedge adjustment carries additional costs such as brokerage, transaction fees, and slippage, which build up over time. Brokerage and execution costs in India can range between ₹20 and ₹50 per lot for each completed hedge cycle, significantly impacting net returns.

- Margin requirements: Hedging with futures requires substantial margin. An unexpected gap or execution error can produce losses far exceeding the original premium paid.

- IV crush: Buying options before a major event locks in high implied volatility. If the event passes without enough actual movement, the IV collapse destroys option value even if the price did move.

Gamma Scalping vs Other Strategies

Understanding how gamma scalping compares to related approaches helps clarify where it fits within the broader options trading basics landscape.

| Strategy | Main objective | How profit is generated | Market condition best suited | Main risk | Typical trader type |

| Gamma scalping | Capture gains from continuous price swings while remaining largely direction-neutral | Frequent delta hedging combined with realised volatility exceeding implied volatility | Highly volatile and fast-moving markets | Theta decay, transaction costs, execution risk | Advanced options traders and market makers |

| Long straddle | The strategy profits from substantial price movement regardless of direction | Option premiums rise sharply after a strong breakout or breakdown | Event-driven volatility like earnings or RBI policy days | Premium loss if movement stays limited | Options traders expecting sharp movement |

| Directional option buying | Profit from a bullish or bearish price move | Call or put option value rises with the underlying price movement | Strong trending markets | Time decay and incorrect directional view | Retail traders and momentum traders |

| Iron condor | Earn from stable prices and low volatility | Collecting option premiums that decay over time | Range-bound or sideways markets | Large losses during sudden breakouts | Income-focused options traders |

| Covered call | Generate additional income on stock holdings | Regular premium collection from selling call options | Stable or mildly bullish markets | Upside gains become limited | Long-term investors |

| Delta heding | Reduce directional exposure in an options portfolio | Balancing option risk rather than aiming for direct profit | Institutional risk management environments | Frequent rebalancing and hedge mismatch | Institutions and professional desks |

Final Takeaway for Traders

Gamma scalping is not a strategy you set and forget. It demands active attention, precise execution, and a clear understanding of how Greeks interact in real time. For traders who invest the time to master it, the real edge lies not in predicting where the market goes, but in being positioned to profit regardless of direction. That shift in thinking from directional to volatility-based is what separates advanced options traders from the rest.

FAQs

Gamma scalping can be profitable when actual market volatility exceeds the implied volatility priced into the options. However, profits depend heavily on execution quality, transaction costs, and managing theta decay effectively.

Gamma scalping is generally better suited for experienced options traders, market makers, and institutional desks comfortable with active hedging, fast execution, and continuous monitoring of volatility, delta exposure, and option Greeks.

Yes, gamma scalping carries meaningful risk. Theta decay, sudden directional moves, slippage, margin requirements, and execution mistakes can quickly outweigh scalping profits, especially during low-volatility or strongly trending market conditions.

Gamma scalping performs best during highly volatile, range-bound, or rapidly fluctuating markets where repeated price swings create multiple profitable hedging opportunities throughout the trading session.

No, delta hedging mainly reduces directional exposure, while gamma scalping actively uses repeated delta hedging adjustments to monetise volatility and capture profits from continuous price movement.