Share buybacks show up in the news regularly, and the coverage almost always frames them as good news. Often they are. But the reasons behind a buyback, and the actual benefits it delivers, vary more than headlines suggest. This article gets into the specifics of what a buyback actually means, why companies reach for it, and where the real advantage lies for the investor on the other side.

What Share Buyback Means

A buyback of shares is when a company decides to buy back its own stock from the people who already hold it. The price on offer is usually higher than where the stock is trading in the market. Once the company gets those shares back, it either cancels them or tucks them away as treasury stock. Either way, there are fewer shares circulating than before.

Indian regulations put a ceiling on buyback sizes. They cannot be more than 25% of a company’s paid-up capital and free reserves. The whole process is governed by the Securities and Exchange Board of India (SEBI) (Buy Back of Securities) Regulations 2018, last revised in November 2024.

There exist different buyback methods through which companies can structure a repurchase. Each one follows a choice of route, pricing, and timing, reflecting a specific objective.

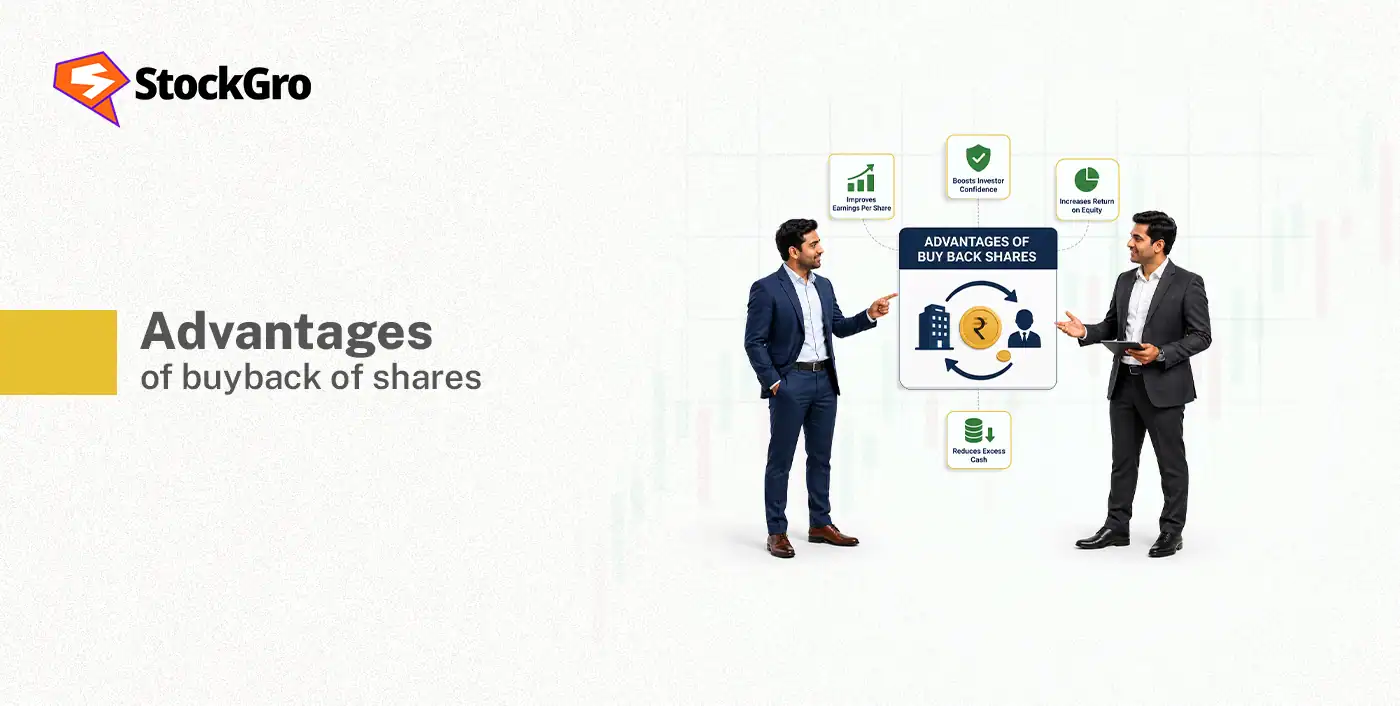

Why Companies Go for Buybacks

There is rarely just one reason behind a buyback announcement. In most cases, it reflects a combination of financial strategy and market signalling.

- Surplus cash with no immediate use

Cash sitting idle on a balance sheet earns very little. When reserves build up beyond what operations or near-term expansion require, a buyback is one of the more efficient ways to redeploy funds without the pressure of making an acquisition just for the sake of action. - Management’s view on valuation

A buyback is management saying that the stock is worth more than what the market currently offers. It is a conviction bet using the company’s own money, and that is harder to dismiss than any press release. - Sharpening the capital structure

A smaller equity base lifts key ratios. Return on equity (ROE) improves because shareholder equity shrinks. Earnings per share (EPS) rise because profits are shared across fewer shares. Neither reflects a change in the actual business, but both make the stock look more attractive to investors screening for value. - Protection against takeovers

When promoter holdings are thin, outside parties can quietly accumulate shares. Buying back stock raises the promoter’s proportional stake without them having to purchase on the open market. It is a quiet but effective defensive move, often used alongside other corporate finance decisions.

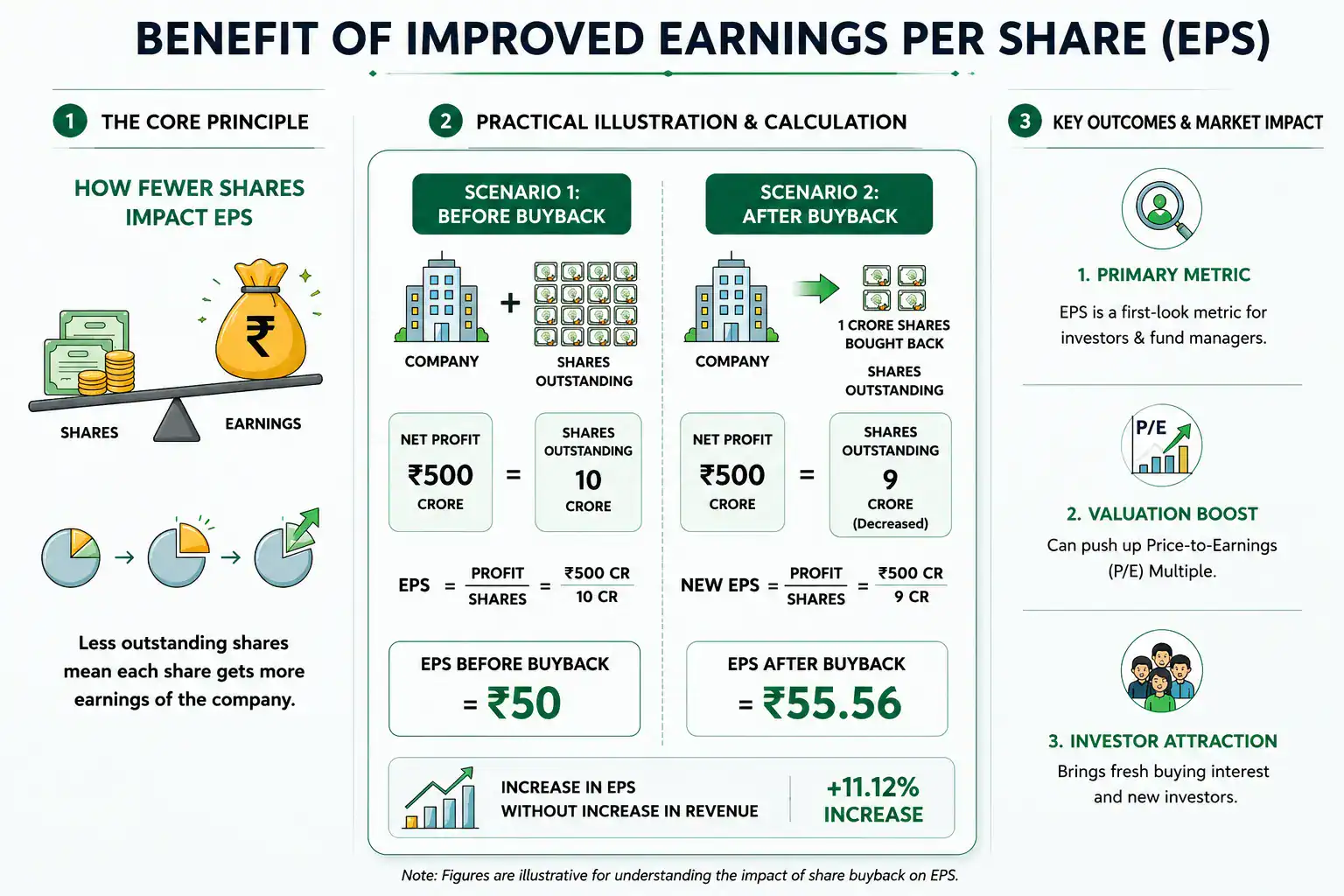

Benefit of Improved Earnings Per Share

Fewer shares in circulation mean each remaining share carries a larger slice of the company’s earnings. The math is straightforward, but the impact is not trivial.

Say a company has earned ₹500 crore. It has 10 crore shares outstanding, and the EPS comes out to ₹50. After buying back 1 crore shares, the profit stays the same, but EPS climbs to ₹55.56, an increase of over 11%, without a single additional rupee of revenue.

That jump matters because EPS is one of the first metrics fund managers and retail investors look at. A rising EPS can push up the price-to-earnings multiple and bring fresh buying interest to the stock.

Positive Signal to Investors

There is a meaningful difference between a company talking about its confidence in the future and actually putting capital behind that belief. A buyback is the latter. When management deploys real money to repurchase shares, it sends a stock market signal that carries weight because if the timing is wrong, the company has spent real money on overpriced stock.

Institutional investors notice this. So do analysts. A buyback at a meaningful premium tends to shift the tone of coverage around a stock, and that effect is often more durable than it first appears.

Benefit of Better Share Value Support

Stock prices do not move in straight lines. During phases when the broader market corrects, or a sector falls out of favour, a buyback gives the stock something most others do not have – a committed buyer who is not going to panic.

That creates a demand floor. While it does not guarantee the price will hold, it dampens volatility and gives long-term shareholders some breathing room. For someone with a three to five-year horizon who has no plan to sell, that kind of support during a rough patch changes the holding experience.

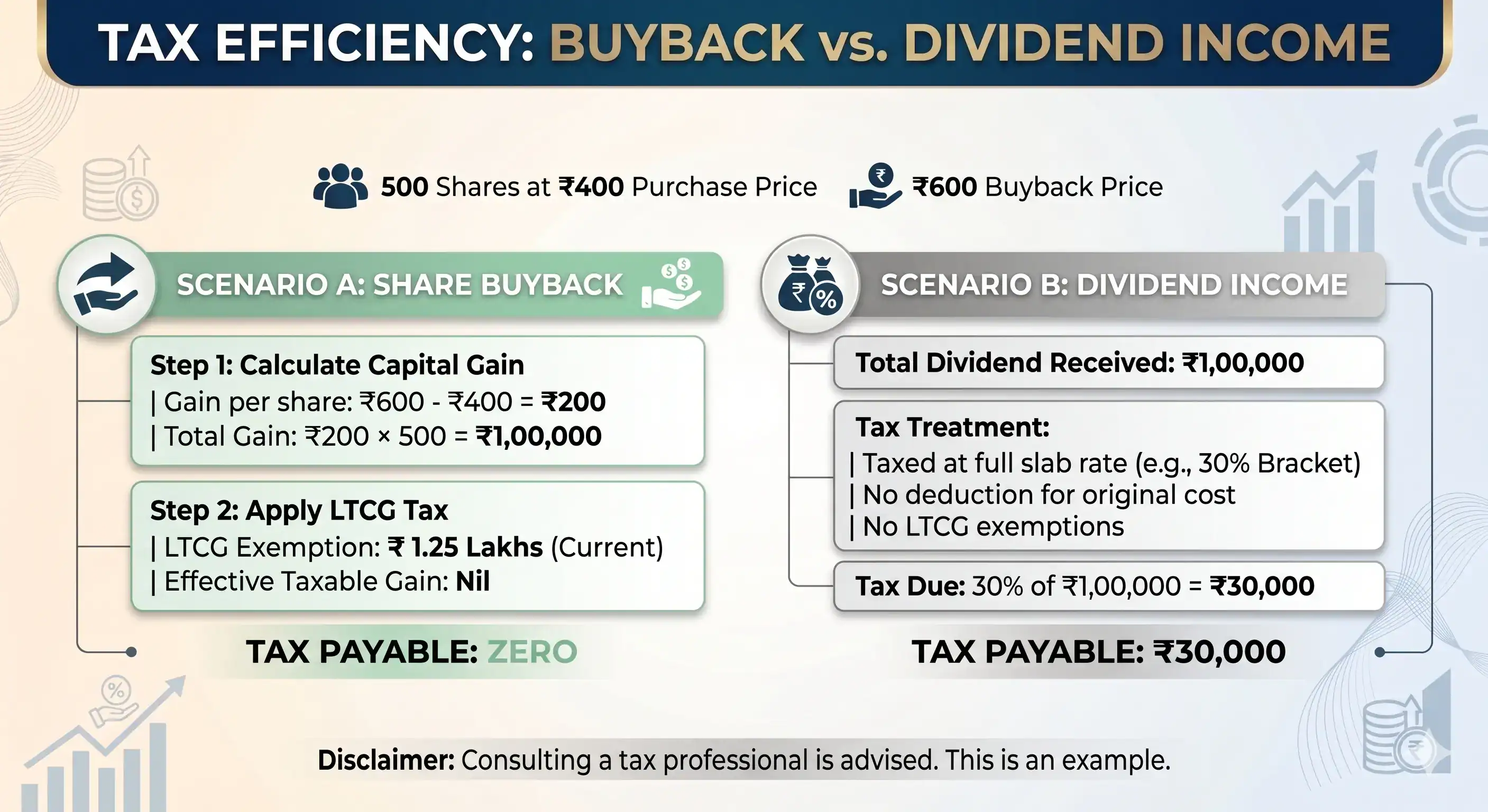

Tax Efficiency Compared to Dividends

Starting from April 1, 2026, the buyback proceeds are now taxed as capital gains in the hands of the shareholder. The tax applies only to the actual gain, not the full amount received.

When shares are held over 12 months, they attract long-term capital gains (LTCG) tax at 12.5%, with an exemption up to ₹1.25 lakh. Shares held under 12 months are taxed as short-term capital gains (STCG) at 20%.

Here is an example: You hold 500 shares bought at ₹400 each, and the buyback price is ₹600. Your gain is ₹200 per share, ₹1,00,000 in total. Since this falls within the ₹1.25 lakh LTCG exemption, your effective tax outgo on a long-term holding is zero.

Now compare that to dividend income, which is taxed at your full slab rate with no exemption and no deduction for what you originally paid. Someone in the 30% bracket receiving the same ₹1,00,000 as a dividend pays ₹30,000 in tax. The gap is hard to ignore.

For most retail investors holding shares over 12 months, the buyback vs dividend tax treatment currently tilts clearly in favour of the buyback route. It rewards patience and puts long-term holders in a more tax-efficient position.

Benefit of Flexibility for Companies

A dividend paid regularly becomes an expectation. Cut it, and the market tends to react poorly. A buyback carries no such obligation. The company executes it once, and there is no promise to repeat it.

That flexibility is valuable. If a better use for cash emerges, the company’s funds are not locked in dividend payments. This makes buybacks a useful concept in investing basics, particularly for companies in sectors where cash generation is uneven rather than steady.

From a shareholder’s perspective, the lack of recurring commitment is a double-edged thing. From the company’s standpoint, it is often the more responsible way to manage capital.

Final Takeaway for Investors

A share buyback is neither a guaranteed windfall nor a reason for alarm. It is a corporate action with specific mechanics and outcomes that vary depending on why it was announced, what price is being offered, and where you stand as an investor. For some, participating makes financial sense. For others, staying invested and benefiting from improved EPS and price support is the better call.

Read the announcement carefully. Understand the premium being offered, check the acceptance ratio, and work out your post-tax position before you decide anything.

FAQs

Companies prefer buybacks to utilise surplus cash, improve EPS and ROE, support share prices, increase promoter holding, and signal management confidence in the company’s long-term valuation.

A buyback can benefit shareholders through higher EPS, possible stock price appreciation, tax-efficient gains, and stronger market confidence, especially when the company repurchases shares at attractive valuations.

A buyback can support or increase stock prices because fewer shares remain in circulation, demand improves temporarily, and investors often interpret the move as a positive management signal.

After a buyback, repurchased shares are either cancelled or held as treasury stock. This reduces outstanding shares, which can improve financial ratios like EPS and ROE.

One is not inherently better than the other. Buybacks may suit long-term investors because gains can be received with favourable capital gains taxation. Dividends provide regular income, but they are taxed according to the investor’s income slab.