What is a Corporate Bond Fund?

A corporate bond fund is a variant of debt mutual fund which channels investor money into fixed-income securities issued by private companies. Regulatory norms mandate that a minimum of 80% of assets are deployed in corporate bonds carrying strong credit quality. Corporations commonly issue such debt securities to improve liquidity and support day-to-day activities..

When a company needs to raise money without issuing new equity shares, it borrows from investors by issuing bonds. Bondholders receive scheduled interest payouts until the repayment date arrives. Corporate bond mutual funds pool money from multiple investors and deploy it into a basket of such bonds, giving individual investors access to the fixed income market in a professionally managed and SEBI-regulated structure.

Debt issued by financially stronger companies is commonly viewed as comparatively safer for investors. External market conditions and changes in issuer finances can still affect the value of these investments.

How Corporate Bond Funds Work

Corporate bond funds collect money from investors and allocate it to a basket of corporate bonds. Returns from these funds are mainly driven by two factors: the regular income earned through interest payments made by the underlying bonds, and changes in bond prices that occur due to shifts in interest rates or the financial condition of issuers. Returns are therefore market-linked and not guaranteed.

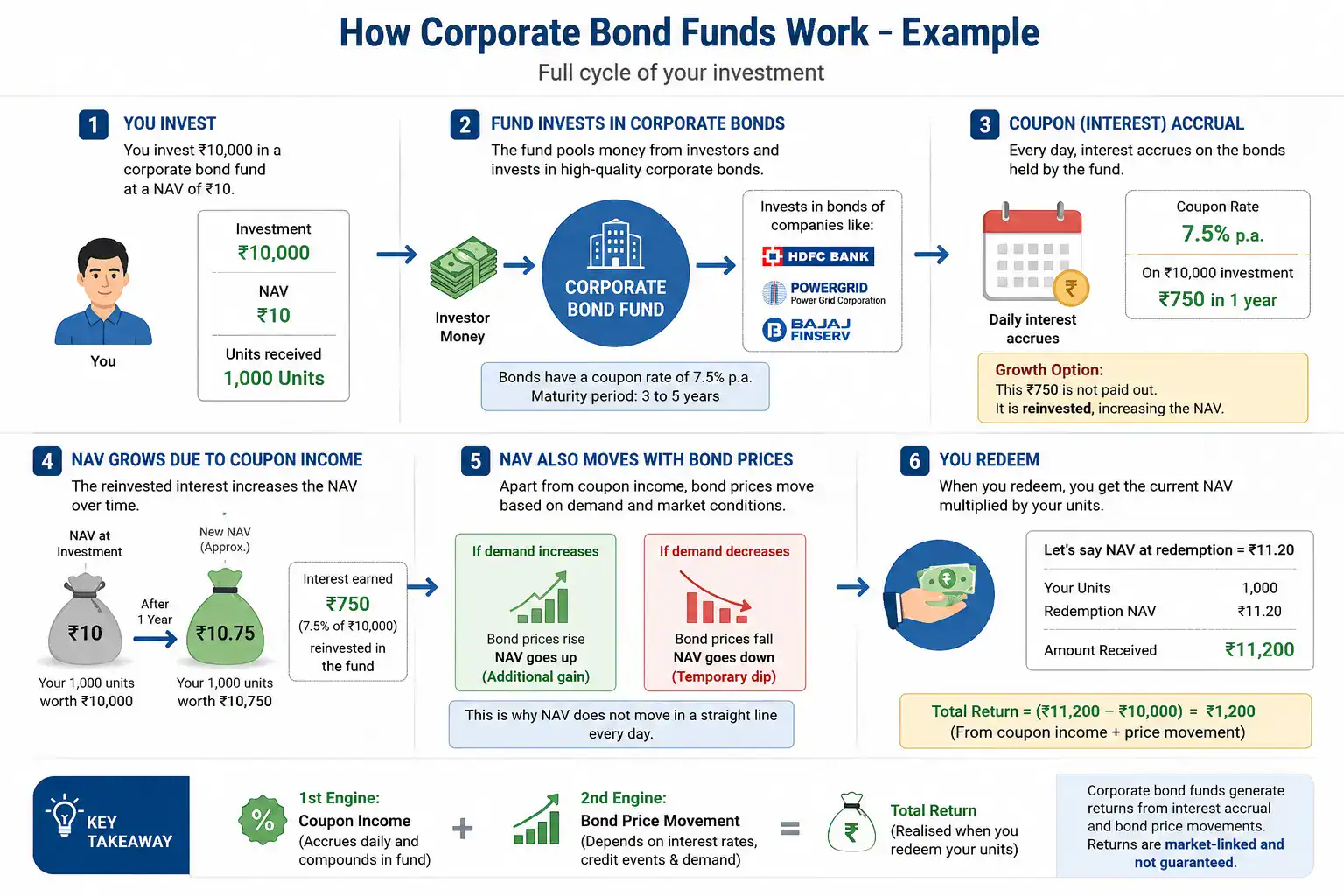

Here is how the full cycle works using a simple example.

You invest ₹10,000 in a corporate bond fund at a NAV of ₹10, receiving 1,000 units. The fund takes your money along with that of other investors and buys bonds issued by companies like HDFC Ltd, Power Grid Corporation, or Bajaj Finance. These bonds carry a fixed coupon rate, say 7.5% per annum, and have a defined maturity period of three to five years.

Every day, the 7.5% annual interest accrues on the bonds held by the fund. This daily accrual is reflected in the fund’s NAV, which rises gradually even when markets are calm. By the end of one year, the fund has earned ₹750 in interest on every ₹10,000 worth of bonds. In the growth option, this ₹750 is not paid out to you. It is reinvested back into the portfolio, which pushes the NAV from ₹10 to approximately ₹10.75. Your 1,000 units are now worth ₹10,750.

This is the first engine of return: coupon income accruing and compounding inside the fund.

The second engine is bond price movement. If demand for the bonds held by the fund increases, their market price rises, pushing the NAV higher beyond just the coupon income. If demand falls, the NAV may dip temporarily. This is why on any given day, the NAV of a corporate bond fund does not move in a straight line even though the coupon is accruing consistently in the background.

The withdrawal amount depends on the latest per-unit valuation of the scheme and your total holdings. The difference between your purchase NAV and redemption NAV, combined with any reinvested coupon income, is your total return.

Types of Corporate Bond Funds

Corporate bond funds in India are not a single uniform product. They vary by maturity profile and credit focus, which are as follows:

- Short duration corporate bond funds: Invest in bonds with shorter maturities, typically one to three years. Interest rate fluctuations usually have a milder effect on this category of debt investments.

- Medium to long duration corporate bond funds: Invest in bonds with longer maturities. These carry higher interest rate risk but can deliver stronger returns in a falling interest rate environment.

- Target maturity corporate bond funds: These are passive funds that invest in bonds with a fixed maturity date, providing better predictability of returns if held to maturity.

- High credit quality funds (AA+ and above): These funds strictly invest in the highest-rated corporate bonds, prioritising capital safety over yield maximisation.

Returns, Risk & Interest Structure Explained

Corporate bond funds generate returns mainly through the interest earned on bonds issued by companies. In general, bonds carrying higher risk often offer higher interest rates, while safer and higher-rated bonds usually provide relatively moderate returns. This creates a direct relationship between risk and return in debt funds.

The average category returns as of 25th May, 2026 are as follows:

| Time period | Average returns |

| 1 Year | 3.15% |

| 3 Years | 6.53% |

| 5 Years | 5.79% |

The relationship between returns and risk can be understood through real market events:

- Securities with stronger credit quality tend to offer reduced yields because repayment concerns are viewed as limited.

- Lower-rated bonds may offer higher coupon rates to attract investors willing to take additional credit risk.

- During the Yes Bank AT1 bond crisis in 2020, several mutual funds holding these higher-yield bonds faced sharp valuation impact after the bonds were downgraded and written down.

- Funds investing in riskier debt instruments sometimes earn higher returns during stable periods, but credit downgrades can affect NAVs sharply.

- Interest rate movements also affect returns. When RBI rates fall, existing higher-interest bonds become more valuable, which may increase bond fund NAVs.

- Multiple routes, including broker apps and AMC portals, are available for investing in these funds.

Corporate Bond Fund vs Other Investment Options

The comparison below discusses how corporate bond funds differ from other common investment choices.

| Investment option | Meaning | Where the money is invested | Risk level | Liquidity | Suitable for |

| Corporate bond funds | Debt mutual funds that mainly invest in high-rated company bonds | Minimum 80% in AA+ and above-rated corporate bonds as per SEBI rules | Low to moderate | High | Investors looking for relatively stable fixed-income exposure over 2–5 years |

| Bank fixed deposits (FDs) | Deposit offered by banks for a fixed tenure and interest rate | Bank deposits | Low | Medium | Investors preferring fixed maturity and predictable income |

| Equity mutual funds | Market-linked mutual funds investing mainly in stocks | Shares of listed companies | Moderate to hugh | High | Long-term wealth creation and market participation |

| Government bonds | Securities borrowed through the Union and state administrations. | Government securities (G-Secs) | Low | Medium | Investors seeking sovereign-backed debt instruments |

| Savings account | Basic bank account for storing and accessing money anytime | Bank deposits | Very low | Very high | Daily transactions and emergency funds |

| Credit risk funds | Debt funds investing significantly in lower-rated corporate bonds | AA and below-rated corporate debt instruments | High | High | Investors comfortable with higher credit-related risk |

| Liquid funds | Short-term debt mutual funds investing in very short maturity instruments | Money market securities for short-term liquidity management. | Low | Very high | Parking surplus money for short durations |

Benefits of Corporate Bond Funds

The prominent benefits of corporate bond funds are as follows:

- SEBI-mandated credit quality floor

Every corporate bond fund must invest at least 80% of its assets in bonds rated AA+ or above as per SEBI’s scheme categorisation rules. This is not discretionary. It is a regulatory requirement, which is what structurally separates corporate bond funds from riskier credit risk funds that chase higher yields with lower-rated paper.

- Liquidity that FDs cannot match

Corporate bond fund units can be redeemed on any business day at the prevailing NAV, with proceeds typically credited within T+2 to T+3 working days. A bank FD broken prematurely attracts a penalty of 0.5% to 1% on the interest rate and you lose the benefit of the locked-in rate entirely.

- Tax efficiency for higher-bracket investors

FD interest is added to your income and taxed at your applicable slab rate every year, regardless of whether you withdraw. Corporate bond fund gains are taxed only when you redeem, giving investors control over when they realise gains and manage their annual tax liability.

- Portfolio stabiliser during equity corrections

Debt exposure often helps reduce overall portfolio swings during stock market declines. During the sharp equity correction of 2022, diversified portfolios containing high-quality bond exposure generally declined less compared to portfolios fully invested in equities. According to Kiplinger data, the S&P 500 fell 18% in 2022 while diversified bond allocation helped reduce overall portfolio volatility.

- Professional management and diversification

Corporate bond funds invest across multiple issuers and sectors instead of relying on a single company bond. This reduces concentration risk compared to directly buying individual corporate bonds.

- Suitable for conservative allocation strategies

These funds are commonly used by investors looking for relatively stable income allocation within a diversified portfolio without taking full equity market exposure.

Risks, Limitations & Common Investor Mistakes

The main risks and limitations are as follows:

- Interest rate increases can reduce NAVs: Rising interest rates reduce existing bond prices. A real example occurred in 2022, when aggressive rate hikes caused broad bond market losses globally. Morningstar reported that one of the world’s largest investment-grade corporate bond ETFs lost nearly 18% during the year because of rising yields.

- High credit ratings do not eliminate risk completely: Even highly rated issuers can face future stress or downgrades. India’s IL&FS crisis became a major example when several debt mutual funds faced pressure after sudden credit deterioration in securities previously considered relatively safe.

- Many investors wrongly compare them directly with FDs: Unlike fixed deposits, corporate bond funds do not provide guaranteed returns or fixed maturity payouts. NAV fluctuations are normal because these are market-linked investments.

- Long-duration exposure can increase fluctuations: Some corporate bond funds hold longer maturity papers to capture higher yields. These funds become more sensitive to interest rate changes and may fluctuate more during tightening cycles.

- Ignoring portfolio quality and duration: Investors often select debt funds only based on recent returns without checking maturity profile or underlying bond quality. Two corporate bond funds can behave very differently depending on duration strategy.

- Redemption pressure can affect debt funds during stress periods: During periods of market panic, large investor withdrawals can create liquidity pressure in debt markets. This became visible during debt market stress events after credit concerns spread across certain Indian NBFC-linked securities.

- Higher yield chasing can create unnecessary risk exposure: Investors sometimes move toward lower-rated debt categories for slightly higher yields without fully understanding credit risk. SEBI’s stricter categorisation rules for corporate bond funds were introduced partly to separate high-credit-quality debt products from riskier credit-focused categories.

How to Invest in Corporate Bond Funds

Multiple routes, including broker apps and AMC portals, are available for investing in these funds. Before investing, check the fund’s portfolio quality, average maturity, expense ratio, and past consistency instead of looking only at returns. The steps to invest in corporate bond funds are as follows:

- Complete KYC using PAN, Aadhaar, and bank details before starting.

- Compare funds based on yield, modified duration, and portfolio holdings rather than only 1-year returns.

- Check whether the fund invests mainly in AAA-rated issuers such as large banks, NBFCs, or established companies.

- Choose SIPs for gradual investing or lump sum investment when interest rates are relatively high.

- Review exit load and taxation rules because frequent withdrawals may reduce overall returns.

- Track interest rate changes since bond fund NAVs can move when RBI policy rates change.

Final Thoughts

Corporate bond funds help diversify portfolios that are otherwise concentrated only in equities or traditional savings products. They offer more return potential than pure liquid or overnight funds, more stability than equity funds, and more liquidity than fixed deposits. They are not risk-free, and minvestors who treat them as guaranteed-return products will be disappointed during interest rate upswings. Used correctly as part of a diversified portfolio, a high-quality corporate bond fund can provide stable income, capital preservation, and a meaningful buffer against equity market volatility.

FAQs

Corporate bond funds are relatively safe compared to equity funds as they invest in high-rated bonds. However, they carry interest rate risk and credit risk and are not as safe as bank deposits, which are covered by DICGC insurance up to ₹5 lakh.

Corporate bond funds suit conservative to moderate investors with an investment horizon of one to three years who want better returns than liquid funds but less volatility than equity. They are particularly useful for investors in higher tax brackets seeking tax-efficient fixed income exposure.

Yes. If interest rates rise sharply or if a bond issuer faces a credit downgrade, the NAV of a corporate bond fund can fall. Short-term losses are possible, though well-managed high-quality funds tend to recover over the medium term.

Corporate bond funds are market-linked investments where returns and NAV change with interest rates and bond prices, while fixed deposits offer fixed, pre-decided interest rates with guaranteed maturity payouts from banks.