Can I Withdraw SIP Anytime?

Yes, your SIP investment can be withdrawn at any time you want. The accumulated units can be redeemed on any day at the prevailing Net Asset Value (NAV), either partially or in full.

While this stands true in most cases, there is one exception. Equity-linked savings scheme (ELSS) funds carry a mandatory 3-year lock-in period. Each ELSS instalment’s holding duration is counted from the day of purchase. If you acquired units in January 2026, you can only redeem them from January 2029 onward.

For all other fund types, equity, debt, and hybrid, you are free to exit at any point. That said, being legally allowed to withdraw is different from it being a financially smart decision. Exit loads, taxes, and the cost of breaking your compounding momentum are all real.

One thing many investors miss: redeeming your units does not automatically cancel your SIP. You need to raise a separate cancellation request for the mandate. If you skip this step, fresh instalments will keep getting deducted even after you have withdrawn the corpus.

Can SIP Be Stopped or Paused Anytime?

Stopping a SIP and pausing a SIP are two completely separate actions, and most investors end up mixing them together.

Stopping a SIP simply means cancelling future instalments. Most fund houses allow this at any time at no cost. You submit a cancellation request through the Asset Management Company (AMC) portal, or your broker app, and the future debits stop. The units already in your folio stay invested until you choose to redeem them.

Pausing is a feature some fund houses offer, letting you temporarily suspend instalments without closing the plan. It is useful during a short financial crunch when you want to keep the SIP alive without straining your cash flow.

The key point to remember is that stopping or pausing a SIP does not trigger any tax or exit load. Only the actual redemption of units does.

Exit Load, Tax Implications & Hidden Charges

This is the section most people skip and end up regretting later.

Exit Load

Exit load is a fee that mutual fund houses charge when you redeem units before a defined period. Since every SIP instalment is treated as a separate purchase, each has its own exit load clock. For instance, if an equity fund charges a 1% exit load on redemptions made within a year, holding its units for more than 12 months will attract no exit load.

Tax on Withdrawal

In SIP redemptions, the holding period is assessed instalment by instalment, not on the total corpus as one block. A redemption can contain both short-term capital gains (STCG) and long-term capital gains (LTCG) components, depending on when each instalment was purchased.

- Equity units held under 12 months fall in the STCG category and are taxed at 20%.

- Equity units held over 12 months qualify for LTCG. They attract a 12.5% tax rate above ₹1.25 lakh.

- For debt funds purchased on or after April 1, 2023, gains are taxed at your applicable income tax slab rate. The holding period does not matter.

What Goes Unnoticed

Securities Transaction Tax (STT) at 0.001% applies on redemption of equity mutual fund units. It is small but real. If you use a SIP calculator to estimate your returns, working with post-tax figures provides a more realistic picture.

Check with SIP Calculator

Step-by-Step: How to Withdraw SIP Investments

Withdrawing your SIP units is fairly straightforward, but each step has a detail worth knowing.

Step 1: Log in to your investment platform

Access the AMC website, your broker app, or MF Central where your SIP is registered. Make sure your KYC is up to date before proceeding.

Step 2: Navigate to your portfolio or folio

Go to the fund you want to redeem from. Check the current number of units you hold and their present NAV.

Step 3: Choose your redemption type

Decide if you want to redeem some of your units or all of them. Partial withdrawals are carried out in a First In, First Out (FIFO) order.

Step 4: Place the redemption request

Enter the amount or unit count you wish to redeem. Most platforms let you choose either. Confirm the request and save the acknowledgement number for tracking.

Step 5: Wait for processing

Equity fund redemptions typically take two to three business days. Debt fund proceeds usually arrive within one to two business days.

Step 6: Receive funds

The amount credited in your bank account reflects the NAV at the time of processing, minus applicable exit load if any.

Step 7: Cancel your SIP mandate separately if needed

If you do not want fresh instalments to continue, raise a SIP cancellation request. This is a step many investors miss entirely.

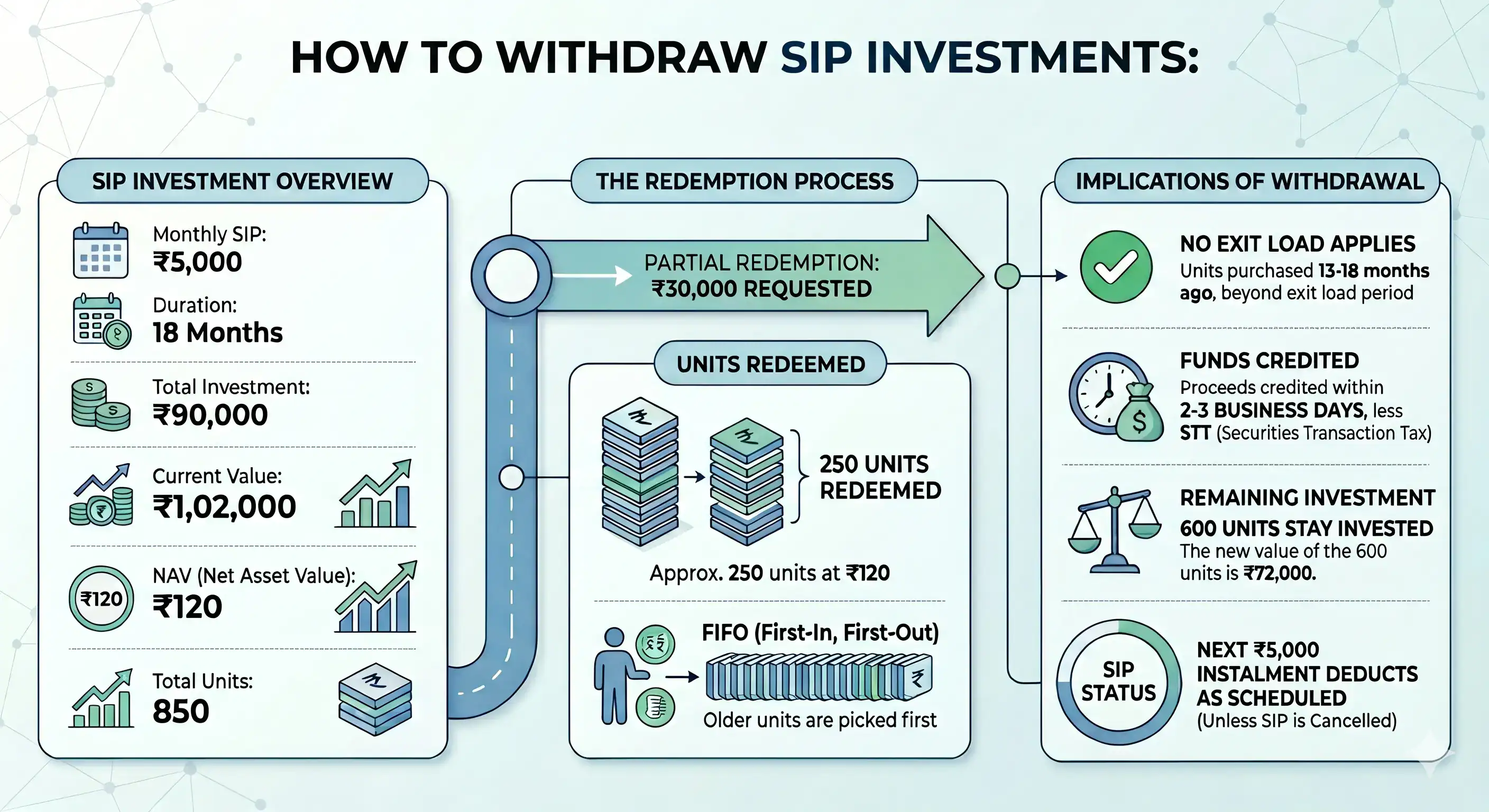

To see how this plays out in practice, here is an example:

Say you have been making a SIP contribution of ₹5,000 a month in a large-cap equity fund for 18 months. Your total investment is ₹90,000. Currently, your investment value is ₹1,02,000, at a NAV of ₹120 across 850 units. You partially redeem ₹30,000.

The platform redeems approximately 250 units at ₹120 using FIFO, starting with the oldest units first. Since those units were purchased 13 to 18 months ago, no exit load applies. Proceeds are credited within two to three business days with only a nominal STT deduction.

The remaining 600 units stay invested. Their value is ₹72,000. If the SIP mandate is not cancelled, the next ₹5,000 instalment will be deducted as scheduled.

Common Mistakes & Risk Management in SIP Withdrawals

Most people make SIP withdrawal decisions in a reactive state, often after a market dip or a sudden expense scare. These are the patterns that tend to cause the most long-term damage.

- Selling during market downturns

Redeeming when markets are down locks in paper losses and eliminates your recovery upside. Short-term markets are volatile. Staying invested through corrections helps in recovery and surpassing earlier portfolio values. - Ignoring the FIFO rule

When you partially redeem, older units go first. If your portfolio has a mix of old and recent units, some newer ones may end up attracting STCG tax at 20%, which can come as an unpleasant surprise during filing. - Not cancelling the SIP after redemption

Redeeming existing units does not stop future instalments. If you forget to cancel the mandate, fresh SIP amounts will keep getting invested even after you have pulled out the corpus. Check your mandate status after every redemption. - Treating all fund categories the same

ELSS funds have a per-instalment lock-in of three years. Submitting a redemption request before that period is completed will simply be rejected by the AMC. Plan your liquidity needs accordingly before starting an ELSS SIP. - Redeeming to switch to another fund

Every redemption is a taxable event. If you want to shift money between funds within the same AMC, explore the Systematic Transfer Plan (STP) route, which can sometimes be more tax-efficient.

Benefits, Outcomes & When You Should Withdraw SIP

SIPs reward patience. The compounding effect that makes them powerful takes time to play out, and breaking that cycle early almost always costs more than it appears on the surface. That said, there are genuine situations where redeeming is the right call.

- Goal achieved

If you set a SIP target, say saving for a home down payment or a child’s education, and you have reached it, redeeming is entirely logical. That is what the SIP was started for. - Consistent underperformance

If a fund has underperformed its benchmark for a long duration without a credible reason to expect improvement, exiting or switching is a reasonable decision. - Financial emergency

If no other option is available, redeeming SIP units is far better than taking a high-interest personal loan. Your mutual fund corpus acts as a financial cushion in times of crisis. - Portfolio rebalancing

Market movements can cause the equity portion of your portfolio to grow out of proportion relative to your risk profile. A partial redemption can help restore the balance.

Final Thoughts

Yes, you can withdraw your SIP anytime for most mutual funds. But whether you should is a different question. Exit loads, capital gains tax, and the cost of broken compounding are all real. If there is no emergency, it is worth asking whether pausing instalments rather than redeeming the corpus gives you the breathing room you need without undoing years of disciplined investing.

FAQs

Yes, most SIPs can be withdrawn anytime, but exit loads and taxes may apply depending on the fund type and holding period.

Most SIPs have no lock-in period, except ELSS funds, where every instalment carries an individual three-year lock-in duration.

Your accumulated units remain invested and continue to grow at market rates. No tax or exit load is triggered by stopping the SIP alone. Only redemption attracts these charges.

Equity mutual fund withdrawals usually take two to three business days, while debt fund redemption proceeds generally arrive within one to two days.

Early withdrawal can reduce returns due to exit loads, taxes, and lost compounding potential, especially during temporary market declines.

Withdrawing during market corrections may lock in losses and reduce recovery potential. Staying invested is often considered a more disciplined long-term approach.