The debate around SIP vs ULIP drive investment decisions across Indian households, especially as investors balance wealth creation with financial protection.

While SIPs are widely associated with disciplined mutual fund investing, ULIPs combine insurance with market-linked returns under a single product. The choice, however, extends far beyond returns alone. The factors such as lock-in periods, charges, liquidity, taxation and long-term financial goals play a decisive role.

Against this backdrop, understanding the difference between SIP and ULIP has become increasingly important for investors aiming to align financial products with specific life goals.

What is an SIP?

A Systematic Investment Plan (SIP) is a method of investing a fixed sum at regular intervals into mutual fund schemes. This means, instead of investing a large sum of money at once, investors contribute smaller amounts monthly, quarterly or at chosen intervals.

In the case of an SIP investment, each instalment is treated as a separate investment, which purchases new units of the mutual fund at the prevailing Net Asset Value (NAV) of the fund.

During market declines, investors receive more units for the same investment amount, while rising markets result in fewer units being allotted. Over the long term, this helps balance the average investment cost through a process called rupee-cost averaging.

The primary advantage of an SIP is flexibility. You can start an SIP with small amounts starting from ₹500, increase contributions gradually and pause or stop investments when required.

You can also estimate long-term returns and monthly contributions using a SIP calculator before starting investments.

However, SIP returns depend on the performance of the chosen mutual fund, and they do not provide fixed or guaranteed returns.

What is a ULIP?

A Unit Linked Insurance Plan (ULIP) is an insurance-cum-investment product that offers life cover alongside market-linked investment opportunities. Under a ULIP, one portion of the premium is allocated towards life insurance, while the remaining amount is invested across market-linked funds such as equity, debt or hybrid funds.

In the case of an ULIP, policyholders receive fund units according to the prevailing Net Asset Value (NAV), much like mutual fund investments. Investors can also switch between equity and debt funds within the ULIP, depending on their financial goals and risk appetite.

One of the defining features of ULIPs is the mandatory five-year lock-in period, designed to promote long-term investing habits. As discussed earlier, ULIPs also provide tax benefits on premiums and maturity proceeds, subject to conditions.

ULIPs also involve various policy-related costs, including premium allocation charges, mortality charges and fund management fees, particularly during the initial years of the policy. Additionally, since the returns are dependent on the market performance, ULIPs do not provide guaranteed returns unless linked to specific guaranteed plans.

SIP vs ULIP: Key Differences Investors Must Know

The table below discusses the key differences between SIPs and ULIPs:

| Feature | Systematic Investment Plan (SIP) | Unit Linked Insurance Plan (ULIP) |

| Product Category | It is a pure investment through mutual funds. | It is a hybrid option that covers term insurance and investment. |

| Life Insurance Cover | There is no life insurance component. | It involves a built-in life cover. |

| Mandatory Lock-in | There is no lock-in period, except in the case of 3 years for tax-saving ELSS. | It has a strict 5-year lock-in period. |

| Allocation of Money | In SIP investments, 100% of your money is invested from Day 1. | In ULIP investments, the premium is split into investment and insurance. |

| Charge & Cost Structure | Mutual funds charge a transparent Total Expense Ratio, at a maximum 2.25% on equity and 2% on debt funds. | The policy includes costs such as premium allocation charges, mortality charges and fund management fees. |

| Tax-Free Fund Switching | Switching mutual funds attract capital gains tax. | A limited number of switches are allowed without charge in a year. |

| Maturity Taxation (Equity) | LTCG taxed at 12.5% on gains exceeding ₹1.25 lakh per year. | The maturity proceeds are fully tax-free under Sec 10(10D), if annual premium < ₹2.50 lakh |

| Partial Withdrawals | You are allowed to withdraw anytime at your convenience (except ELSS). | Here it is strictly prohibited until the 5-year lock-in ends. |

| Regulated By | Securities and Exchange Board of India (SEBI). | Insurance Regulatory and Development Authority (IRDAI). |

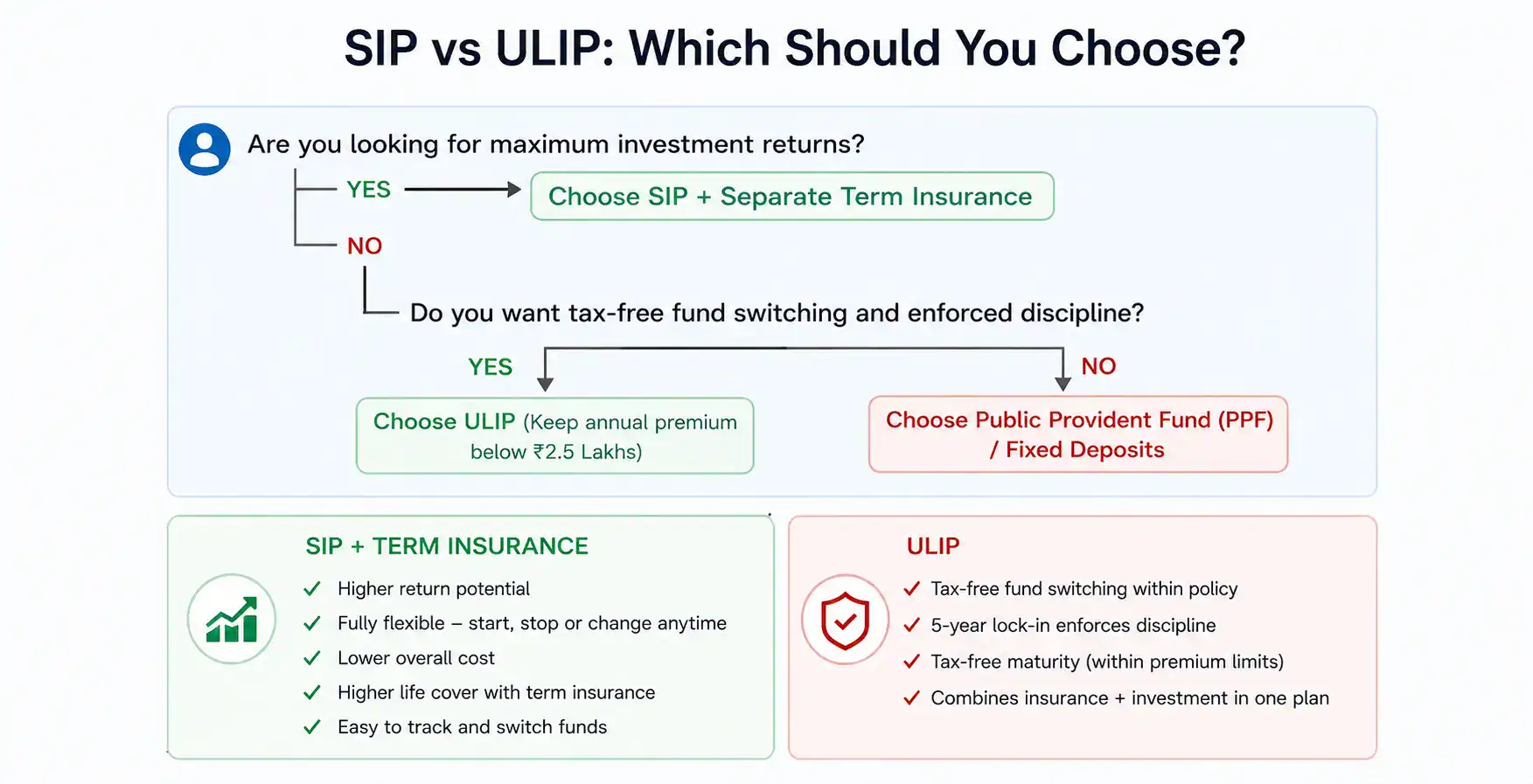

Based on Financial Goals–Which is better: SIP or ULIP?

SIPs are generally preferred for liquidity, flexibility and pure wealth creation, while ULIPs may suit investors looking for insurance-backed, tax-efficient investing over longer investment horizons.

- Long-term goals: ULIPs may suit retirement or child education planning due to their lock-in period, which encourages disciplined investing and long-term corpus building.

- Flexibility and wealth creation: SIPs are generally preferred for investors looking for higher liquidity, lower costs and pure wealth creation potential.

- Insurance protection: ULIPs may be more suitable for investors seeking life insurance cover along with market-linked investments.

- Short-term goals: SIPs are often better for shorter investment horizons since they do not carry a mandatory five-year lock-in like ULIPs.

Why SIP Usually Beats ULIP?

- Better compounding: In the case of an SIP, 100% of your investments are invested from the beginning, while ULIPs deduct several charges first.

- Higher flexibility: SIPs can be paused or stopped anytime, with the flexibility to change installment amounts, whereas ULIPs come with a five-year lock-in.

- Lower insurance cost: An SIP combined with a term insurance usually provides higher cover at a lower cost.

- Easy fund switching: The investors can shift from poorly performing mutual funds more easily than ULIP funds.

When ULIP Might Be Better?

- Tax-efficient switching: You can switch between equity and debt fund changes within ULIPs, without attracting capital gains tax.

- Disciplined investing: The lock-in period helps investors stay invested for longer.

- Tax-free maturity: The maturity proceeds are exempt from tax if the total premium limit is below ₹2.50 lakh, under Section 10 (10D) of the Income Tax Act, 1961.

- Section 80C benefit: ULIP premiums also qualify for ₹1.50 lakh Section 80C tax deduction. However, terminating the policy before five years may reverse the claimed tax benefits.

Common Mistakes, Myths & Investor Misconceptions

Understanding common myths and investor mistakes around SIPs and ULIPs can help investors make better long-term financial decisions and avoid costly planning errors.

- Using ULIPs for short-term goals: The early exits may reduce overall returns due to initial charges.

- Stopping SIPs during market falls: The market corrections can actually help investors buy more units at lower prices.

- Ignoring investment costs: The charges and expense ratios can affect long-term returns significantly.

- Relying only on ULIPs for insurance: ULIP life cover may not always provide adequate financial protection.

- Choosing funds based on high NAVs: A higher NAV does not guarantee better future performance.

Final Thoughts

There is no universal winner in the SIP vs ULIP debate because both products serve different financial purposes.

SIPs are often preferred by investors prioritising liquidity, transparency and long-term wealth creation, while ULIPs may suit those who want insurance coverage alongside disciplined investing.

The right choice depends on investment horizon, insurance needs, tax planning requirements and overall financial goals.

FAQs

SIPs and ULIPs both carry market-linked risks, since returns depend on the performance of underlying funds. However, SIPs are often considered more transparent and flexible, while ULIPs additionally include insurance and policy-related charges.

Some ULIP equity funds may deliver returns comparable to mutual funds over long investment periods. However, charges such as mortality and premium allocation fees can reduce the net returns earned by investors.

Yes, SIPs are considered suitable for beginners because they allow small regular investments, offer flexibility and help investors build disciplined long-term investing habits through rupee-cost averaging.

Yes, ULIPs provide tax benefits on premiums under Section 80C, while maturity proceeds may remain tax-free under Section 10(10D), subject to applicable premium limits and tax conditions.

Yes, investors can stop contributing to a ULIP after the lock-in period and start investing through SIPs. However, surrender charges, taxation and financial goals should be evaluated before making the shift.

The biggest difference is that SIP is purely an investment method for mutual funds, whereas ULIP combines life insurance with market-linked investments under a single financial product.