India’s next phase of economic growth will be powered not only by consumption but also by industrial automation, electrification, and digital manufacturing. As industries modernize, factories become smarter, and infrastructure becomes more energy efficient, companies enabling this transformation stand to benefit significantly.

One such company is ABB India, a leader in industrial automation, robotics, electrification, and motion technologies. Backed by the global expertise of the ABB Group, the company sits at the heart of India’s manufacturing upgrade cycle.

But does ABB India Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | ABB |

| Industry/Sector | Capital Goods |

| CMP | 6058.00 |

| Market Cap (₹ Cr.) | 1,28,374 |

| P/E | 77.05 (Vs Industry P/E of 49.76) |

| 52 W High/Low | 6260.00 / 4637.50 |

| EPS (TTM) | 78.73 |

| Dividend Yield | 0.65% |

About ABB India Ltd.

ABB India Limited is a leading engineering and technology company specializing in electrification, automation, robotics, and motion solutions. It is the Indian subsidiary of the global industrial technology leader ABB Group.

With a strong presence across manufacturing, infrastructure, utilities, and transportation sectors, ABB India provides advanced industrial technologies that help companies improve efficiency, productivity, and sustainability.

The company has a wide installed base across industries such as metals, cement, railways, energy, chemicals, and data centers.

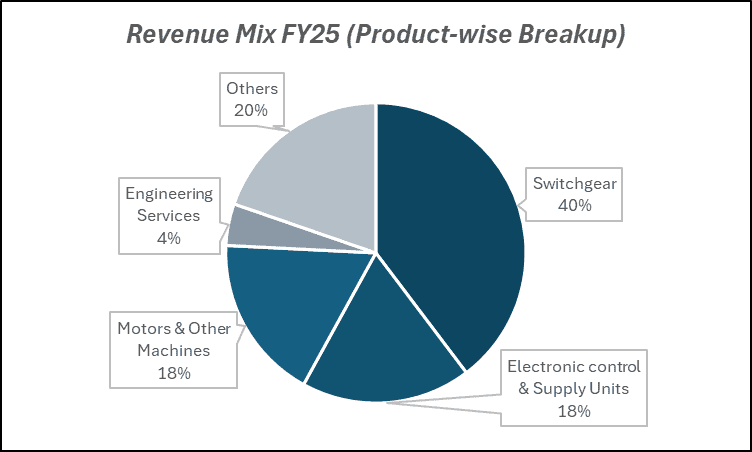

Key business segments

ABB India Ltd. operates primarily in the following key business segments:

- Electrification: Electrical products, switchgear, and power distribution solutions.

- Motion: Motors, drives, and motion control systems for industrial applications.

- Process Automation: Automation solutions for industries such as oil & gas, metals, and utilities.

- Robotics & Discrete Automation: Industrial robots and automation systems for manufacturing.

- Digital & Industrial Software: Industrial IoT and smart factory solutions.

Primary growth factors for ABB India Ltd.

ABB India Ltd. key growth drivers:

- India Capex Cycle Revival: Rising industrial investment across manufacturing and infrastructure.

- Automation & Industry 4.0 Adoption: Increasing demand for robotics, automation, and digital manufacturing.

- Electrification & Energy Efficiency: Growing need for energy-efficient electrical equipment.

- Infrastructure & Railways Modernization: Electrification of railways and infrastructure projects driving demand.

- Data Centers & Renewable Energy Growth: New opportunities in power distribution and automation.

Detailed competition analysis for ABB India Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| ABB India Ltd. | 13202.73 | 2043.00 | 15.47% | 1669.40 | 12.64% | 77.05 |

| Siemens Ltd. | 17607.70 | 2027.90 | 11.52% | 1585.50 | 9.00% | 65.71 |

| Hitachi Energy India Ltd. | 7277.34 | 1037.17 | 14.25% | 841.27 | 11.56% | 137.07 |

| CG Power Ltd. | 11728.96 | 1502.07 | 12.81% | 1109.48 | 9.46% | 101.67 |

| GE Vernova T&D India Ltd. | 5721.77 | 1490.83 | 26.06% | 1067.97 | 18.67% | 92.76 |

Key insights on ABB India Ltd.

- Strong parentage from global technology leader ABB Group.

- Asset-light operations with high return ratios.

- Increasing order inflows from manufacturing and infrastructure sectors.

- Strong positioning in automation and electrification megatrends.

- Margin improvement driven by operating leverage and product mix.

Recent financial performance of ABB India Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 3364.93 | 3310.72 | 3557.01 | 7.44% | 5.71% |

| EBITDA (₹ Cr.) | 657.34 | 500.39 | 546.25 | 9.16% | -16.90% |

| EBITDA Margin (%) | 19.54% | 15.11% | 15.36% | 25 bps | -418 bps |

| PAT (₹ Cr.) | 531.91 | 408.88 | 434.32 | 6.22% | -18.35% |

| PAT Margin (%) | 15.81% | 12.35% | 12.21% | -14 bps | -360 bps |

| Adjusted EPS (₹) | 24.94 | 19.30 | 20.43 | 5.85% | -18.08% |

ABB India Ltd. financial update (Q3 FY26)

Financial performance

- Revenue grew 6% YoY to ₹3,557 Cr in Q3FY26, supported by execution of a healthy order backlog and steady demand across industrial segments.

- EBITDA declined 17% YoY to ₹546 Cr, with margins contracting to 15.4%, impacted by higher material costs, forex volatility, and labour cost adjustments.

- PAT fell 18% YoY to ₹434 Cr, with PAT margin at 12.2%, reflecting cost pressures despite stable revenue growth.

- For the first nine months of the year, revenue reached a record ₹13,203 Cr, reflecting continued demand from infrastructure, manufacturing, and energy sectors.

- Profitability remained under pressure during the period due to commodity inflation, pricing normalization, and higher input costs.

Business highlights

- Order inflows surged 52% YoY to ₹4,096 Cr, marking one of the strongest quarterly order intakes in recent years.

- Order backlog rose 12% YoY to ₹10,471 Cr, providing strong multi-quarter revenue visibility.

- Electrification segment orders grew 43% YoY, driven by smart power solutions and strong demand from data centres and power infrastructure.

- Motion segment orders increased 25% YoY, supported by propulsion systems for railways and strong demand for drives and large motors.

- Demand remained strong across data centres, infrastructure, metals, railways, and energy sectors, reflecting improving industrial capex momentum.

Outlook

- Management expects double-digit revenue growth going forward, supported by a strong order backlog and improving private capex cycle.

- PAT margins are expected to stabilize in the 12–15% range, reflecting normalized profitability levels.

- Strong demand pipeline across data centres, renewables, infrastructure, and automation solutions is expected to support medium-term growth.

- Government capex push and manufacturing initiatives are likely to drive sustained demand for electrification and automation solutions.

- Revenue and profit are expected to grow at mid-teens CAGR over the next two years, supported by order execution and rising industrial automation demand.

Recent Updates on ABB India Ltd.

- Expansion of robotics and automation offerings in India.

- Increased focus on digital industrial solutions.

- Growing participation in infrastructure and railway electrification projects.

- Strategic investments in manufacturing capacity and localization.

- Strengthening partnerships with industrial customers for automation upgrades.

Company valuation insights – ABB India Ltd.

ABB India is currently trading at a TTM P/E of 77.05x, significantly above the industry average of 49.76x, after delivering a 17.4% return over the last one year, outperforming the NIFTY 50’s 8.9% gain. The premium valuation reflects strong investor confidence in the company’s long-term growth prospects, supported by structural demand for electrification, automation, and digitalisation solutions across industries.

The investment case for ABB India is supported by its strong positioning across electrification, motion, and industrial automation, enabling it to benefit from India’s ongoing industrial capex cycle and energy transition. The company continues to witness healthy demand from core sectors such as data centres, infrastructure, railways, metals, and manufacturing, supported by increasing adoption of automation and energy-efficient technologies. Order inflows remain robust with a strong and growing backlog providing multi-quarter revenue visibility. ABB’s diversified product portfolio, technology leadership, and strong presence across high-growth industrial segments position it well to capture opportunities arising from the government’s infrastructure push, rising manufacturing investments, and expanding digitalisation across industries. Additionally, the company’s strong balance sheet, high return ratios, and consistent cash generation provide financial flexibility to support growth while maintaining operational resilience.

From a valuation perspective, applying a 70x multiple to FY27E EPS of ₹108, we derive a 12-month target price of ₹7,560, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹6,420, indicating a 6% upside, supported by strong order inflows, improving industrial capex trends, continued demand from data centres and infrastructure projects, and steady execution of the company’s order backlog.

Major risk factors affecting ABB India Ltd.

- Capex Cycle Dependency: Slowdown in industrial investments may impact order inflows.

- Execution Risk: Delays in project execution can affect revenue recognition.

- Global Economic Cycles: Industrial demand linked to global manufacturing trends.

- Competition: Strong competition from multinational and domestic engineering companies.

- Technology Investment Requirements: Continuous innovation required to stay competitive.

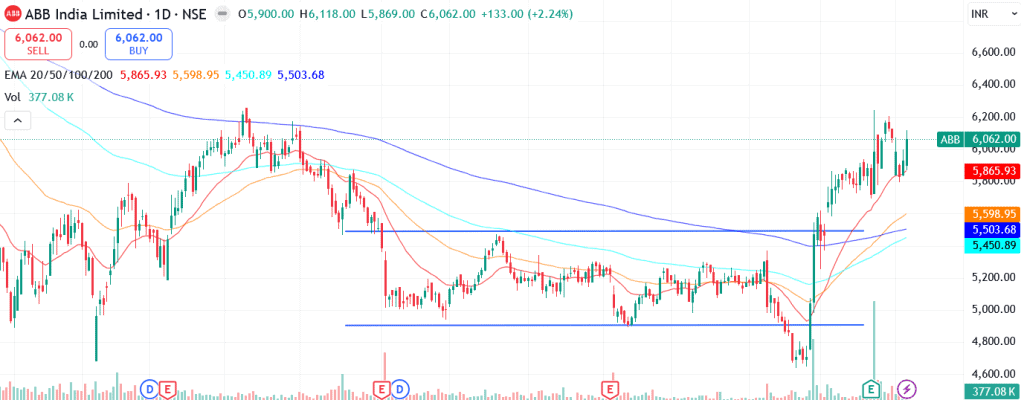

Technical analysis of ABB India Ltd. share

ABB India has broken out strongly from a prolonged sideways channel, signalling a potential resumption of the broader uptrend. The breakout indicates strengthening buying interest and suggests that the consolidation phase has likely concluded, opening the door for a fresh upward move in the stock.

Importantly, the price is trading above its 20-, 50-, 100-, and 200-day EMAs, reflecting strong structural alignment across multiple timeframes. This configuration reinforces the positive trend structure, with these moving averages expected to act as dynamic support zones during any near-term consolidation.

Momentum indicators present a constructive setup. The MACD at 156.48 remains in positive territory, though it is currently slightly below the signal line, indicating that a bullish crossover is awaited. A crossover above the signal line could further strengthen upward momentum and confirm continuation of the breakout move.

The RSI at 60.96 indicates healthy buying interest without entering overbought territory, suggesting room for further upside. Additionally, the 21-day and 55-day Relative RSI readings at 0.11 and 0.22 highlight consistent outperformance versus the broader market, reinforcing the stock’s relative strength.

Meanwhile, the ADX at 32.36 signals a strong trend environment, indicating that the breakout is supported by strengthening trend intensity rather than short-term price volatility.

A decisive move above ₹6,420 could open the path toward ₹7,560 and beyond, aligning with our 12-month fundamental target. On the downside, ₹5,500 remains a key support level; holding above this zone would preserve the breakout structure while limiting downside risk.

- RSI: 60.96 (Bullish; healthy buying interest)

- ADX: 32.36 (Strong trend)

- MACD: 156.48 (Positive; crossover above signal line awaited)

- Resistance: ₹6,420

- Support: ₹5,500

ABB India Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹6,420 (6% upside) and a 12-month target of ₹7,560 (24% upside), based on 70x FY27E EPS of ₹108.

Why buy now?

Strong order momentum and robust backlog, providing multi-quarter revenue visibility and supporting steady execution across key industrial segments.

Beneficiary of India’s industrial capex cycle, with rising investments across infrastructure, railways, metals, manufacturing, and energy sectors driving demand for electrification and automation solutions.

Growing demand from emerging sectors such as data centres and digital infrastructure, supported by increasing adoption of energy-efficient and automation technologies.

Diversified product portfolio across electrification, motion, robotics, and industrial automation, enabling the company to capture opportunities across multiple high-growth industrial segments.

Strong balance sheet, high return ratios, and consistent cash generation, providing financial strength to support growth while maintaining operational resilience.

Portfolio fit

ABB India offers exposure to India’s long-term industrial and infrastructure growth, supported by rising adoption of electrification, automation, and digitalisation across industries. With strong technological capabilities, a diversified industrial presence, and healthy order visibility, the company is well positioned to benefit from the structural capex cycle and increasing demand for energy-efficient industrial solutions. The stock fits well in portfolios seeking exposure to high-quality industrial technology companies with strong balance sheets and long-term growth visibility.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebABB India Ltd.: Budget 2026-27 opportunities

- Manufacturing Push under Make in India: Increased industrial capex boosting automation demand.

- Infrastructure Investment: Higher spending on railways, power, and smart infrastructure.

- Energy Transition & Electrification: Demand for efficient electrical equipment and grid upgrades.

- PLI Schemes for Manufacturing: Production-linked incentives driving factory automation.

- Data Center Infrastructure Expansion: Rising power management and automation requirements.

Final thoughts

ABB India Limited stands at the intersection of India’s industrial modernization, automation adoption, and electrification trends. With strong global technology backing, rising order inflows, and increasing demand for smart manufacturing solutions, the company is well positioned to benefit from India’s long-term capex cycle.

For investors seeking exposure to the structural themes of industrial automation, electrification, and infrastructure growth, ABB India offers a combination of technological leadership, strong execution capabilities, and long-term growth visibility.