India’s premium motorcycle market has evolved from being a niche segment to a lifestyle-driven category fueled by aspirational consumption, rising disposable income, and leisure riding culture. In this transformation, one brand has built a near-iconic status, Royal Enfield.

Backed by the strength of Royal Enfield and its growing premium motorcycle ecosystem, Eicher Motors Ltd. has emerged as one of India’s most recognized automotive brands. Beyond motorcycles, the company also has exposure to commercial vehicles through its joint venture with Volvo.

But does Eicher Motors Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | EICHERMOT |

| Industry/Sector | Automobile |

| CMP | 7315.00 |

| Market Cap (₹ Cr.) | 2,02,883 |

| P/E | 37.44 (Vs Industry P/E of 25.01) |

| 52 W High/Low | 8230.00 / 5219.50 |

| EPS (TTM) | 195.30 |

| Dividend Yield | 0.96% |

About Eicher Motors Ltd.

Eicher Motors Limited is the parent company of Royal Enfield, a leading premium motorcycle manufacturer in India, and also holds a stake in Volvo Eicher Commercial Vehicles (VECV), a joint venture with the Volvo Group.

Royal Enfield dominates the mid-size motorcycle segment in India and has steadily expanded internationally. The company focuses on premium motorcycles, riding accessories, apparel, and lifestyle experiences, creating a strong ecosystem around the brand.

Key business segments

Eicher Motors Ltd. operates primarily in the following key business segments:

- Royal Enfield Motorcycles: Premium motorcycles across domestic and export markets.

- Motorcycle Accessories & Apparel: Riding gear, merchandise, and accessories.

- International Business: Exports and overseas expansion of Royal Enfield.

- Commercial Vehicles (VECV): Trucks, buses, and related services through JV.

- Aftermarket & Services: Service network and customer engagement ecosystem.

Primary growth factors for Eicher Motors Ltd.

Eicher Motors Ltd. key growth drivers:

- Premium Motorcycle Demand Growth: Rising aspirational spending driving premium bike sales.

- International Expansion: Growth opportunities in global motorcycle markets.

- New Product Launches: Expansion into new motorcycle categories and segments.

- Brand-Led Pricing Power: Strong customer loyalty supporting premium positioning.

- Leisure & Touring Culture Growth: Increasing adoption of riding experiences and premium biking.

Detailed competition analysis for Eicher Motors Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Eicher Motors Ltd. | 22568.58 | 5529.09 | 24.50% | 4634.48 | 20.54% | 37.44 |

| Bajaj Auto Ltd. | 62905.00 | 13061.07 | 20.76% | 10013.76 | 15.92% | 32.45 |

| TVS Motor Company Ltd. | 52558.79 | 8126.12 | 15.46% | 3095.63 | 5.89% | 56.09 |

| Hero MotoCorp Ltd. | 47411.24 | 7045.13 | 14.86% | 5391.12 | 11.37% | 17.91 |

| Ather Energy Ltd. | 3671.76 | -408.36 | -11.12% | -517.17 | -14.09% | NA |

Key insights on Eicher Motors Ltd.

- Royal Enfield enjoys dominant market share in mid-size motorcycles.

- Strong brand equity creates pricing power and customer loyalty.

- Asset-light ecosystem through accessories and merchandise.

- International business offers long-term growth optionality.

- VECV provides diversification beyond motorcycles.

Recent financial performance of Eicher Motors Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 4973.12 | 6171.59 | 6114.04 | -0.93% | 22.94% |

| EBITDA (₹ Cr.) | 1201.19 | 1511.90 | 1556.72 | 2.96% | 29.60% |

| EBITDA Margin (%) | 24.15% | 24.50% | 25.46% | 96 bps | 131 bps |

| PAT (₹ Cr.) | 1006.99 | 1234.54 | 1237.67 | 0.25% | 22.91% |

| PAT Margin (%) | 20.25% | 20.00% | 20.24% | 24 bps | -1 bps |

| Adjusted EPS (₹) | 42.70 | 49.93 | 51.79 | 3.73% | 21.29% |

Eicher Motors Ltd. financial update (Q3 FY26)

Financial performance

- Revenue grew 23% YoY to ₹6,114 crore, driven by strong Royal Enfield volume growth of 21% YoY to 3.29 lakh units amid healthy festive demand and premium motorcycle traction.

- EBITDA increased 30% YoY to ₹1,557 crore, with EBITDA margins improving to 25.5%, supported by operating leverage, disciplined pricing actions, and value engineering initiatives.

- Profitability remained robust, with PAT rising 23% YoY to ₹1,238 crore, reflecting sustained topline growth and improving operational efficiencies.

- Gross margins benefited from favorable product mix, earlier pricing actions, and cost optimization measures, partially offsetting higher commodity costs related to precious metals, aluminum, and copper.

- VECV delivered a healthy performance with volumes rising 24% YoY and EBITDA margins improving to 9.5%, adding diversification and a second growth engine to the business.

Business highlights

- Royal Enfield maintained dominant leadership in the mid-weight motorcycle segment with 89% market share in the 250-750cc category, reinforcing its strong premium positioning.

- The 350cc platform continued to be the primary growth driver, benefiting from strong domestic demand and GST rationalization, while recovery in 650cc and gradual traction in 450cc provided incremental support.

- International operations continued to expand, with strong traction in Brazil, Argentina, and Thailand, alongside new store additions and CKD expansion initiatives in key growth markets.

- The company approved a ₹958 crore brownfield capacity expansion to increase Royal Enfield’s annual production capacity from 1.4 million units to 2 million units by FY28.

- VECV continued to benefit from infrastructure spending and domestic manufacturing push, with strong growth across light, medium, and heavy commercial vehicle segments.

Outlook

- Management remains optimistic on sustained double-digit growth for Royal Enfield, supported by strong bookings, healthy inquiries, and continued premium motorcycle demand.

- Premium motorcycle industry growth is expected to remain in high single digits, with Royal Enfield likely to outperform the broader industry driven by strong brand positioning and product pipeline.

- Capacity expansion and improving operating leverage are expected to support margin expansion and long-term earnings growth over the medium term.

- International markets, particularly Latin America and select Asian regions, are expected to emerge as key long-term growth drivers for Royal Enfield.

- Long-term growth outlook remains strong, supported by market leadership in the premium motorcycle segment, strong cash generation, balanced CV exposure through VECV, and sustained product innovation.

Recent Updates on Eicher Motors Ltd.

- Launch of new motorcycle models and variants.

- Expansion into international markets and assembly units.

- Strengthening premium retail and riding ecosystem.

- Continued focus on EV and future mobility exploration.

- Growing contribution from exports and global operations.

Company valuation insights – Eicher Motors Ltd.

Eicher Motors Ltd is currently trading at a TTM P/E of 37.44x, higher than the industry average of 25.01x, with the stock delivering a strong 35.1% return over the last one year, significantly outperforming the NIFTY 50’s -0.1% return during the same period.

The investment case for Eicher Motors is driven by Royal Enfield’s dominant leadership in the premium mid-weight motorcycle segment, where it continues to command an overwhelming market share across the 250cc-750cc category. The company continues to benefit from strong domestic demand, sustained traction in the 350cc platform, recovery in higher-displacement motorcycles, and rising aspirational premiumization trends within the Indian two-wheeler industry. International expansion across key markets such as Latin America, Southeast Asia, and select developed regions is gradually strengthening Royal Enfield’s global presence, while continuous product launches and platform refreshes are supporting customer engagement and market share gains. Additionally, the VECV business provides diversification through exposure to the commercial vehicle segment, benefiting from infrastructure spending, manufacturing growth, and improving freight demand. With strong operating leverage, disciplined pricing strategy, healthy cash generation, and ongoing capacity expansion plans to support future demand, Eicher Motors remains well positioned to deliver sustained earnings growth and long-term value creation.

From a valuation perspective, using the SOTP (Sum-of-the-Parts) methodology for Royal Enfield and VECV businesses, we arrive at a 12-month target price of ₹9,200, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹7,850, indicating a 6% upside, supported by healthy demand momentum, improving operating leverage, strong festive traction, and continued premium motorcycle segment outperformance.

Major risk factors affecting Eicher Motors Ltd.

- Demand Slowdown Risk: Premium motorcycle demand linked to discretionary spending.

- Competition Risk: Increasing competition in the premium bike segment.

- Execution Risk (Global Expansion): Scaling international markets profitably.

- Commodity Cost Volatility: Raw material price fluctuations affecting margins.

- Technology Transition Risk: Shift toward EV mobility in two-wheelers.

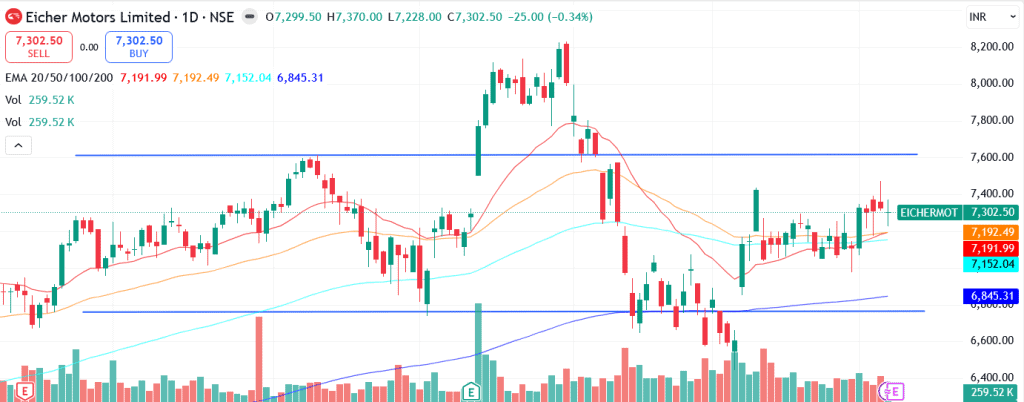

Technical analysis of Eicher Motors Ltd. share

Eicher Motors Ltd has been consolidating within a broad sideways range over the past few months, with the stock currently bouncing back from the lower trendline of the channel, indicating improving momentum and renewed buying interest at lower levels. Despite the consolidation phase, the broader structure remains constructive as the stock continues to trade above all its key moving averages (20, 50, 100, and 200-day EMAs), reflecting underlying strength across short, medium, and long-term timeframes.

Momentum indicators are gradually turning supportive. The MACD at 51.17 remains in positive territory and above the signal line, suggesting a pickup in bullish momentum after the recent consolidation. The RSI at 54.83 indicates healthy buying interest without entering overbought territory, leaving room for further upside if momentum sustains.

The Relative RSI over the 21-day and 55-day periods stands at 0.06 and 0.02 respectively, highlighting steady outperformance versus the broader market and indicating relative resilience within the auto space. Meanwhile, the ADX at 11.29 suggests the stock is currently in a sideways trend with limited directional strength; however, a decisive breakout above the upper trendline of the consolidation channel could lead to a significant improvement in trend strength and trigger fresh momentum buying.

A sustained move above ₹7,850 (key resistance) could result in a breakout from the ongoing consolidation range and potentially open the path towards ₹9,200, aligning with the 12-month fundamental target. On the downside, ₹6,700 remains a crucial support level, below which the current setup may weaken.

- RSI: 54.83 (Good buying interest)

- ADX: 11.29 (Sideways trend; strength may improve on breakout)

- MACD: 51.17 (Positive; above signal line)

- Resistance: ₹7,850

- Support: ₹6,700

Eicher Motors Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹7,850 (6% upside) and a 12-month target of ₹9,200 (24% upside), based on the SOTP valuation methodology for Royal Enfield and VECV businesses.

Why buy now?

Dominant leadership in the premium mid-weight motorcycle segment through Royal Enfield, with a strong brand franchise and commanding market share across the 250cc-750cc category.

Sustained demand momentum in the core 350cc platform, alongside gradual recovery in the 450cc and 650cc segments, supporting healthy volume growth.

Strong operating leverage and disciplined pricing strategy are driving margin expansion and robust profitability despite commodity cost pressures.

International expansion across Latin America, Southeast Asia, and other global markets is strengthening Royal Enfield’s long-term growth runway and global brand presence.

VECV provides an additional growth engine through exposure to the commercial vehicle segment, benefiting from infrastructure spending, manufacturing growth, and improving freight demand.

Portfolio fit

Eicher Motors offers a compelling play on India’s premiumization trend within the two-wheeler industry, backed by Royal Enfield’s aspirational brand positioning and strong customer loyalty. The company combines strong domestic demand drivers with growing international opportunities, while VECV adds diversification through cyclical recovery in the commercial vehicle segment. Its strong balance sheet, healthy cash generation, scalable business model, and ongoing capacity expansion support long-term earnings visibility and operational strength. With leadership in the premium motorcycle category, improving global presence, and sustained profitability, Eicher Motors fits well in portfolios seeking exposure to high-quality consumer discretionary businesses with strong brand equity and long-term structural growth potential.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebEicher Motors Ltd.: Budget 2026-27 opportunities

- Manufacturing & Export Incentives: Support for automotive exports and localization.

- Tourism & Infrastructure Growth: Improved highways supporting leisure riding culture.

- Rural Income Growth: Higher aspirational spending on premium vehicles.

- EV Ecosystem Development: Opportunities in future mobility and electric motorcycles.

- Consumption-Led Growth Policies: Rising disposable income boosting discretionary demand.

Final thoughts

Eicher Motors Limited stands at the intersection of premium consumption, brand-led growth, and evolving mobility trends. With Royal Enfield’s strong market positioning, expanding international presence, and lifestyle-driven ecosystem, the company is well positioned to capture long-term growth opportunities.

For investors seeking exposure to India’s premium automotive and aspirational consumption story, Eicher Motors offers a compelling blend of brand strength, profitability, and scalable growth potential.