India’s pharmaceutical sector sits at the intersection of global healthcare demand, cost-efficient manufacturing, and innovation in specialty therapies. As developed markets look to control healthcare costs and emerging markets expand access to medicines, Indian pharma companies are uniquely positioned to benefit from both trends.

Within this landscape, Glenmark Pharmaceuticals represents a hybrid story, combining a strong generics business with a long-term aspiration to build innovative specialty drugs. With a growing presence in the US generics market, expansion in emerging markets, and a differentiated pipeline in respiratory and dermatology therapies, Glenmark is steadily repositioning itself in the global pharmaceutical value chain.

But does Glenmark Pharmaceuticals Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | GLENMARK |

| Industry/Sector | Healthcare & Pharma |

| CMP | 2126.70 |

| Market Cap (₹ Cr.) | 58,867 |

| P/E | 54.06 (Vs Industry P/E of 32.40) |

| 52 W High/Low | 2284.80 / 1288.55 |

| EPS (TTM) | 37.74 |

| Dividend Yield | 0.12% |

About Glenmark Pharmaceuticals Ltd.

Glenmark Pharmaceuticals Limited is a global pharmaceutical company focused on developing, manufacturing, and marketing branded and generic formulations across multiple therapeutic areas. Founded in 1977 and headquartered in Mumbai, the company has built a strong presence across the United States, Europe, India, and emerging markets.

Glenmark operates across a diversified pharmaceutical portfolio including generics, specialty drugs, and active pharmaceutical ingredients (APIs). Over the years, the company has invested significantly in research and development, particularly in respiratory, dermatology, and oncology therapies, positioning itself as one of the few Indian pharma companies with meaningful innovation ambitions.

Key business segments

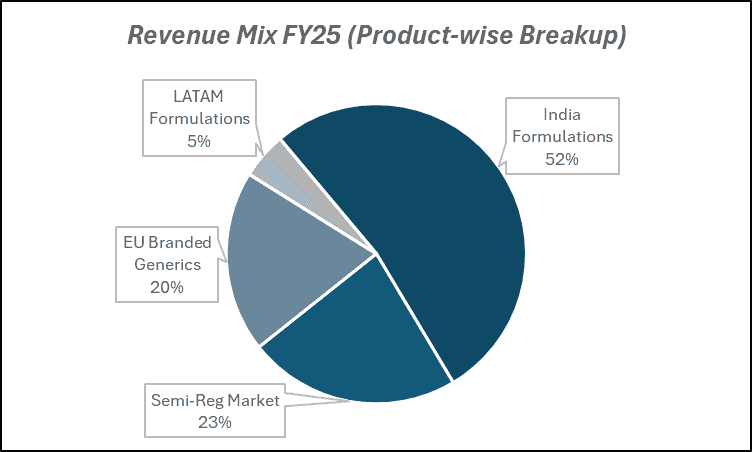

Glenmark Pharmaceuticals Ltd. operates primarily in the following key business segments:

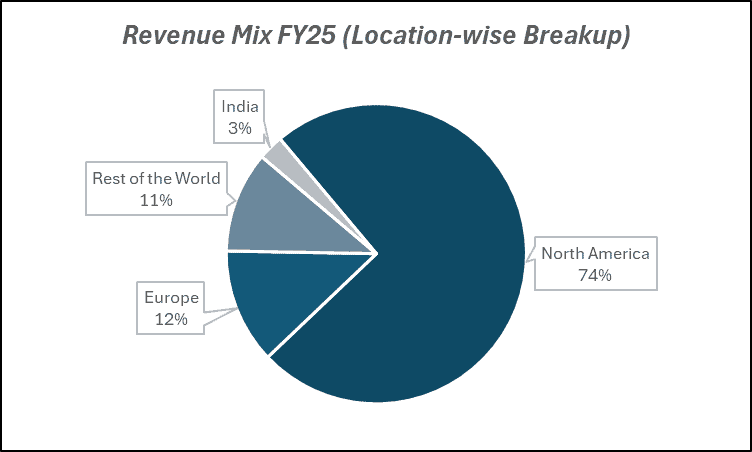

- North America Generics: Generic drug sales in the US market across multiple therapeutic categories.

- India Formulations: Branded prescription medicines across key therapeutic areas in the domestic market.

- Europe & Emerging Markets: Branded generics and specialty products across international markets.

- Active Pharmaceutical Ingredients (API): Manufacturing of APIs for internal use and external supply.

- Specialty & Innovation Pipeline: Development of novel molecules and specialty therapies.

Primary growth factors for Glenmark Pharmaceuticals Ltd.

Glenmark Pharmaceuticals Ltd. key growth drivers:

- Expansion in the US Generics Market: Increasing product launches and complex generics pipeline support revenue growth.

- Strong India Branded Formulations Business: Rising healthcare demand and doctor prescriptions support steady domestic growth.

- Specialty Drug Development: Pipeline in respiratory and dermatology therapies provides long-term value creation potential.

- Emerging Market Expansion: Growth across Latin America, Asia, and other emerging markets.

- Operational Efficiency & Debt Reduction: Balance sheet improvement and cost optimization supporting margin expansion.

Detailed competition analysis for Glenmark Pharmaceuticals Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Glenmark Pharmaceuticals Ltd. | 16468.13 | 4370.84 | 26.54% | 1065.02 | 6.47% | 54.06 |

| Aurobindo Pharma Ltd. | 33181.86 | 6846.39 | 20.63% | 3513.20 | 10.59% | 19.92 |

| Alkem Laboratories Ltd. | 14252.70 | 2879.11 | 20.20% | 2424.46 | 17.01% | 26.96 |

| Biocon Ltd. | 16827.40 | 3496.00 | 20.78% | 629.60 | 3.74% | 97.49 |

| Laurus Labs Ltd. | 6721.63 | 1686.20 | 25.09% | 841.81 | 12.52% | 66.17 |

Key insights on Glenmark Pharmaceuticals Ltd.

- Strong presence in both regulated and emerging pharmaceutical markets.

- Generics business provides stable cash flows supporting R&D investments.

- Specialty pipelines could unlock significant long-term value.

- India branded formulations segment remains a high-margin business.

- Diversified geographic presence reduces dependence on any single market.

Recent financial performance of Glenmark Pharmaceuticals Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 3387.55 | 6046.87 | 3900.62 | -35.49% | 15.15% |

| EBITDA (₹ Cr.) | 600.23 | 2359.55 | 869.75 | -63.14% | 44.90% |

| EBITDA Margin (%) | 17.72% | 39.02% | 22.30% | -1672 bps | 458 bps |

| PAT (₹ Cr.) | 348.03 | 610.43 | 403.23 | -33.94% | 15.86% |

| PAT Margin (%) | 10.27% | 10.10% | 10.34% | 24 bps | 7 bps |

| Adjusted EPS (₹) | 12.33 | 21.63 | 14.29 | -33.93% | 15.90% |

Glenmark Pharmaceuticals Ltd. financial update (Q3 FY26)

Financial performance

- Revenue grew 15.2% YoY to ₹3,901 Cr in Q3FY26, supported by strong growth in the India business, while US sales remained muted.

- Gross margin declined 259 bps YoY to 65.4%, impacted by an unfavorable product and geographic mix.

- EBITDA rose 44.9% YoY to ₹870 Cr, with margin improving to 22.3% aided by cost control measures.

- PAT increased 15.9% YoY to ₹403 Cr, reflecting operational leverage despite margin pressure.

- 9MFY26 revenue declined 6.8% YoY to ₹9,385 Cr, while profitability remained volatile due to margin compression and exceptional items.

Business highlights

- India formulation revenue grew 22.1% YoY to ₹1,298 Cr, driven by new launches and market share gains across therapies.

- US revenue remained stable at ~$93 Mn, with growth constrained by pricing pressure and limited differentiated launches.

- Four injectable products launched in the US during Q3, while multiple respiratory products including gFlovent are under filing/approval pipeline.

- The Monroe facility received regulatory clearance, enabling restart of commercial manufacturing from Q4FY26.

- Europe and RoW markets delivered 8–9% growth, supported by respiratory portfolio traction and recovery in LATAM markets.

Outlook

- Management expects EBITDA margins to improve toward 23% over the next four quarters driven by operating leverage and cost discipline.

- US growth recovery expected from respiratory and injectable launches, along with Monroe facility ramp-up.

- Innovative oncology portfolio and licensed assets are expected to become key growth drivers over the medium term.

- Revenue projected to grow at 6–7% CAGR over FY25–FY28, supported by new product launches and geographic expansion.

- Strengthening balance sheet and steady cash generation could support EBITDA margin expansion toward 20% by FY28.

Recent Updates on Glenmark Pharmaceuticals Ltd.

- Continued investment in specialty and innovation pipeline.

- New generic drug approvals and product launches in regulated markets.

- Strategic focus on respiratory and dermatology segments.

- Ongoing initiatives to strengthen the balance sheet and reduce leverage.

- Expansion of manufacturing capabilities for global markets.

Company valuation insights – Glenmark Pharmaceuticals Ltd.

Glenmark Pharmaceuticals is currently trading at a TTM P/E of 54.06x, significantly above the industry average of 32.40x, after delivering a strong 51.6% return over the last one year, substantially outperforming the NIFTY 50’s 8.9% gain. The premium valuation reflects improving investor confidence in the company’s earnings recovery, driven by margin expansion, stabilisation in the US business, and strong traction in its India formulations portfolio.

The investment case for Glenmark is supported by improving profitability, strengthening presence in key therapeutic segments, and a gradually stabilising global business. The India business continues to be a key growth driver, led by strong momentum in respiratory, oncology, and chronic therapies, along with continued market share gains across multiple brands. The company’s innovative oncology portfolio including Tevimbra, Brukinsa, and Akynzeo is witnessing increasing traction and is expected to emerge as a meaningful contributor to medium-term growth. In the US market, growth visibility is improving with the restart of commercial manufacturing at the Monroe facility and a pipeline of respiratory and injectable product launches. Additionally, Glenmark’s expanding innovation pipeline, including assets under its IGI platform and global partnerships for oncology and specialty therapies, could support long-term earnings growth. The company’s improving balance sheet, steady cash generation, and disciplined cost management further enhance earnings visibility over the medium term.

From a valuation perspective, applying a 33x multiple to FY27E EPS of ₹80, we derive a 12-month target price of ₹2,640, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹2,260, indicating a 6% upside, supported by improving margin trajectory, expected recovery in US operations, continued strength in India formulations, and steady progress across its innovation pipeline.

Major risk factors affecting Glenmark Pharmaceuticals Ltd.

- Pricing Pressure: Intense competition in the US generics market can compress margins.

- Regulatory Risk: FDA observations or compliance issues at manufacturing facilities.

- R&D Execution Risk: Failure or delays in specialty drug development.

- Currency Exposure: Global operations expose earnings to exchange rate fluctuations.

- High R&D Investment: Sustained spending required to maintain innovation pipeline.

Technical analysis of Glenmark Pharmaceuticals Ltd. share

Glenmark Pharmaceuticals is forming a cup and handle pattern, signalling a constructive consolidation phase within a broader uptrend. The stock is currently trading near the neckline zone, and a decisive breakout above this level could trigger renewed positive momentum, confirming continuation of the prevailing trend.

Importantly, the price is trading above its 20-, 50-, 100-, and 200-day EMAs, indicating strong structural alignment across multiple timeframes. This positioning suggests the broader trend remains positive, with these moving averages likely to act as dynamic support levels during near-term volatility.

Momentum indicators also reflect strengthening price action. The MACD at 31.96 is in positive territory and above the signal line, indicating improving bullish momentum and supporting the possibility of a breakout continuation.

The RSI at 60.30 signals healthy buying strength without entering overbought territory, leaving room for further upside. Additionally, the 21-day and 55-day Relative RSI readings at 0.14 indicate consistent outperformance versus the broader market, reinforcing the stock’s relative strength.

Meanwhile, the ADX at 12.42 indicates a range-bound phase, suggesting that the trend is still developing. However, a confirmed breakout above the neckline could strengthen trend intensity and trigger a fresh leg of the upside move.

A decisive move above ₹2,260 could open the path toward ₹2,640 and beyond, aligning with our 12-month fundamental target. On the downside, ₹2,000 remains a crucial support level; sustaining above this zone preserves the cup and handle structure while limiting downside risk.

- RSI: 60.30 (Bullish; healthy buying interest)

- ADX: 12.42 (Sideways; pattern breakout awaited)

- MACD: 31.96 (Positive; above the signal line)

- Resistance: ₹2,260

- Support: ₹2,000

Glenmark Pharmaceuticals Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹2,260 (6% upside) and a 12-month target of ₹2,640 (24% upside), based on 33x FY27E EPS of ₹80.

Why buy now?

Improving earnings trajectory, supported by margin expansion driven by cost optimisation and operating leverage across key geographies.

Strong India formulations growth, led by respiratory, oncology, and chronic therapies along with sustained market share gains across key brands.

Gradual stabilisation in the US business, aided by restart of commercial manufacturing at the Monroe facility and a pipeline of respiratory and injectable launches.

Innovative oncology portfolio gaining traction, with assets such as Tevimbra, Brukinsa, and Akynzeo expected to contribute meaningfully to medium-term growth.

Strengthening balance sheet and steady cash generation, enabling continued investment in R&D and innovation while maintaining financial discipline.

Portfolio fit

Glenmark Pharmaceuticals offers exposure to India’s structural pharmaceutical growth along with global specialty opportunities. With strong momentum in domestic formulations, improving visibility in the US generics business, and an expanding innovation pipeline through its IGI platform and global partnerships, the company is well positioned for sustainable earnings recovery over the medium term. The stock fits well in portfolios seeking a blend of domestic pharma growth, innovation-driven optionality, and improving profitability outlook.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebGlenmark Pharmaceuticals Ltd.: Budget 2026-27 opportunities

- Incentives for Domestic Pharma Manufacturing: Policies supporting local API and drug manufacturing.

- PLI Scheme Expansion: Production-linked incentives for pharmaceutical exports.

- Healthcare Spending Growth: Increased public healthcare spending boosting domestic demand.

- Innovation & R&D Support: Tax incentives or grants for pharmaceutical research.

- Export Promotion Policies: Strengthening India’s role as a global pharmaceutical supplier.

Final thoughts

Glenmark Pharmaceuticals Limited stands at an important strategic juncture, balancing its established generics franchise with ambitions in specialty drug development. With steady growth in domestic formulations, expanding global generics presence, and ongoing investments in innovative therapies, the company is positioning itself for long-term value creation.

For investors seeking exposure to India’s pharmaceutical sector with a blend of stable generics revenues and potential upside from specialty innovation, Glenmark offers a combination of defensive healthcare demand and pipeline-driven growth opportunities.