India’s real estate sector is in the midst of a structural upcycle, driven by urbanization, premiumization, and consolidation toward branded developers. As buyers increasingly prefer trusted names, large developers are gaining market share from unorganized players.

Among the key beneficiaries of this shift is Godrej Properties Ltd. (GPL), a developer that combines strong brand equity from the Godrej Group with an asset-light, partnership-driven growth model.

But does Godrej Properties Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | GODREJPROP |

| Industry/Sector | Realty |

| CMP | 1758.00 |

| Market Cap (₹ Cr.) | 52916 |

| P/E | 33.44 (Vs Industry P/E of 33.20) |

| 52 W High/Low | 2506.50 / 1434.00 |

| EPS (TTM) | 52.25 |

| Dividend Yield | 0.00% |

About Godrej Properties Ltd.

Godrej Properties Limited is one of India’s leading real estate developers, part of the Godrej Group. The company focuses on residential, commercial, and township developments across major cities such as Mumbai, Pune, Bengaluru, NCR, and Hyderabad.

Godrej Properties has differentiated itself through a brand-led, asset-light strategy, often entering projects via joint ventures and development agreements rather than outright land ownership, enabling capital efficiency and faster scale-up.

Key business segments

Godrej Properties Ltd. operates primarily in the following key business segments:

- Residential Real Estate: Premium, mid-income, and affordable housing projects.

- Townships & Mixed-Use Developments: Integrated developments across large land parcels.

- Commercial Real Estate: Office spaces and business parks.

- Joint Development Projects (JVs/JDAs): Asset-light partnerships for project execution.

- Land Development: Strategic land acquisition and monetization.

Primary growth factors for Godrej Properties Ltd.

Godrej Properties Ltd. key growth drivers:

- Market Share Gains from Unorganized Players: Shift toward branded developers post-RERA.

- Strong Launch Pipeline: Continuous project launches driving pre-sales growth.

- Asset-Light Business Model: Joint development strategy enabling capital efficiency.

- Premiumization Trend: Rising demand for branded, high-quality housing.

- Geographic Expansion: Entry into new cities and micro-markets.

Detailed competition analysis for Godrej Properties Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Godrej Properties Ltd. | 3795.03 | -828.81 | -21.84% | 1733.74 | 45.68% | 33.44 |

| Lodha Developers Ltd. | 16187.00 | 4729.00 | 29.21% | 3339.20 | 20.63% | 26.09 |

| The Phoenix Mills Ltd. | 4205.94 | 2447.15 | 58.18% | 1417.40 | 33.70% | 238.28 |

| Oberoi Realty Ltd. | 5409.37 | 3015.96 | 55.75% | 2209.38 | 40.84% | 27.83 |

| Prestige Estates Projects Ltd. | 10140.00 | 3204.70 | 31.60% | 1050.80 | 10.36% | 54.54 |

Key insights on Godrej Properties Ltd.

- Among the fastest-growing real estate developers in India.

- Strong brand trust due to Godrej Group legacy.

- The asset-light model reduces balance sheet risk.

- High pre-sales visibility supporting revenue growth.

- Aggressive business development pipeline.

Recent financial performance of Godrej Properties Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 968.88 | 740.38 | 498.36 | -32.69% | -48.56% |

| EBITDA (₹ Cr.) | 27.55 | -512.74 | -182.74 | 64.36% | -763.30% |

| EBITDA Margin (%) | 2.84% | -69.25% | -36.67% | 3258 bps | -3951 bps |

| PAT (₹ Cr.) | 176.48 | 486.13 | 208.22 | -57.17% | 17.99% |

| PAT Margin (%) | 18.21% | 65.66% | 41.78% | -2388 bps | 2357 bps |

| Adjusted EPS (₹) | 5.40 | 13.45 | 6.48 | -51.82% | 20.00% |

Godrej Properties Ltd. financial update (Q3 FY26)

Financial performance

- Revenue declined 48.6% YoY to ₹498 Cr in Q3FY26, largely due to timing of project deliveries and revenue recognition, despite strong underlying sales momentum.

- EBITDA remained negative at ₹183 Cr, impacted by sharp increase in construction costs and higher operating expenses.

- Margins stayed under pressure due to elevated cost structure and ongoing project execution intensity, reflecting near-term profitability challenges.

- PAT grew 18.0% YoY to ₹208 Cr, supported by a strong rise in other income rather than core operating performance.

- Overall profitability remained volatile, with earnings largely driven by non-operating income while core real estate margins are yet to normalize.

Business highlights

- Booking value surged 54.6% YoY, driven by strong demand with 3,973 homes sold and volumes rising 57.9% YoY to 6.43 mn sq ft.

- Customer collections increased 39.5% YoY to ₹4,282 Cr, indicating strong cash flow traction and healthy execution momentum.

- Added 3 new projects (7.3 mn sq ft) with ₹8,400 Cr potential booking value, strengthening future revenue visibility.

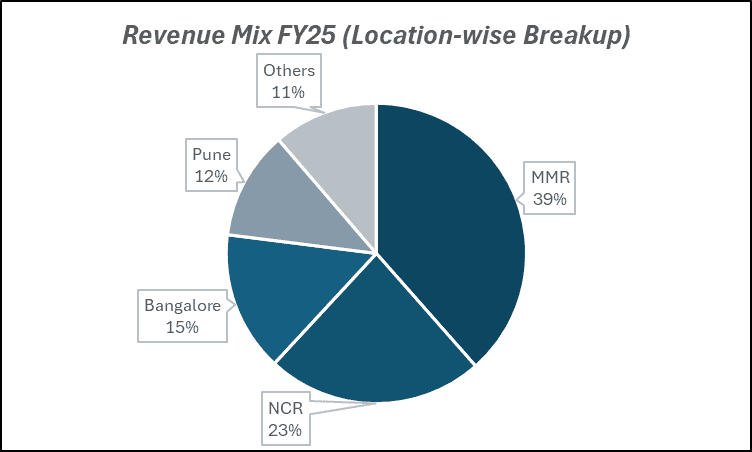

- Mumbai Metropolitan Region remained the key contributor (~₹3,239 Cr booking value), led by strong response to premium launches like Worli.

- Robust pipeline expansion continues, with multiple project additions supporting long-term growth visibility.

Outlook

- Strong launch pipeline and high-demand micro-market focus expected to sustain booking growth and sales velocity going forward.

- Revenue and earnings expected to improve meaningfully from Q4 onwards, supported by a large pipeline of project completions.

- Continued consolidation of joint ventures to enhance scalability and improve contribution to revenue and profitability.

- The medium-term outlook remains robust with multi-city expansion strategy and resilient real estate demand across core markets.

- Margins likely to gradually recover with operating leverage, better execution, and normalization of construction cost pressures.

Recent Updates on Godrej Properties Ltd.

- Strong addition of new projects through JDAs and partnerships.

- Expansion across key real estate markets in India.

- Continued leadership in pre-sales growth among peers.

- Focus on scaling operations with capital efficiency.

- Strengthening presence in premium housing segments.

Company valuation insights – Godrej Properties Ltd.

Godrej Properties Ltd is currently trading at a P/B ratio of 2.9x, with the stock delivering a -13.6% return over the last one year, underperforming the NIFTY 50’s 1.3% return during the same period.

The investment case for Godrej Properties is anchored in its strong launch pipeline, robust presales momentum, and multi-city presence across high-demand micro-markets. The company has demonstrated healthy booking value growth, supported by strong volume traction, while customer collections have also remained resilient. Its strategy of asset-light expansion through joint ventures, combined with a focus on premium residential developments, enables scalable growth with controlled balance sheet risk. Additionally, a large pipeline of upcoming launches, steady delivery momentum, and consolidation of JVs are expected to drive revenue visibility and earnings growth over the medium term. Despite near-term volatility due to timing of project deliveries and elevated construction costs, the company remains well positioned to benefit from sustained demand in core urban markets and improving real estate cycle tailwinds.

From a valuation perspective, applying a 2.2x P/B multiple to FY28E book value, we arrive at a 12-month target price of ₹2,180, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹1,870, indicating a 6% upside, supported by strong launch visibility, improving presales trajectory, and expected pickup in project deliveries.

Major risk factors affecting Godrej Properties Ltd.

- Execution Risk: Timely delivery of multiple projects across geographies.

- Real Estate Cyclicality: Demand sensitivity to interest rates and economic conditions.

- High Growth Expectations: Valuations sensitive to any slowdown in pre-sales.

- Regulatory Risk: Changes in real estate regulations and approvals.

- Land Acquisition Risk: Dependence on partnerships and project sourcing.

Technical analysis of Godrej Properties Ltd. share

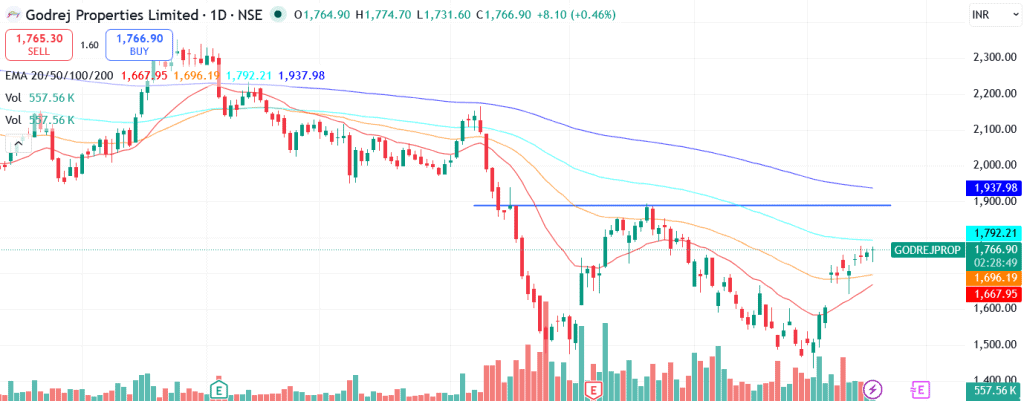

Godrej Properties Ltd has been consolidating over the past few months and is now showing signs of a structural reversal, with a double bottom pattern formation near key levels. The stock is currently approaching its neckline, and a decisive breakout from this zone could trigger a fresh upward move, indicating a shift from consolidation to a bullish trend.

Encouragingly, the stock is trading above its 20-day and 50-day EMAs, reflecting improving short-term strength. However, it remains below the 100-day and 200-day EMAs, indicating that the broader trend is still transitioning. This setup provides a favorable buying opportunity, especially if the breakout sustains.

Momentum indicators are supportive. The MACD at 26.46 is in positive territory and trading above the signal line, indicating strengthening bullish momentum. The RSI at 62.23 reflects good buying interest while still leaving room before entering overbought territory, suggesting further upside potential.

The Relative RSI (21-day at 0.06 and 55-day at 0.17) indicates outperformance versus the broader market, highlighting improving relative strength. Meanwhile, the ADX at 17.57 suggests that the trend is gradually strengthening, supporting the case for a sustained move higher.

A decisive breakout above ₹1870 (key resistance / neckline) could open up further upside towards ₹2180, aligning with the 12-month fundamental target. On the downside, ₹1640 remains a critical support level, below which the bullish structure may weaken.

- RSI: 62.23 (Good buying interest)

- ADX: 17.57 (Trend strengthening)

- MACD: 26.46 (Positive; above signal line)

- Resistance: ₹1870

- Support: ₹1640

Godrej Properties Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹1,870 (6% upside) and a 12-month target of ₹2,180 (24% upside), based on 2.2x FY28E book value.

Why buy now?

Strong launch pipeline and presales visibility, with multiple upcoming projects across key urban markets expected to drive booking growth.

Healthy demand across core micro-markets, supporting sustained sales velocity and pricing strength in the residential segment.

Asset-light growth strategy via joint ventures, enabling scale-up with controlled capital deployment and improved return ratios.

Robust business development momentum, with continuous addition of new projects enhancing long-term revenue visibility.

Improving earnings trajectory, supported by expected pickup in project deliveries, operating leverage, and normalization of construction costs over the medium term.

Portfolio fit

Godrej Properties Ltd offers exposure to India’s structural real estate upcycle, backed by a strong brand, pan-India presence, and execution capabilities across high-demand urban markets. Its asset-light JV model, robust launch pipeline, and steady presales growth provide visibility on future cash flows while maintaining balance sheet discipline. With a combination of scalable growth, improving profitability, and sector tailwinds, the stock fits well in portfolios seeking cyclical recovery plays with strong medium-term earnings visibility and premium real estate exposure.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebGodrej Properties Ltd.: Budget 2026-27 opportunities

- Affordable Housing Push: Government incentives boosting housing demand.

- Infrastructure Development: Improved connectivity enhancing real estate demand.

- Tax Benefits for Homebuyers: Encouraging property purchases.

- Urbanization Policies: Growth in housing demand across cities.

- Real Estate Sector Reforms: Continued formalization benefiting organized players.

Final thoughts

Godrej Properties Limited stands at the forefront of India’s real estate transformation, benefiting from consolidation, urbanization, and rising demand for branded housing. With a strong asset-light model, aggressive expansion strategy, and consistent pre-sales performance, the company is well positioned to capture long-term growth opportunities.

For investors seeking exposure to India’s real estate upcycle with a focus on growth and scalability, Godrej Properties offers a compelling blend of brand strength, execution capability, and structural tailwinds.