India’s energy transition is not just about generating more power, it’s about moving that power efficiently across the country. With renewable energy capacity expanding rapidly, the real bottleneck lies in transmission infrastructure and grid modernization.

This is where companies involved in power transmission and distribution (T&D) equipment play a crucial role. Among them, GVT&D Ltd. (GE Vernova T&D India) stands out as a key enabler of India’s evolving power ecosystem.

But does GE Vernova T&D India Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | GVT&D |

| Industry/Sector | Capital Goods |

| CMP | 4604.00 |

| Market Cap (₹ Cr.) | 1,17,172 |

| P/E | 107.82 (Vs Industry P/E of 60.44) |

| 52 W High/Low | 4650.00 / 1437.10 |

| EPS (TTM) | 41.71 |

| Dividend Yield | 0.11% |

About GE Vernova T&D India Ltd.

GE Vernova T&D India Limited is engaged in the manufacturing and supply of equipment and solutions for power transmission and distribution. The company is part of the global GE Vernova ecosystem, bringing advanced technology and engineering expertise to India’s power sector.

Its offerings include transformers, substations, grid solutions, and services that are critical for efficient electricity transmission and distribution.

Key business segments

GE Vernova T&D India Ltd. operates primarily in the following key business segments:

- Power Transformers: High-voltage transformers for transmission networks.

- Grid Solutions & Substations: Turnkey substation and grid infrastructure projects.

- Transmission Equipment: Products for high-voltage transmission systems.

- Services & Maintenance: Lifecycle services and grid support solutions.

- Renewable Integration Solutions: Equipment supporting solar and wind grid connectivity.

Primary growth factors for GE Vernova T&D India Ltd.

GE Vernova T&D India Ltd. key growth drivers:

- Renewable Energy Expansion: Increasing need for grid infrastructure to support solar and wind projects.

- Transmission Network Investments: Government-led expansion of national grid capacity.

- Grid Modernization & Smart Grids: Digitalization and automation of power networks.

- Electrification & Energy Demand Growth: Rising power consumption across sectors.

- Export Opportunities: Supply of transmission equipment to global markets.

Detailed competition analysis for GE Vernova T&D India Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| GE Vernova T&D India Ltd. | 5721.77 | 1490.83 | 26.06% | 1067.97 | 18.67% | 107.82 |

| ABB India Ltd. | 13202.73 | 2043.00 | 15.47% | 1669.40 | 12.64% | 96.15 |

| Hitachi Energy India Ltd. | 7277.34 | 1037.17 | 14.25% | 841.27 | 11.56% | 168.07 |

| Siemens Ltd. | 17607.70 | 2027.90 | 11.52% | 1585.50 | 9.00% | 77.83 |

| CG Power Ltd. | 11728.96 | 1502.07 | 12.81% | 1109.48 | 9.46% | 118.96 |

Key insights on GE Vernova T&D India Ltd.

- Strategic positioning in India’s power infrastructure ecosystem.

- Strong backing and technology access from global GE Vernova group.

- Beneficiary of renewable energy and grid expansion trends.

- Project-based revenue model with execution visibility.

- Operating leverage potential during capex upcycles.

Recent financial performance of GE Vernova T&D India Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 1073.65 | 1538.46 | 1700.64 | 10.54% | 58.40% |

| EBITDA (₹ Cr.) | 179.68 | 396.46 | 454.63 | 14.67% | 153.02% |

| EBITDA Margin (%) | 16.74% | 25.77% | 26.73% | 96 bps | 999 bps |

| PAT (₹ Cr.) | 142.68 | 299.48 | 290.80 | -2.90% | 103.81% |

| PAT Margin (%) | 13.29% | 19.47% | 17.10% | -237 bps | 381 bps |

| Adjusted EPS (₹) | 5.57 | 11.70 | 11.36 | -2.91% | 103.95% |

GE Vernova T&D India Ltd. financial update (Q3 FY26)

Financial performance

- Revenue grew 58% YoY, driven by strong execution across domestic and export projects amid a robust power transmission capex cycle.

- EBITDA margins improved sharply by 999 bps YoY to 26.73%, supported by operating leverage and a favorable product mix.

- Profitability remained strong, with PAT increasing 104% YoY, reflecting healthy operating performance.

- Margins remained at elevated levels, aided by disciplined project selection and higher contribution from high-value segments like HVDC and grid solutions.

- Overall earnings trajectory continues to strengthen, backed by execution momentum and structurally improving margin profile.

Business highlights

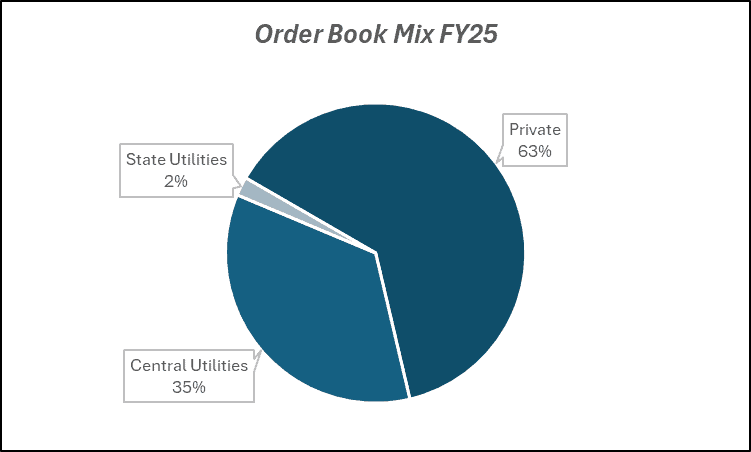

- Order inflows remained robust, with strong traction across HVDC, grid solutions, and export markets, reinforcing long-term revenue visibility.

- Order backlog remains strong, providing visibility for 3.5–4 years of revenue growth.

- Secured marquee HVDC projects including the Khavda–South Olpad project and Chandrapur refurbishment, strengthening positioning in complex transmission projects.

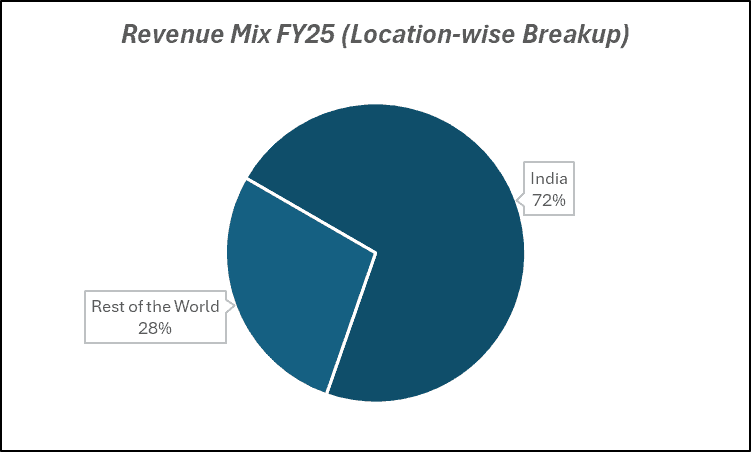

- The export segment continues to scale up, supported by global parent linkage and India’s emergence as a manufacturing hub, with a higher margin profile compared to domestic business.

- Diversified demand drivers across power utilities, renewables, data centres, railways, and electrification continue to support sustained order momentum.

Outlook

- Strong industry tailwinds driven by rising power demand, renewable integration, EV infrastructure, and data centre expansion are expected to sustain order inflows.

- The large HVDC pipeline over the next few years provides significant opportunity for order wins and long-term growth visibility.

- Revenue growth is expected to accelerate over the medium term, supported by execution of large projects and rising contributions from HVDC.

- Margins are likely to remain strong, supported by operating leverage, favorable project mix, and continued focus on high-value opportunities.

- Long-term outlook remains structurally robust, driven by the transmission capex upcycle, limited competition in HVDC space, and strong global positioning.

Recent Updates on GE Vernova T&D India Ltd.

- Increasing participation in grid expansion and substation projects.

- Focus on renewable energy integration solutions.

- Strengthening order book from domestic utilities.

- Expansion of service offerings and lifecycle solutions.

- Growing emphasis on digital and smart grid technologies.

Company valuation insights – GE Vernova T&D India Ltd.

GE Vernova T&D India is currently trading at a TTM P/E of 107.8x, significantly higher than the industry average of 60.4x, with the stock delivering a strong 204.7% return over the last one year, sharply outperforming the NIFTY 50’s -1.4% return during the same period.

The investment case for GE Vernova T&D India is anchored in its strong positioning within the power transmission upcycle, particularly in the high-entry-barrier HVDC segment. The company benefits from robust demand tailwinds driven by renewable energy integration, rising power consumption, data centre expansion, and electrification initiatives. Its technological leadership in HVDC and grid solutions, coupled with a selective bidding strategy focused on high-margin projects, enables superior profitability and execution efficiency. A strong and growing order book provides multi-year revenue visibility, while increasing export opportunities and global parent support further strengthen growth prospects. Additionally, limited competition in complex HVDC projects and a large upcoming project pipeline position the company well for sustained order inflows and long-term value creation.

From a valuation perspective, applying a 70x multiple to FY28E EPS of ₹82, we arrive at a 12-month target price of ₹5,740, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹4,900, indicating a 6% upside, supported by strong order inflows, execution momentum, and continued traction in the power transmission capex cycle.

Major risk factors affecting GE Vernova T&D India Ltd.

- Execution Risk: Delays in project execution affecting revenues.

- Order Inflow Volatility: Dependence on large project wins.

- Capex Cycle Dependency: Linked to power sector investments.

- Competition: Presence of global and domestic players in T&D space.

- Working Capital Intensity: Project-based business requiring significant capital.

Technical analysis of GE Vernova T&D India Ltd. share

GE Vernova T&D India has been in a strong uptrend, consistently forming higher highs and higher lows, indicating sustained bullish momentum. The stock continues to trade firmly above all its key moving averages (20, 50, 100, and 200-day EMAs), reflecting strength across short, medium, and long-term timeframes. This alignment suggests a well-established bullish structure with strong institutional participation.

Momentum indicators remain highly supportive of the ongoing trend. The MACD at 198.91 is firmly in positive territory and trading above the signal line, indicating continued bullish momentum. The RSI at 73.23 reflects strong buying interest, albeit nearing overbought territory, which is typical in strong trending stocks and often sustains during extended rallies.

The Relative RSI (21-day at 0.14 and 55-day at 0.46) highlights clear outperformance versus the broader market, reinforcing the stock’s leadership within the capital goods and power transmission space. Additionally, the ADX at 36.25 indicates a strong trend in place, supporting the continuation of the current up move rather than a short-lived rally.

A sustained move above ₹4,900 (key resistance) could trigger the next leg of the rally, with potential upside towards ₹5,740, aligning with the 12-month fundamental target. On the downside, ₹4,300 acts as a crucial support level, below which the current bullish structure may weaken.

- RSI: 73.23 (Good buying interest)

- ADX: 36.25 (Strong Trend)

- MACD: 198.91 (Positive; above signal line)

- Resistance: ₹4,900

- Support: ₹4,300

GE Vernova T&D India Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹4,900 (6% upside) and a 12-month target of ₹5,740 (24% upside), based on 70x FY28E EPS of ₹82.

Why buy now?

Strong order book visibility with a multi-year execution pipeline, providing revenue certainty over the next 3-4 years.

Positioned as a key beneficiary of the power transmission capex upcycle, driven by renewables, electrification, and rising power demand.

Leadership in high-entry-barrier HVDC segment, enabling participation in large, high-margin projects with limited competition.

Robust order inflow pipeline, supported by a large upcoming HVDC opportunity set and sustained demand across domestic and export markets.

Improving profitability profile, driven by operating leverage, favorable project mix, and increasing contribution from high-margin products and exports.

Portfolio fit

GE Vernova T&D India offers exposure to India’s structural power and electrification theme, backed by strong technological capabilities and a leadership position in complex grid solutions. Its presence across the power value chain, coupled with global parent support and rising export opportunities, provides strong earnings visibility and scalability. With a combination of high growth, improving margins, and structural tailwinds from the energy transition and infrastructure capex cycle, the stock fits well in portfolios seeking exposure to long-term infrastructure themes with strong execution visibility and operating leverage benefits.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebGE Vernova T&D India Ltd.: Budget 2026-27 opportunities

- Power Infrastructure Spending: Increased government investment in transmission networks.

- Green Energy Corridors: Dedicated transmission lines for renewable energy.

- Smart Grid Initiatives: Digitalization of power distribution systems.

- Electrification Push: Expansion of electricity access and reliability.

- Export Promotion Policies: Opportunities in global power infrastructure markets.

Final thoughts

GE Vernova T&D India Limited stands at the heart of India’s evolving energy landscape, benefiting from rising electricity demand, renewable expansion, and grid modernization. With strong technological backing, growing order visibility, and exposure to long-term infrastructure trends, the company is well positioned for growth.

For investors seeking exposure to India’s power infrastructure and energy transition theme, GVT&D offers a compelling combination of cyclical capex upside and structural growth opportunity.