India’s specialty chemicals sector is emerging as a global growth engine, driven by China+1 supply chain shifts, rising domestic demand, and increasing focus on advanced materials. Within this space, companies that combine traditional chemical strengths with future-ready applications are gaining significant investor attention.

HSCL Ltd. (Himadri Speciality Chemical Limited) is one such player, evolving from a carbon materials company into a specialty chemicals and advanced materials platform, with growing exposure to lithium-ion battery materials.

But does Himadri Speciality Chemical Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | HSCL |

| Industry/Sector | Chemicals |

| CMP | 563.70 |

| Market Cap (₹ Cr.) | 28,441 |

| P/E | 38.50 (Vs Industry P/E of 40.87) |

| 52 W High/Low | 605.00 / 410.20 |

| EPS (TTM) | 13.93 |

| Dividend Yield | 0.15% |

About Himadri Speciality Chemica Ltd.

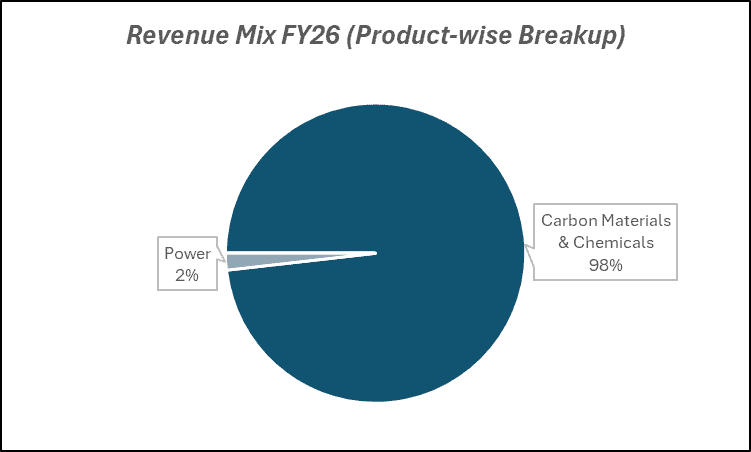

Himadri Speciality Chemical Limited is a leading specialty chemicals company engaged in the production of carbon materials and advanced chemical products. The company has a strong presence in coal tar derivatives, carbon black, and specialty chemicals, catering to industries such as tires, aluminum, graphite, and energy storage.

In recent years, HSCL has been focusing on value-added products and lithium-ion battery materials, positioning itself for long-term growth in the energy transition ecosystem.

Key business segments

Himadri Speciality Chemical Ltd. operates primarily in the following key business segments:

- Carbon Materials: Coal tar pitch, carbon black, and related products.

- Specialty Chemicals: High-value chemical derivatives for industrial applications.

- Advanced Materials: Products used in lithium-ion batteries and energy storage.

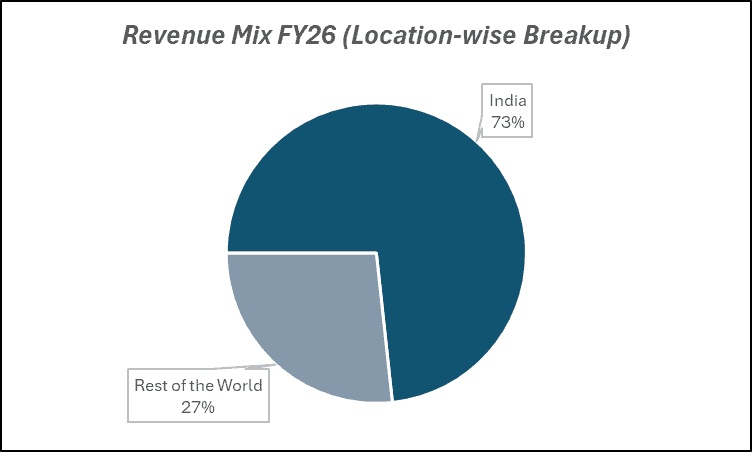

- Exports: Supply to global markets across multiple industries.

- By-products & Derivatives: Value-added outputs from core chemical processes.

Primary growth factors for Himadri Speciality Chemical Ltd.

Himadri Speciality Chemical Ltd. key growth drivers:

- Specialty Chemicals Demand Growth: Increasing global demand for high-value chemical products.

- Lithium-Ion Battery Materials Opportunity: Entry into energy storage materials with long-term growth potential.

- China+1 Supply Chain Shift: Global customers diversifying sourcing toward India.

- Export Expansion: Growing international presence and revenue diversification.

- Value-Added Product Mix: Shift toward higher-margin specialty and advanced materials.

Detailed competition analysis for Himadri Speciality Chemical Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Himadri Speciality Chemicals Ltd. | 4660.70 | 962.14 | 20.64% | 755.07 | 16.20% | 38.50 |

| Coromandel International Ltd. | 30464.27 | 3154.29 | 10.35% | 2378.64 | 7.81% | 25.46 |

| UPL Ltd. | 49077.00 | 8905.00 | 18.14% | 2149.00 | 4.38% | 27.03 |

| PI Industries Ltd. | 6935.60 | 1818.30 | 26.22% | 1444.50 | 20.83% | 32.08 |

| Deepak Nitrite Ltd. | 7946.43 | 921.24 | 11.59% | 533.32 | 6.71% | 44.27 |

Key insights on Himadri Speciality Chemical Ltd.

- Strong integration across the carbon and chemical value chain.

- Transitioning from commodity to specialty and advanced materials.

- Early positioning in the battery materials ecosystem.

- Export-oriented business with a global client base.

- Operating leverage benefits during demand upcycles.

Recent financial performance of Himadri Speciality Chemical Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 1134.64 | 1183.62 | 1287.76 | 8.80% | 13.50% |

| EBITDA (₹ Cr.) | 233.31 | 242.61 | 241.74 | -0.36% | 3.61% |

| EBITDA Margin (%) | 20.56% | 20.50% | 18.77% | -173 bps | -179 bps |

| PAT (₹ Cr.) | 155.46 | 192.04 | 207.53 | 8.07% | 33.49% |

| PAT Margin (%) | 13.70% | 16.22% | 16.12% | -10 bps | 242 bps |

| Adjusted EPS (₹) | 3.15 | 3.81 | 3.98 | 4.46% | 26.35% |

Himadri Speciality Chemical Ltd. financial update (Q4 FY26)

Financial performance

- Revenue grew 13.5% YoY to ₹1,287.8 crore (vs ₹1,134.6 crore in Q4 FY25), supported by strong demand across key segments.

- Profitability remained strong, with PAT rising 33.4% YoY to ₹207.5 crore.

- PAT margins expanded 242 bps YoY to 16.12%, reflecting improved operational efficiency and cost control.

- Gross margins remained firm, aided by softening input costs and higher share of value-added products.

- Overall earnings profile continues to strengthen, supported by scale-up in high-margin segments and disciplined cost management.

Business highlights

- Strong performance driven by improved realizations and steady demand across core business segments.

- Margin profile remained healthy despite minor QoQ moderation, indicating resilience in operating performance.

- Export contribution continued to support overall growth, benefiting from favorable global demand dynamics.

- Focus on value-added products and operational efficiencies contributed to sustained profitability.

- Stable execution across segments ensured consistent growth visibility and earnings stability.

Outlook

- Revenue growth expected to remain steady, supported by demand visibility and execution momentum.

- Margins likely to sustain at healthy levels, driven by cost efficiencies and product mix optimization.

- Continued focus on high-value segments expected to support profitability expansion.

- Growth in exports and specialty segments to remain key drivers going forward.

- Overall outlook remains positive, with a stable earnings trajectory and improving return profile.

Recent Updates on Himadri Speciality Chemical Ltd.

- Increasing focus on lithium-ion battery material development.

- Expansion of specialty chemical product portfolio.

- Strengthening export footprint across geographies.

- Capacity expansion initiatives in high-value segments.

- Strategic shift toward sustainability and advanced materials.

Company valuation insights – Himadri Speciality Chemical Ltd.

Himadri Speciality Chemical Ltd is currently trading at an EV/EBITDA of 25x, compared to its historical averages, with the stock delivering a return of 26.5% over the last one year, outperforming the NIFTY 50 which declined by 0.9% during the same period.

The investment case for HSCL is anchored in its strong positioning within niche, high-growth segments of the specialty chemicals space, particularly advanced carbon materials and lithium-ion battery value chains. The company is well placed to benefit from structural tailwinds such as increasing electric vehicle adoption, rising demand for energy storage, and broader industrial applications of specialty carbon products. Its integrated business model, diversified product portfolio, and focus on high-margin, value-added segments support superior profitability and margin resilience. Additionally, ongoing capacity expansions, improving export mix, and strong relationships with global clients provide robust revenue visibility, while disciplined capital allocation and execution capabilities further strengthen long-term growth prospects.

From a valuation perspective, applying a 21x EV/EBITDA multiple, we arrive at a 12-month target price of ₹700, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹600, indicating a 6% upside, supported by steady earnings visibility, improving product mix, and continued demand momentum in specialty chemicals.

Major risk factors affecting Himadri Speciality Chemical Ltd.

- Raw Material Price Volatility: Dependence on coal tar derivatives.

- Execution Risk: Scaling advanced materials and battery segments.

- Cyclical Demand Risk: Exposure to industrial and commodity cycles.

- Competition: Global and domestic competition in specialty chemicals.

- Technology Risk: Rapid evolution in battery materials and energy storage.

Technical analysis of Himadri Speciality Chemical Ltd. share

Himadri Speciality Chemical has transitioned into a strong bullish phase after forming a triple bottom pattern, followed by a decisive breakout above its neckline, an indication of a structural trend reversal from consolidation to expansion. This breakout is technically significant as it reflects strong demand absorption at lower levels and a shift in market sentiment in favor of buyers.

The stock is now trading comfortably above all its key moving averages (20, 50, 100, and 200-day EMAs), reinforcing strength across timeframes and confirming a well-aligned bullish setup. This positioning typically signals sustained institutional interest and trend continuation rather than a short-term move.

Momentum indicators further validate the bullish bias. The MACD at 24.56 remains in positive territory and above the signal line, suggesting continued upward momentum. The RSI at 82.38 indicates very strong buying interest, even though it is in the overbought zone, something often observed in high-momentum breakout stocks where rallies tend to extend further.

The Relative RSI (21-day at 0.22 and 55-day at 0.29) highlights consistent outperformance versus broader benchmarks, establishing HSCL as a relative leader within its segment. Meanwhile, the ADX at 25.83 confirms a strong and developing trend, indicating that the current move has strength and is not merely a short-lived spike.

A decisive move above ₹600 (key resistance) could act as a trigger for the next leg of the rally, with potential upside towards ₹700, in line with the 12-month fundamental target. On the downside, ₹530 serves as a critical support level, below which the bullish structure could lose strength.

- RSI: 82.38 (Very strong buying interest)

- ADX: 25.83 (Strong trend)

- MACD: 24.56 (Positive; above signal line)

- Resistance: ₹600

- Support: ₹530

Himadri Speciality Chemical Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹600 (6% upside) and a 12-month target of ₹700 (24% upside), based on 21x EV/EBITDA.

Why buy now?

Strong demand visibility in specialty carbon materials, particularly from lithium-ion batteries and energy storage applications, providing a multi-year growth runway.

Well positioned to benefit from structural tailwinds such as EV adoption, renewable energy expansion, and increasing industrial demand for high-performance carbon products.

Integrated operations across the value chain, ensuring better cost control, margin stability, and supply chain reliability.

Expanding global footprint with rising export contribution, enabling diversification of revenue streams and access to higher-margin markets.

Improving profitability profile, supported by a shift towards value-added products, operating leverage from capacity expansions, and disciplined capital allocation.

Portfolio fit

Himadri Speciality Chemical Ltd offers exposure to the structural growth theme of specialty chemicals and advanced materials, particularly linked to the global energy transition. Its focus on high-margin niche segments, strong execution track record, and increasing relevance in the EV and battery ecosystem provide strong earnings visibility and scalability. With a combination of consistent growth, margin expansion, and favorable industry tailwinds, the stock fits well in portfolios seeking exposure to emerging materials and long-term manufacturing themes.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebHimadri Speciality Chemical Ltd.: Budget 2026-27 opportunities

- PLI Scheme for Chemicals & Advanced Materials: Incentives supporting domestic manufacturing.

- EV & Battery Ecosystem Push: Demand for lithium-ion battery materials.

- Export Promotion Policies: Strengthening India’s role in global chemical supply chains.

- Make in India for Chemicals: Reduced dependence on imports.

- Sustainability & Green Energy Initiatives: Growth in advanced and eco-friendly materials.

Final thoughts

Himadri Speciality Chemical Limited stands at an important inflection point, leveraging its strong base in carbon materials to move up the value chain into specialty chemicals and advanced materials. With exposure to emerging sectors like lithium-ion batteries and strong export growth potential, the company is well positioned to benefit from both cyclical and structural tailwinds.

For investors seeking exposure to India’s specialty chemicals sector with added optionality from energy transition themes, HSCL offers a compelling blend of current profitability and future growth potential.