India’s IT services sector has long been a cornerstone of global outsourcing, but the narrative is evolving. The focus is shifting from traditional IT services to cloud, digital transformation, AI, and platform-led solutions.

In this transformation journey, mid-tier IT companies with niche expertise and strong client relationships are carving out meaningful growth opportunities. Mphasis Ltd. is one such player, combining deep domain expertise with a focused strategy on next-gen technologies.

But does Mphasis Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | MPHASIS |

| Industry/Sector | Information Technology |

| CMP | 2312.00 |

| Market Cap (₹ Cr.) | 44,117 |

| P/E | 24.66 (Vs Industry P/E of 20.74) |

| 52 W High/Low | 3037.20 / 2013.00 |

| EPS (TTM) | 94.30 |

| Dividend Yield | 2.44% |

About Mphasis Ltd.

Mphasis Limited is a global IT services company specializing in cloud, cognitive services, and digital transformation. Headquartered in Bengaluru, the company primarily serves clients in the banking, financial services, and insurance (BFSI) sector.

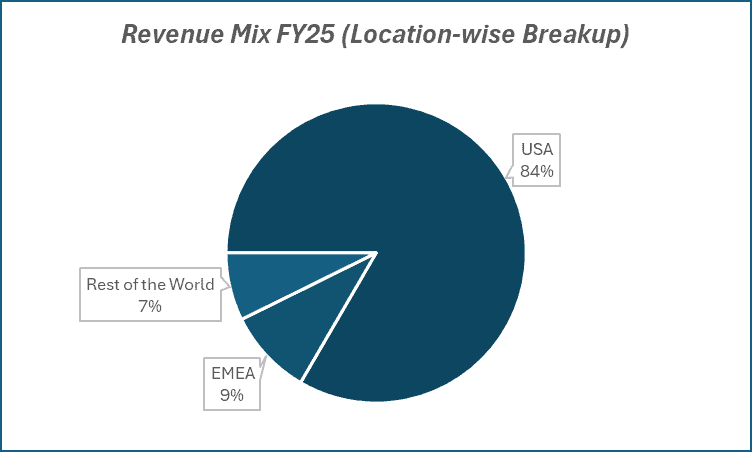

Mphasis operates with a strong focus on next-generation technologies such as cloud computing, AI, and automation. With a significant presence in the US and other developed markets, the company derives a large portion of its revenue from global clients.

Key business segments

Mphasis Ltd. operates primarily in the following key business segments:

- BFSI IT Services: Technology solutions for banking, financial services, and insurance clients.

- Cloud & Digital Transformation: Cloud migration, AI, and data analytics solutions.

- Application Services: Development, maintenance, and modernization of applications.

- Infrastructure Services: IT infrastructure management and support.

- Consulting & Platforms: Digital consulting and platform-based solutions.

Primary growth factors for Mphasis Ltd.

Mphasis Ltd. key growth drivers:

- Cloud Transformation Demand: Increasing adoption of cloud services across enterprises.

- Strong BFSI Client Base: Stable demand from financial institutions for IT services.

- Digital & AI Adoption: Growth in next-gen technologies such as AI and automation.

- Deal Wins & Client Mining: Expansion within existing clients and new deal pipelines.

- Operational Efficiency & Margin Focus: Improved delivery models supporting profitability.

Detailed competition analysis for Mphasis Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Mphasis Ltd. | 15347.02 | 2880.69 | 18.77% | 1802.93 | 11.75% | 24.66 |

| Persistent Systems Ltd. | 13934.62 | 2612.15 | 18.75% | 1731.62 | 12.43% | 49.43 |

| Oracle Financial Services Ltd. | 7323.20 | 3177.60 | 43.39% | 2441.50 | 33.34% | 25.86 |

| Coforge Ltd. | 15272.30 | 2566.70 | 16.81% | 1314.20 | 8.61% | 29.66 |

| L&T Technology Services Ltd. | 11751.40 | 1942.50 | 16.53% | 1258.60 | 10.71% | 28.99 |

Key insights on Mphasis Ltd.

- Strong positioning in the BFSI vertical providing revenue stability.

- Increasing focus on high-margin digital and cloud services.

- High exposure to global markets, especially the US.

- Consistent deal wins supporting revenue visibility.

- Transition from traditional IT services to next-gen offerings.

Recent financial performance of Mphasis Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 3561.34 | 3901.91 | 4002.58 | 2.58% | 12.39% |

| EBITDA (₹ Cr.) | 678.00 | 723.58 | 751.68 | 3.88% | 10.87% |

| EBITDA Margin (%) | 19.04% | 18.54% | 18.78% | 24 bps | -26 bps |

| PAT (₹ Cr.) | 427.81 | 471.04 | 443.70 | -5.80% | 3.71% |

| PAT Margin (%) | 12.01% | 12.07% | 11.09% | -98 bps | -92 bps |

| Adjusted EPS (₹) | 22.56 | 24.65 | 23.20 | -5.88% | 2.84% |

Mphasis Ltd. financial update (Q3 FY26)

Financial performance

- Revenue grew 12% YoY to ₹4003 Cr, supported by steady growth across BFSI and technology verticals.

- EBITDA increased 11% YoY to ₹752 Cr, with margins largely stable at 18.8% despite cost pressures.

- PAT growth remained modest at 4% YoY (reported), impacted by exceptional items and higher tax outgo.

- Gross profit grew 10.7% YoY, reflecting steady operating performance and execution strength.

- Margins remained stable across levels (EBITDA 19%, PAT 11%), indicating disciplined cost management amid investments.

Business highlights

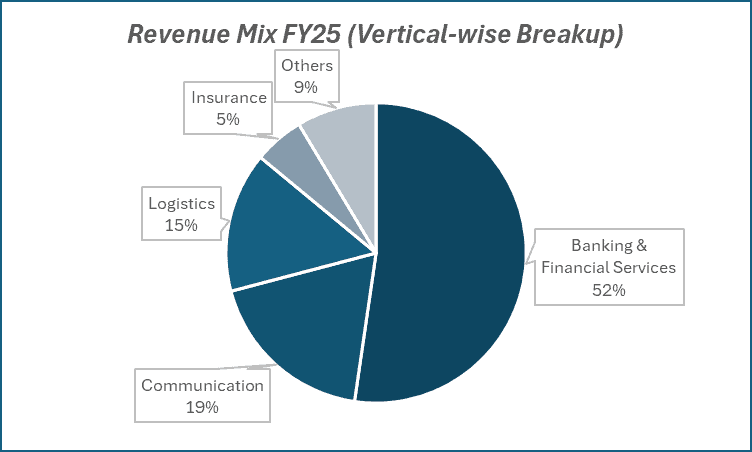

- The BFSI segment remained the key growth driver, contributing 66% of revenue with strong double-digit YoY growth.

- Insurance and TMT verticals delivered strong traction, with insurance witnessing strong growth momentum.

- Deal wins remained healthy with strong TCV traction, supported by large deal conversions across geographies.

- AI-led pipeline expanded significantly, with strong traction in AI-driven transformation deals.

- Logistics vertical margins recovered sharply, supporting overall margin stability during the quarter.

Outlook

- Revenue growth expected to outpace industry growth in FY26, supported by strong deal pipeline and ramp-ups.

- Continued focus on AI-led transformation and application modernization to drive long-term growth.

- BFSI vertical to remain a key growth engine, backed by strong pipeline and client spending visibility.

- Strong large deal pipeline and AI-led deals to support future revenue acceleration and operating leverage.

- Margin discipline expected within 18.75 – 19.75% band while continuing investments in AI platforms and capabilities.

Recent Updates on Mphasis Ltd.

- Increased focus on cloud and AI-driven solutions.

- Strategic deal wins across BFSI clients.

- Expansion of digital transformation service offerings.

- Continued investment in platform-based solutions.

- Strengthening partnerships with global technology providers.

Company valuation insights – Mphasis Ltd.

Mphasis is currently trading at a TTM P/E of 24.66x, at a premium to the industry average of 20.74x, while delivering a relatively muted return of 1.9% over the last one year, broadly in line with the NIFTY 50’s return of 2.2% during the same period.

The investment case for Mphasis is anchored in its strong positioning in BFSI and insurance verticals, which continue to drive growth through wallet share gains, steady ramp-up of large deals, and strong traction in new accounts. The company is benefiting from a robust deal pipeline and strong TCV conversion, with increasing exposure to large deals providing medium-term revenue visibility. Additionally, its strategic focus on AI-led transformation, supported by the scaling of its NeoIP platform, is strengthening its competitive positioning as enterprises shift towards outcome-based and platform-driven engagements. With a high proportion of AI-led deals, expanding large deal pipelines, and improving traction in application modernization, Mphasis is well placed to outperform industry growth, while maintaining margin discipline through controlled reinvestments.

From a valuation perspective, applying a 22x P/E multiple to FY28E EPS of ₹130, we derive a 12-month target price of ₹2,860, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹2,450, indicating a 6% upside, supported by strong deal momentum, AI-led growth opportunities, and sustained traction in core BFSI verticals.

Major risk factors affecting Mphasis Ltd.

- Client Concentration Risk: High dependence on the BFSI sector.

- Global Economic Slowdown: Impact on IT spending by global clients.

- Currency Risk: Fluctuations in exchange rates affecting revenues.

- Talent Costs: Rising employee costs impacting margins.

- Technology Disruption: Rapid changes in technology requiring continuous investment.

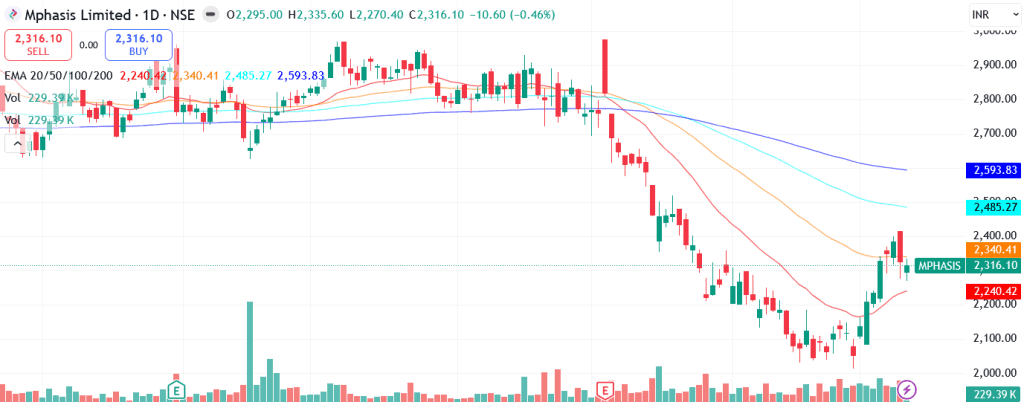

Technical analysis of Mphasis Ltd. share

Mphasis has witnessed a meaningful correction in line with broader market weakness, but the stock now appears to be stabilizing near a key support zone and is showing early signs of a trend reversal. The recent price action indicates renewed buying interest, supported by improving momentum indicators.

The stock has moved above its 20-day EMA and is approaching a crossover above the 50-day EMA, signaling strengthening short-term momentum. While it still trades below its 100- and 200-day EMAs, this phase offers a potential early entry opportunity if the recovery sustains and broader trend alignment follows.

Momentum indicators are clearly supportive. The MACD at 6.80 is firmly in positive territory and trading well above the signal line, indicating strong bullish momentum and the possibility of continued upside. The RSI at 55.97 reflects healthy buying interest without being overbought, suggesting further room for upward movement.

The Relative RSI (21-day at 0.07) indicates short-term outperformance against the broader market, signaling improving relative strength. Meanwhile, the ADX at 24.73 suggests a strengthening trend, reinforcing the likelihood of a sustained recovery phase.

A decisive move above ₹2,450 (resistance zone) could trigger further upside toward ₹2,860, aligning with the 12-month fundamental target. On the downside, ₹2,170 remains a key support level, below which the recovery structure may weaken.

- RSI: 55.97 (Decent buying interest)

- ADX: 24.73 (Trend strengthening)

- MACD: 6.80 (Positive; above signal line)

- Resistance: ₹2,450

- Support: ₹2,170

Mphasis Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹2,450 (6% upside) and a 12-month target of ₹2,860 (24% upside), based on 22x FY28E EPS.

Why buy now?

Strong growth visibility supported by a robust deal pipeline and steady conversion of large TCV wins into revenues.

Continued momentum in BFSI and insurance verticals, driven by wallet share gains, new client additions, and resilient demand.

Increasing share of AI-led and platform-driven deals, positioning the company well for the ongoing enterprise digital transformation cycle.

Expanding a large deal pipeline, providing medium-term revenue visibility and scalability benefits.

Margin discipline maintained within a guided band, with operating leverage expected to improve as large deals ramp up.

Portfolio fit

Mphasis offers exposure to the global IT services and digital transformation theme, with a strong focus on BFSI-led growth and increasing capabilities in AI-driven modernization. Its positioning in high-value, outcome-based engagements and growing presence in large deals provide visibility on sustained revenue growth. With a balanced approach between growth investments and margin discipline, along with strong deal momentum and pipeline strength, the stock fits well in portfolios seeking steady compounding from global technology spending with improving earnings visibility.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebMphasis Ltd.: Budget 2026-27 opportunities

- Digital India Push: Increased demand for IT services and digital infrastructure.

- AI & Technology Investments: Growth in enterprise technology spending.

- Startup & Innovation Ecosystem: Increased demand for digital and IT services.

- Global Capability Centers (GCCs): Expansion of global companies’ tech centers in India.

- Export Promotion Policies: Strengthening India’s IT services exports.

Final thoughts

Mphasis Limited stands at a critical point in the IT services evolution, transitioning from traditional outsourcing to a digital-first, cloud-led services model. With a strong BFSI franchise, consistent deal pipeline, and increasing focus on next-gen technologies, the company is well positioned to capture emerging opportunities in global IT spending.

For investors seeking exposure to the IT sector with a balance of stability and growth, Mphasis offers a combination of steady execution, digital transformation upside, and long-term global demand tailwinds.