India’s consumption story is evolving rapidly, from basic staples to branded, premium, and health-focused products. Tata Consumer Products Ltd (TCPL) sits right at the intersection of this shift. Backed by the Tata brand, a strong distribution network, and an expanding portfolio beyond tea and salt, TCPL is steadily transforming itself into a full-fledged, future-ready FMCG company with aspirations far beyond its legacy categories.

But does TATA Consumer Products Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | TATACONSUM |

| Industry/Sector | FMCG/CD/Services |

| CMP | 1153.00 |

| Market Cap (₹ Cr.) | 1,14,095 |

| P/E | 78.48 (Vs Industry P/E of 60.34) |

| 52 W High/Low | 1220.90 / 930.10 |

| EPS (TTM) | 14.87 |

| Dividend Yield | 0.71% |

About TATA Consumer Products Ltd.

Tata Consumer Products Ltd was formed through the merger of Tata Global Beverages and Tata Chemicals’ consumer business, creating a unified FMCG platform under the Tata umbrella. The company operates across beverages, foods, and emerging categories, with leadership positions in tea and salt, and a growing presence in packaged foods, health, and ready-to-consume segments. TCPL leverages Tata’s brand trust, innovation capabilities, and distribution scale to drive long-term growth.

Key business segments

TATA Consumer Products Ltd. operates primarily in the following key business segments:

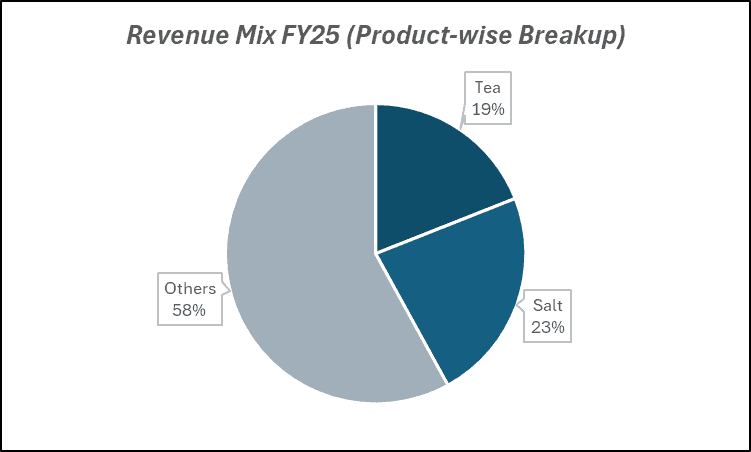

- Beverages: Branded tea and coffee portfolio including Tata Tea, Tetley, and Tata Coffee.

- Foods & Staples: Salt, spices, pulses, ready-to-cook and packaged food offerings under Tata Salt and Tata Sampann.

- NourishCo & RTD: Ready-to-drink beverages and hydration products.

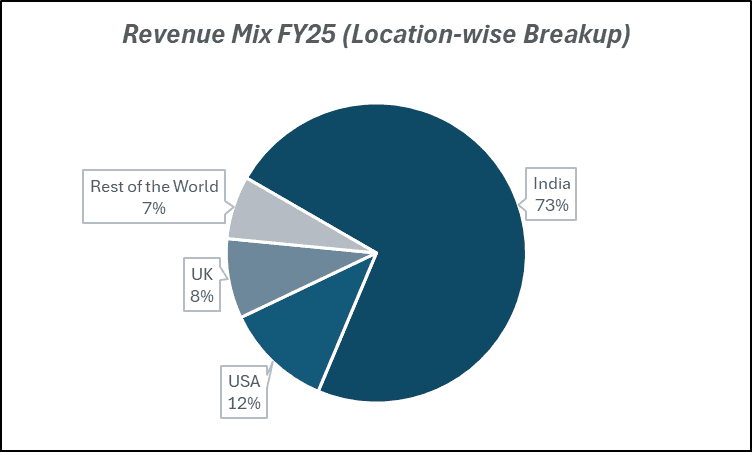

- International Business: Global tea and coffee operations, especially in the UK, US, and Canada.

- New-Age Categories: Health, wellness, and premium nutrition-focused products.

Primary growth factors for TATA Consumer Products Ltd.

TATA Consumer Products Ltd. key growth drivers:

- Premiumisation: Shift from commoditised staples to premium, value-added food and beverage products.

- New Product Launches: Strong pipeline in spices, pulses, ready foods, and wellness categories.

- Distribution Expansion: Deeper rural reach and stronger modern trade and e-commerce presence.

- Brand Trust: Tata brand equity supporting faster acceptance in newer categories.

- International Recovery: Improving performance in global beverage markets.

Detailed competition analysis for TATA Consumer Products Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| TATA Consumer Products Ltd. | 19465.03 | 2620.34 | 13.46% | 1553.35 | 7.98% | 78.48 |

| EID Parry Ltd. | 35879.59 | 3235.19 | 9.02% | 2210.80 | 6.16% | 7.57 |

| CCL Products Ltd. | 4068.78 | 704.40 | 17.31% | 375.44 | 9.23% | 36.32 |

| Balrampur Chini Mills Ltd. | 6170.84 | 821.74 | 13.32% | 410.39 | 6.65% | 22.57 |

| Triveni Engineering Ltd. | 7712.48 | 578.55 | 7.50% | 289.34 | 3.75% | 28.90 |

Key insights on TATA Consumer Products Ltd.

- Category Leadership: Dominant positions in tea and salt provide stable cash flows.

- Margin Upside: Mix improvement and operating leverage from scale and premium products.

- Portfolio Diversification: Reduced dependence on tea through foods and wellness expansion.

- Innovation-Led Growth: Focus on health, immunity, and convenience-led consumption.

- Strong Parentage: Backed by Tata Group’s governance, capital, and ecosystem synergies.

Recent financial performance of TATA Consumer Products Ltd. for Q3 FY26

| Metric | Q3 FY25 | Q2 FY26 | Q3 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 4443.56 | 4965.90 | 5112.00 | 2.94% | 15.04% |

| EBITDA (₹ Cr.) | 564.73 | 671.78 | 720.67 | 7.28% | 27.61% |

| EBITDA Margin (%) | 12.71% | 13.53% | 14.10% | 57 bps | 139 bps |

| PAT (₹ Cr.) | 299.75 | 397.05 | 402.79 | 1.45% | 34.38% |

| PAT Margin (%) | 6.75% | 8.00% | 7.88% | -12 bps | 113 bps |

| Adjusted EPS (₹) | 2.82 | 4.09 | 3.89 | -4.89% | 37.94% |

TATA Consumer Products Ltd. financial update (Q3 FY26)

Financial performance

- Revenue up 15% YoY to ₹5,112 Cr, led by 15% volume growth in India branded business.

- EBITDA grew 27.6% YoY; margins expanded 139 bps to 14.1%.

- Adjusted PAT increased 34.4% YoY to ₹403 Cr.

- Gross margins improved 170 bps YoY to 42.8% on lower tea prices.

- 9MFY26 revenue up 14.2% YoY; EBITDA up 7.6% YoY despite international margin pressure.

Business highlights

- India Foods is strong at ~20% YoY; Tata Sampann up 45% YoY.

- Growth portfolio (~30% mix) delivered 29% YoY growth.

- RTD beverages grew 26% YoY; scaling ahead of the summer season.

- International revenue up 18% YoY; margins to normalize over 1–2 quarters.

- GTM restructuring ~82% complete to accelerate premium brands.

Outlook

- Double-digit revenue growth outlook sustained.

- EBITDA margins guided at 14–15% near term; 15%+ medium term.

- Growth businesses expected to maintain ~30% growth trajectory.

- Healthy cash flows and declining leverage support earnings visibility.

Recent Updates on TATA Consumer Products Ltd.

- New Product Launches: Expansion in spices, pulses, and ready-to-eat categories under Tata Sampann.

- E-commerce Push: Increased focus on direct-to-consumer and online-first product launches.

- Sustainability Initiatives: Packaging reduction, recyclable materials, and responsible sourcing.

- Retail Partnerships: Strengthening presence in modern trade and quick-commerce platforms.

- Brand Investments: Higher spends on brand building to support long-term category expansion.

Company valuation insights – TATA Consumer Products Ltd.

Tata Consumer Products (TCPL) is currently trading at a TTM P/E of 78.5x, at a premium to the industry average of 60.3x. Over the last one year, the stock has delivered a 12.2% return, marginally outperforming the NIFTY 50’s 10.9% gain.

While the headline valuation appears optically elevated, the premium reflects TCPL’s ongoing portfolio transformation, strong growth visibility in high-margin categories, and improving profitability trajectory.

The investment case for TCPL is anchored in its structural shift from a commodity-led tea business to a diversified, higher-margin food and beverage portfolio. The company delivered 15% YoY revenue growth in Q3FY26, supported by strong volume expansion in India branded business and ~29% growth in its high-margin “growth businesses” such as Tata Sampann, RTD beverages, and recent acquisitions.

Gross margins expanded 170 bps YoY to 42.8%, while EBITDA margins improved to 14.1%, with management guiding toward 15%+ margins over the medium term driven by premiumisation, operating leverage, and normalization of international margins.

The ongoing go-to-market restructuring, innovation intensity, and scaling of margin-accretive businesses provide strong earnings visibility. Additionally, improving cash flows and a declining leverage profile enhance financial flexibility to support brand investments and future growth.

From a valuation standpoint, applying a 62x multiple to FY27E EPS of ₹23, we arrive at a 12-month target price of ₹1,425, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹1,220, indicating a 6% upside, supported by sustained double-digit revenue growth, margin expansion trajectory, and continued momentum in growth categories.

Major risk factors affecting TATA Consumer Products Ltd.

- Commodity Price Volatility: Tea, coffee, and agri-input prices can impact margins.

- Execution Risk: Scaling new food categories requires sustained brand and distribution investment.

- Competitive Intensity: Strong competition from established FMCG players in foods and spices.

- International Exposure: Currency and demand fluctuations in global markets.

- Margin Pressure: Near-term profitability may be impacted by investments in growth.

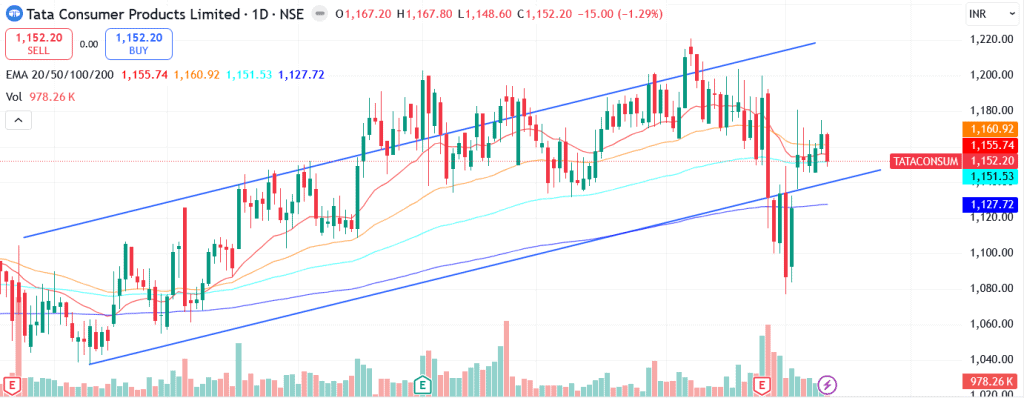

Technical analysis of TATA Consumer Products Ltd. share

Tata Consumer Products (TCPL) is currently trading within an upward trending channel, with prices positioned near the lower trendline of the structure. This placement offers a favourable risk–reward setup, as the stock is attempting to rebound from dynamic support within a broader bullish framework.

Importantly, the stock is trading above its 20-, 50-, 100- and 200-day EMAs, indicating that the primary trend remains structurally positive across timeframes. The alignment of moving averages suggests underlying strength, with dips likely to attract buying interest as long as price sustains above these key levels.

Momentum indicators present a mixed but improving picture. MACD at -5.91 remains in negative territory but has crossed above the signal line, signalling an early bullish momentum shift.

RSI at 48.63 reflects neutral positioning with adequate room for upside, indicating decent buying potential without being overbought. Relative RSI at -0.03 (21-day) and -0.02 (55-day) suggests broadly market-aligned performance, with no significant underperformance risk building.

ADX at 14.13 indicates a range-bound environment, implying that while the broader trend is upward, directional strength is yet to accelerate meaningfully.

A decisive move above ₹1,220 could trigger fresh momentum and open the path towards ₹1,425 (12-month fundamental target). On the downside, ₹1,080 remains a key support zone; sustaining above this level preserves the bullish channel structure and limits downside risk.

- RSI: 48.63 (Neutral; room for upside)

- ADX: 14.13 (Range-bound structure)

- MACD: -5.91 (Bullish crossover; early upside signal)

- Resistance: ₹1,220

- Support: ₹1,080

TATA Consumer Products Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹1,220 (6% upside) and a 12-month target of ₹1,425 (24% upside), based on 62x FY27E EPS of ₹23.

Why buy now?

Structural shift from commodity tea to high-margin food & beverage portfolio.

~30% growth in premium “growth businesses” driving revenue acceleration.

Margin expansion tailwinds from premiumisation and operating leverage.

Strong brand equity and improving distribution via GTM restructuring.

Healthy cash flows and declining leverage supporting sustainable growth.

Portfolio fit

Tata Consumer Products offers exposure to India’s premiumisation and branded consumption theme, combining defensive cash flows with structural growth from high-margin food and beverage categories. With improving margins, strong execution, and scalable growth platforms, the stock fits well in portfolios seeking steady compounders, consumer-driven earnings visibility, and diversification alongside cyclical or thematic allocations.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebTATA Consumer Products Ltd.: Budget 2026-27 opportunities

- Rural Consumption Push: Higher rural spending and income support schemes to boost FMCG and packaged food demand.

- Food Processing Incentives: Continued PLI and infrastructure support for value-added foods and branded staples.

- Agri Supply Chain Investments: Cold-chain and logistics upgrades aiding margin stability and premium product scale-up.

- Inflation Management Measures: Policy focus on commodity price stability benefiting gross margins (tea, edible oils).

- Formalisation & GST Compliance: Shift toward organised branded players supporting market share gains for established brands.

Final thoughts

Tata Consumer Products is in the midst of a structural transformation, from a tea-and-salt company to a diversified, innovation-led FMCG platform. With category leadership providing stability, and new-age foods and wellness products driving growth, TCPL offers investors exposure to India’s evolving consumption patterns. Backed by Tata’s brand trust and long-term vision, the company is well-positioned to compound steadily as it builds the next chapter of India’s FMCG growth story.