What a Synthetic Short Call Means

A synthetic short call is an options strategy that replicates the payoff profile of a short call option without actually selling a call. It is constructed by combining a short put option with a short position in the underlying stock or futures contract. Together, these two positions produce a combined payoff that mirrors what a trader would experience if they had simply sold a call at the same strike price.

The logic behind this comes from put-call parity, a foundational principle in derivatives trading that defines the mathematical relationship between calls, puts, and the underlying asset. Put-call parity states that a call option, a put option, and the underlying asset are connected in a way that allows any one of them to be replicated using the other two. The synthetic short call is a direct application of this principle and sits within the broader category of synthetic call strategy structures used in advanced options trading. In practical terms:

Short Stock + Short Put = Synthetic Short Call

Each leg of this position contributes to an overall profile where profits are capped on the downside and losses are theoretically unlimited on the upside which is exactly how a short call behaves.

How the Strategy Is Created

Building a synthetic short call in options trading involves two simultaneous actions:

Leg 1 — Short the Underlying Stock or Futures: The trader takes a short position in the underlying asset, borrowing and selling shares with the expectation that the price will fall or remain flat.

Leg 2 — Sell a Put Option: At the same time, the trader sells a put option on the same underlying asset, typically at the same strike price that would be used if selling an actual call.

The short put generates premium income upfront. The short stock position profits when the price falls. Together, the combination produces a payoff that is economically identical to selling a call option. The strike price of the put determines the equivalent call strike in the synthetic position.

It’s worth noting that in practice, this strategy is more commonly encountered in theoretical options frameworks and institutional derivatives trading than in retail options strategies. Understanding it, however, sharpens the trader’s grasp of how options pricing and synthetic equivalence work in real markets.

Payoff Structure Explained

Understanding the payoff is central to grasping why this qualifies as a synthetic short call.

- When the stock price falls below the strike at expiration

The short stock position generates profit as price declines. The short put expires worthless, and the premium collected is retained in full. This mirrors a short call expiring out of the money, the position wins, and the premium is the bonus on top.

- When the stock price stays near the strike

The short put expires worthless or close to it. The short stock position shows minimal movement. The premium from the short put is the primary contributor to profit exactly how a short call behaves when the market goes nowhere.

- When the stock price rises sharply above the strike

This is where the position turns painful. The short stock generates mounting losses with every point the stock climbs and there is no ceiling on how high a stock can go. The short put expires worthless, contributing nothing to offset those losses. This is the mirror of a short call’s worst-case scenario: unlimited loss potential on a strong upward move.

The result is an asymmetric payoff profile: modest, capped profit when the trade works, and theoretically unlimited loss when it doesn’t.

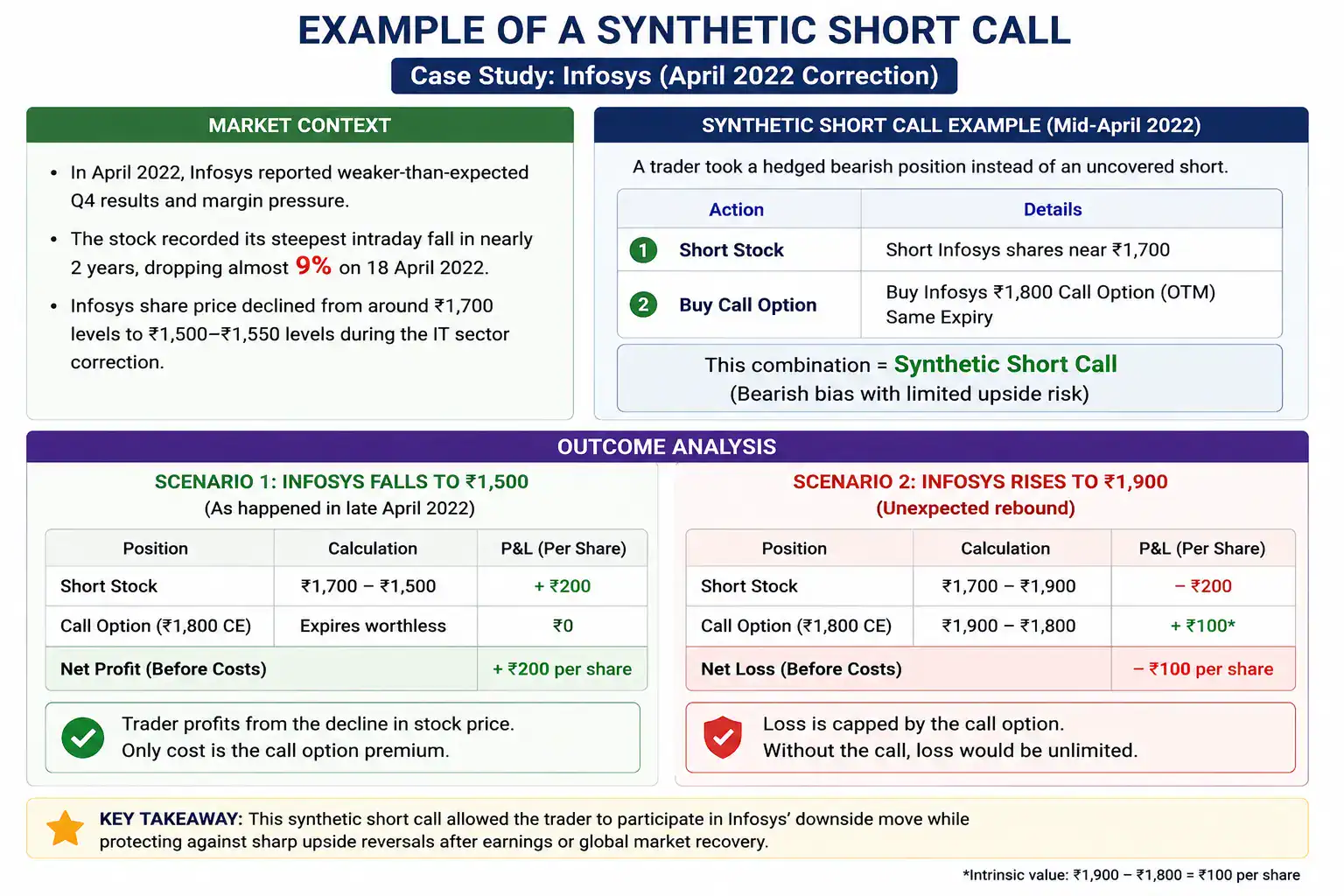

Example of a Synthetic Short Call

A real market options trading example of synthetic short call-style positioning emerged during the sharp Infosys correction in April 2022. After the company reported weaker-than-expected quarterly numbers and margin pressure, Infosys shares recorded their steepest intraday fall in nearly two years, dropping almost 9% in a single session.

During this phase, several derivatives traders adopted hedged bearish positions instead of taking completely uncovered short exposure. One common structure involved shorting Infosys shares while simultaneously purchasing out-of-the-money call options as protection against sudden upside reversals.

For example, a trader shorting Infosys near ₹1,700 while buying a ₹1,800 call option could participate in the downside as the stock later slipped toward ₹1,500–₹1,550 levels during the broader IT sector correction. At the same time, the purchased call helped cap losses if the stock unexpectedly rebounded after earnings commentary or global market recovery.

This became a practical Indian-market case study of how synthetic bearish positions can help traders manage directional exposure during sharp earnings-driven declines while avoiding unlimited upside risk.

Why Traders Use This Strategy

Traders reach for the synthetic short call in specific circumstances where directly selling a call is impractical, restricted, or less efficient.

- Regulatory or access constraints: In some markets or accounts, selling naked calls is restricted due to margin requirements or broker-level rules. Constructing the equivalent synthetic position using a short stock and short put may be more accessible.

- Options hedging purposes: A trader who already holds a short stock position and wants to enhance yield from that position can sell a put to create the synthetic short call profile earning premium while maintaining the short exposure.

- Arbitrage opportunities: When put-call parity temporarily breaks down and the synthetic short call can be constructed more cheaply than selling the actual call, arbitrageurs step in to capture the pricing discrepancy.

- Expressing a neutral-to-bearish view: The strategy suits traders who expect the underlying to stay flat or decline modestly not surge upward and want to collect premium income from that thesis.

Advantages of Synthetic Short Call

The synthetic short call offers more than just an alternative route to the same payoff in the right manner, it brings specific structural and strategic benefits to a trader’s toolkit, which include:

- Equivalent economics to short call: For traders who cannot directly sell a naked call, the synthetic version achieves the same economic outcome using positions that may be more accessible within their trading framework.

- Deep understanding of pricing relationships: Traders who work with synthetic positions develop a more sophisticated grasp of how options are priced and how put-call parity functions in live markets, a skill that enhances decision-making across all derivatives trading activity.

- Flexibility in construction: Traders who already have a short stock position can add the short put to synthetically replicate a short call without opening an entirely separate options position making it a capital-efficient options hedging strategy in the right context.

- Exploiting put-call parity mispricing: When options markets are temporarily inefficient such as during high volatility events like earnings or macro announcements the synthetic short call can be constructed more cheaply than selling the actual call directly. Traders who spot this discrepancy can lock in a better net premium for the same economic exposure.

Risks and Limitations

The options risk profile of a synthetic short call is one of the most unforgiving in derivatives trading, and it must be approached with that awareness.

- Unlimited upside risk: Just like a short call, losses are theoretically unlimited if the underlying price rises sharply and without bound. There is no natural ceiling on how much a short stock position can lose.

- Margin requirements: Both the short stock position and the short put require margin. Combined margin obligations can be substantially higher than simply selling a call outright, making this a capital-intensive strategy.

- Not suitable for bullish markets: In strong uptrending markets, this strategy suffers on both legs simultaneously, the short stock loses money and the short put may also move against the trader if the price rises significantly above the strike.

- Complexity of management: Managing two separate positions, a short stock and a short put requires active monitoring. If one leg needs to be adjusted due to price movement, the synthetic equivalence can break down.

Synthetic Short Call vs Actual Short Call

The key differences between a synthetic short call and an actual short call are as follows:

| Factor | Synthetic short call | Actual short call |

| Meaning | A bearish position created by short-selling a stock and buying a call option | A bearish position created by directly selling a call option |

| How it is created | Short stock + long call option | Sell call option only |

| Maximum profit | Profit comes from a fall in the stock price | Limited to the premium received from selling the call |

| Maximum loss | Limited because the bought call controls upside risk | Unlimited if the stock price keeps rising |

| Risk level | Lower because the call option acts as protection | Higher because there is no built-in hedge |

| Capital requirement | Higher due to stock shorting and option purchase | Lower compared to synthetic setup |

| Margin requirement | Usually high because of the short stock position | Can rise sharply if the stock moves upward |

| Protection against sudden rise | Yes, the long call limits losses above the strike price | No automatic protection against sharp rallies |

| Complexity | More complex because two positions must be managed | Simpler because only one option is sold |

| Usage | Traders want bearish exposure with controlled risk | Traders expect the stock to stay below the strike price |

Final Takeaway for Traders

Understanding the synthetic short call goes beyond learning one more strategy, it rewires how a trader thinks about options pricing, synthetic equivalence, and position construction. Few retail traders ever explore this territory, which is precisely why those who do gain a meaningful edge. In derivatives trading, knowing that every payoff can be replicated multiple ways transforms how you read markets and manage risk.

FAQs

Traders use it when naked call selling is restricted, when an existing short stock position needs premium enhancement, or when a pricing gap makes the synthetic construction cheaper than selling the call directly.

Yes, significantly. Buying a call caps your loss at the premium paid. A synthetic short call carries unlimited loss potential if the stock rallies sharply against the position.

Experienced traders and institutional participants with active margin management capabilities, strong derivatives trading knowledge, and a clear neutral-to-bearish view on the stock they’re positioning against.

The synthetic long call built using a long stock position combined with a long put replicates buying a call, offering unlimited upside with a defined maximum loss.

Rarely in retail trading. It appears more in institutional derivatives desks, options arbitrage, and academic pricing frameworks where synthetic equivalence is actively exploited.