India’s banking sector offers a wide spectrum of business models, from large universal banks to niche lenders focused on financial inclusion. Among these, microfinance-led banks have carved a unique space by serving underserved segments and driving grassroots credit growth.

Bandhan Bank Ltd. stands out as one of the most prominent players in this segment, having evolved from a microfinance institution into a full-fledged bank. With deep rural penetration and strong liability franchise expansion underway, the bank is at a critical turning point.

But does Bandhan Bank Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | BANDHANBNK |

| Industry/Sector | Financial Services |

| CMP | 178.00 |

| Market Cap (₹ Cr.) | 28,675 |

| P/B | 1.19 |

| 52 W High/Low | 192.48 / 160.79 |

| EPS (TTM) | 6.25 |

| Dividend Yield | 0.82% |

About Bandhan Bank Ltd.

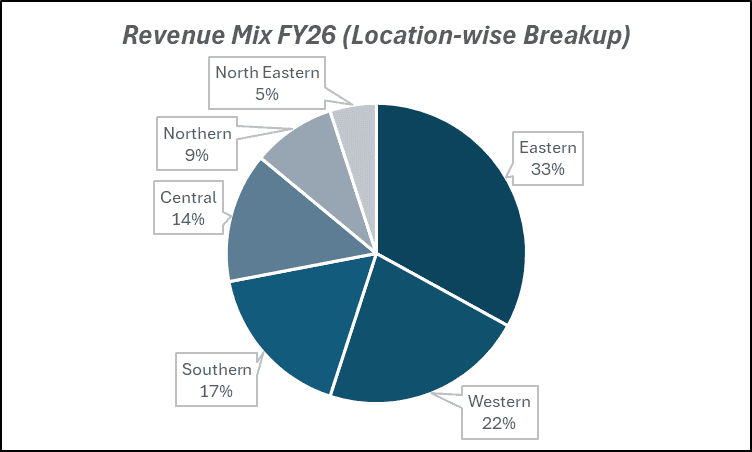

Bandhan Bank Limited is a private sector bank that began as a microfinance institution and transitioned into a universal bank. Headquartered in Kolkata, the bank has a strong presence in eastern and northeastern India, with a focus on underserved and unbanked populations.

Bandhan Bank primarily lends to microfinance borrowers, small businesses, and retail customers, while gradually expanding its deposit base and product offerings to build a more diversified banking model.

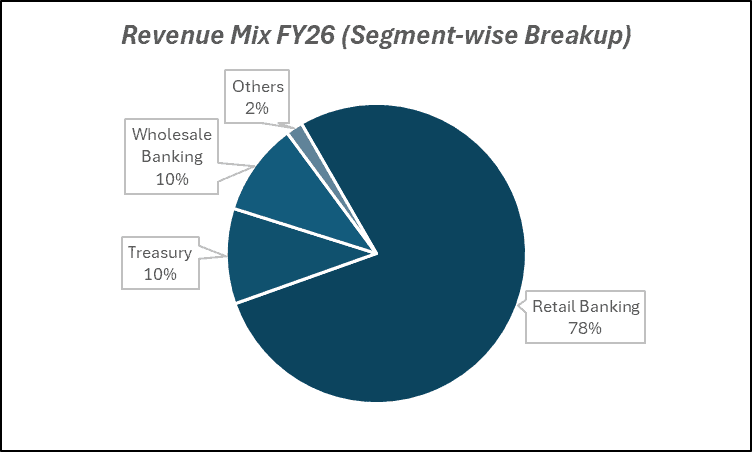

Key business segments

Bandhan Bank Ltd. operates primarily in the following key business segments:

- Microfinance Lending: Group-based loans to women borrowers in rural and semi-urban areas.

- Retail Banking: Housing loans, gold loans, personal loans, and deposits.

- SME & MSME Lending: Loans to small businesses and entrepreneurs.

- Treasury Operations: Investment in government securities and money markets.

- Digital & Branch Banking: Expanding digital and physical banking presence.

Primary growth factors for Bandhan Bank Ltd.

Bandhan Bank Ltd. key growth drivers:

- Financial Inclusion Growth: Expanding access to credit in underserved regions.

- Portfolio Diversification: Increasing share of retail and SME loans beyond microfinance.

- Deposit Franchise Expansion: Growth in CASA improving funding profile.

- Credit Demand in Rural India: Rising economic activity in semi-urban and rural markets.

- Operating Leverage: Improved profitability as scale increases.

Detailed competition analysis for Bandhan Bank Ltd.

Key financial metrics – TTM;

| Company | NII (₹ Cr.) | NII Growth (%) | Operating Income (₹ Cr.) | PAT (₹ Cr.) | PAT Margin (%) | P/B |

| Bandhan Bank Ltd. | 10829.69 | -5.75% | 5864.92 | 1223.56 | 5.01% | 1.19 |

| City Union Bank Ltd. | 2829.83 | 22.20% | 2014.23 | 1326.23 | 16.77% | 2.03 |

| RBL Bank Ltd. | 6362.09 | -1.59% | 3365.61 | 879.05 | 4.76% | 1.17 |

| Karur Vysya Bank Ltd. | 4669.04 | 12.00% | 3663.19 | 2298.73 | 18.15% | 2.25 |

| IDFC First Bank Ltd. | 21215.77 | 9.96% | 7185.54 | 1610.56 | 3.33% | 1.28 |

Key insights on Bandhan Bank Ltd.

- Strong legacy and leadership in microfinance lending.

- High-yield loan portfolio supporting margins.

- Transitioning toward a more diversified loan book.

- Improving liability profile with growing deposits.

- Asset quality remains a key monitorable.

Recent financial performance of Bandhan Bank Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| NII (₹ Cr.) | 2755.90 | 2688.30 | 2795.59 | 3.99% | 1.44% |

| NII Growth YoY (%) | -3.62% | -4.48% | 1.44% | 592 bps | 506 bps |

| Operating Income (₹ Cr.) | 1571.34 | 1445.00 | 1441.16 | -0.27% | -8.28% |

| PAT (₹ Cr.) | 317.90 | 205.59 | 534.14 | 159.81% | 68.02% |

| PAT Margin (%) | 5.18% | 3.36% | 8.62% | 526 bps | 344 bps |

| GNPA (%) | 4.71% | 3.33% | 3.27% | -6 bps | -144 bps |

| NNPA (%) | 1.28% | 0.99% | 0.97% | -2 bps | -31 bps |

Bandhan Bank Ltd. financial update (Q4 FY26)

Financial performance

- NII grew marginally by 1.4% YoY to ₹2,796 Cr, indicating stable core income growth.

- PAT increased sharply by 68% YoY to ₹534 Cr, driven by lower provisions and improving asset quality.

- Net revenue stood at ₹3,567 Cr (+3.2% YoY), reflecting modest topline growth.

- NIM improved to 6.2%, supported by better cost of funds and improved portfolio mix.

- Asset quality strengthened with GNPA/NNPA at 3.3% / 1.0%, reflecting better collections and lower stress.

Business highlights

- The advances growth remained healthy, led by continued strength in microfinance and gradual diversification into retail segments.

- Deposits saw stable traction, though CASA moderated to 27%, indicating reliance on term deposits for growth.

- Microfinance continues to dominate the portfolio, but share is gradually declining with focus on secured lending.

- Retail segments (housing, personal loans, and MSME) are scaling up, improving risk diversification.

- Cost efficiency improved with strong income growth, aiding operating profitability despite elevated investments.

Outlook

- Credit growth expected to remain strong in mid-to-high teens, driven by microfinance stability and retail expansion.

- NIMs are likely to normalize but remain elevated (7.5–8%), supported by portfolio mix and pricing discipline.

- Asset quality outlook remains positive, with controlled slippages and improving collection efficiency.

- Earnings expected to grow at 18–20% CAGR over FY26–28, driven by normalization in credit costs and steady growth.

- RoA/RoE expected to improve to 1.8% / 16–18%, reflecting improving profitability and operating efficiency.

Recent Updates on Bandhan Bank Ltd.

- Continued focus on reducing microfinance concentration.

- Expansion of retail and MSME loan segments.

- Strengthening risk management and underwriting practices.

- Improving collection efficiency and asset quality.

- Branch network expansion in key regions.

Company valuation insights – Bandhan Bank Ltd.

Bandhan Bank is currently trading at 1.19x its book value, delivering a 8.4% return over the last one year, outperforming the NIFTY 50 which declined 1.4% during the same period.

The investment case for Bandhan Bank is anchored in its strong microfinance franchise, which continues to provide high-yield growth, along with a gradual shift towards a more diversified and secured loan mix. The bank has been focusing on expanding its presence in retail and MSME lending, reducing concentration risks inherent in the microfinance segment. Asset quality trends have shown meaningful improvement, supported by better collection efficiencies, declining stress in legacy portfolios, and tighter underwriting standards. On the liability side, the bank continues to strengthen its deposit franchise, with a focus on granular retail deposits to improve funding stability. Margins remain healthy due to the high-yield nature of its core portfolio, while normalization in credit costs is aiding earnings recovery. With improving operational efficiency, a more balanced loan book, and a stronger risk framework, Bandhan Bank is well positioned to benefit from the ongoing credit cycle and deliver steady earnings growth over the medium term.

From a valuation perspective, applying a 1.1x FY28E book value, we derive a 12-month target price of ₹220, implying an upside potential of 24% from current levels. Over the near term, we assign a 3-month target price of ₹190, indicating a 6% upside, supported by improving asset quality, stable margins, and continued traction in portfolio diversification.

Major risk factors affecting Bandhan Bank Ltd.

- Asset Quality Risk: Microfinance portfolio vulnerable to economic stress.

- Concentration Risk: High dependence on microfinance segment.

- Regulatory Risk: Changes in microfinance lending norms.

- Geographic Risk: High exposure to eastern India.

- Collection Efficiency Risk: Sensitivity to borrower repayment behavior.

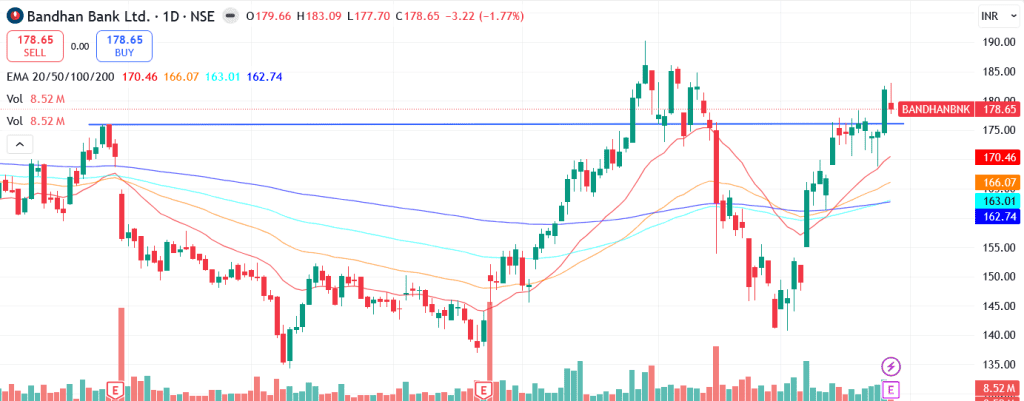

Technical analysis of Bandhan Bank Ltd. share

Bandhan Bank has shown a strong technical recovery, breaking out of a cup and handle formation, which is typically considered a bullish continuation pattern. The breakout indicates a shift in sentiment, with renewed buying interest and potential for sustained upside. The stock is now trading firmly above all its key moving averages (20, 50, 100, and 200-day EMAs), signaling strength across short, medium, and long-term timeframes and confirming a well-established uptrend.

Momentum indicators remain highly supportive of the ongoing move. The MACD at 4.38 is in positive territory and above the signal line, indicating sustained bullish momentum. The RSI at 60.92 reflects strong buying interest without entering overbought territory, suggesting room for further upside. Additionally, the Relative RSI over 21 and 55 days at 0.14 and 0.24 respectively indicates consistent outperformance versus broader benchmarks. The ADX at 18.60 suggests that the trend is strengthening, supporting the continuation of the current uptrend.

A sustained move above ₹190 could trigger further upside towards ₹220, aligning with our 12-month fundamental target. On the downside, ₹165 acts as a strong support level, below which the bullish structure may weaken.

- RSI: 60.92 (Good buying interest)

- ADX: 18.60 (Trend strengthening)

- MACD: 4.38 (Positive; above signal)

- Resistance: ₹190

- Support: ₹165

Bandhan Bank Ltd. stock recommendation

Current Stance: Buy, with a 3-month target of ₹190 (6% upside) and a 12-month target of ₹220 (24% upside), based on 1.1x FY28E book value.

Why buy now?

Strong earnings recovery underway, supported by normalization in credit costs and improving profitability.

Improving asset quality, with declining GNPA/NNPA and better collection efficiency across key segments.

High-yielding microfinance franchises continue to support margins, while diversification into retail and MSME reduces concentration risk.

Gradual strengthening of the liability franchise, with focus on granular deposits to improve funding stability.

Improving return ratios, with RoA/RoE expected to trend upwards as asset quality stabilizes and growth normalizes.

Portfolio fit

Bandhan Bank offers exposure to India’s underpenetrated rural and semi-urban credit markets through its strong microfinance franchise, while its ongoing transition towards a more diversified and secured loan book improves the overall risk profile. With improving asset quality, stable margins, and a clear strategy to scale retail and MSME lending, the bank is well positioned to benefit from the credit upcycle. Supported by a strengthening liability base and better operating efficiency, the stock fits well in portfolios seeking turnaround opportunities within the BFSI space with favorable risk-reward.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebBandhan Bank Ltd.: Budget 2026-27 opportunities

- Financial Inclusion Schemes: Increased credit penetration in rural and semi-urban areas.

- MSME Support Programs: Boost in lending opportunities for small businesses.

- Digital Banking Initiatives: Expansion of digital financial services.

- Rural Development Spending: Increased income levels supporting credit demand.

- Priority Sector Lending Push: Favorable environment for microfinance-focused banks.

Final thoughts

Bandhan Bank Limited stands at an important inflection point, balancing its strong microfinance legacy with efforts to build a more diversified banking model. With improving asset quality, expanding retail presence, and strong growth potential in underserved markets, the bank is well positioned for a gradual turnaround.

For investors seeking exposure to high-growth banking with turnaround potential, Bandhan Bank offers a blend of yield-driven lending, financial inclusion tailwinds, and long-term scalability.