India’s manufacturing growth story extends far beyond final assembly. The real opportunity lies in the vast ecosystem of original equipment manufacturing (OEM), electronics manufacturing services (EMS), and critical sub-systems that power everything from consumer appliances and automobiles to advanced railway infrastructure.

As domestic consumption accelerates, government focus on local electronics manufacturing intensifies, and railway modernization gathers pace, integrated B2B solution providers are capturing immense value. In this backdrop, Amber Enterprises India Ltd. has emerged as the undisputed market leader in the room air conditioner (RAC) OEM space, with a rapidly growing footprint in electronics, PCBs, and railway mobility.

But does Amber Enterprises India Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | AMBER |

| Industry/Sector | Consumer Durables |

| CMP | 7585.00 |

| Market Cap (₹ Cr.) | 26,751 |

| P/E | 118.60 (Vs Industry P/E of 52.95) |

| 52 W High/Low | 8974.00 / 5400.50 |

| EPS (TTM) | 64.21 |

| Dividend Yield | 0.00% |

About Amber Enterprises India Ltd.

Amber Enterprises India Limited is one of India’s leading manufacturers of room air conditioners, cooling components, and electronic products. The company operates primarily as a key Original Equipment Manufacturer (OEM) and Original Design Manufacturer (ODM) and has established a strong presence across consumer durables, electronics, industrial, and railway infrastructure segments.

Over the years, Amber Enterprises has evolved from a room air conditioner manufacturer into a broader electronics manufacturing services (EMS) and HVAC company with offerings that include printed circuit board assemblies (PCBAs), electric motors, heat exchangers, and railway mobility cooling solutions. The company has a significant domestic manufacturing footprint, operating 30 facilities across India, and an expanding international export presence.

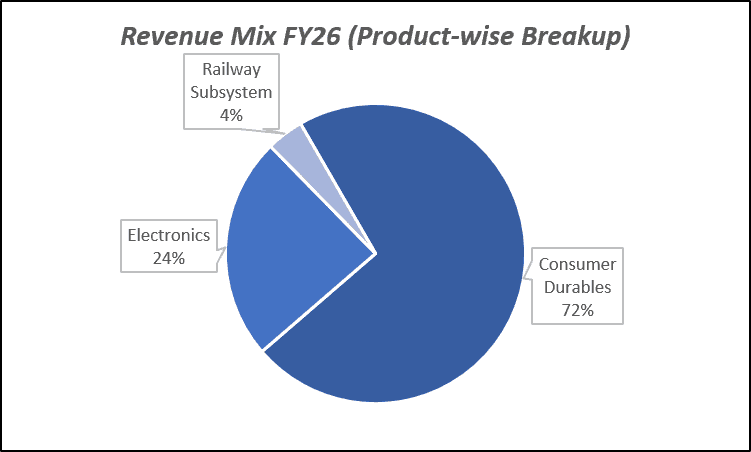

Key business segments

Amber Enterprises India Ltd. operates primarily in the following key business segments:

- Consumer Durables (RACs): Split, window, and inverter air conditioners, alongside critical components like motors and copper tubes.

- Electronics (EMS): Printed Circuit Board Assemblies (PCBAs), bare PCBs, and solutions for telecom, automotive, and smart energy meters.

- Railway Subsystems: HVAC systems, doors, gangways, and pantry systems for Indian Railways, metros, and RRTS.

- Non-RAC Components: Injection molding and sheet metal components for refrigerators, washing machines, and microwaves.

- Defence Solutions: Customised cooling, HVAC, and integrated subsystem solutions for defence applications.

Primary growth factors for Amber Enterprises India Ltd.

Amber Enterprises India Ltd. key growth drivers:

- Underpenetrated RAC Market: Rising temperatures and increasing affordability driving room air conditioner demand.

- Favourable Government Policies: Beneficiary of PLI schemes and import substitution initiatives promoting domestic manufacturing.

- Expansion of Electronics Business (EMS): Growing contribution from higher-margin printed circuit board assemblies and smart meters.

- Railway & Mobility Infrastructure: Surging demand and robust order book from railway, metro, and defence projects.

- Backward Integration & Components: Enhancing profitability through in-house manufacturing of critical components like compressors and motors.

Detailed competition analysis for Amber Enterprises India Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| Amber Enterprises India Ltd. | 12186.48 | 952.32 | 7.81% | 316.49 | 2.60% | 118.60 |

| Voltas Ltd. | 14244.50 | 646.90 | 4.54% | 500.57 | 3.51% | 114.85 |

| Blue Star Ltd. | 12401.99 | 930.40 | 7.50% | 526.77 | 4.25% | 62.32 |

| Bosch Home Comfort India Ltd. | 2698.69 | 67.49 | 2.50% | -2.86 | -0.11% | – |

| EPACK Durable Ltd. | 1894.45 | 113.92 | 6.01% | 9.71 | 0.51% | 691.32 |

Key insights on Amber Enterprises India Ltd.

- Among India’s leading OEM/ODM players for room air conditioners and components.

- Robust manufacturing network with strategically located facilities across the country.

- Beneficiary of rising domestic consumption, PLI schemes, and railway infrastructure modernization.

- Growing Electronics Manufacturing Services (EMS) division enhancing profitability and scale.

- Diversified revenue streams across consumer durables, mobility applications, and defense solutions.

- Increasing focus on exports and global supply chain integration supporting long-term growth.

- Focus on backward integration, continuous R&D, and strategic acquisitions.

Recent financial performance of Amber Enterprises India Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 3753.70 | 2942.82 | 4147.52 | 40.94% | 10.49% |

| EBITDA (₹ Cr.) | 294.76 | 246.10 | 358.23 | 45.56% | 21.53% |

| EBITDA Margin (%) | 7.85% | 8.36% | 8.64% | 28 bps | 79 bps |

| PAT (₹ Cr.) | 131.12 | -0.70 | 228.96 | 32808.57% | 74.62% |

| PAT Margin (%) | 3.49% | -0.02% | 5.52% | 554 bps | 203 bps |

| Adjusted EPS (₹) | 34.32 | -7.75 | 38.04 | 590.84% | 10.84% |

Amber Enterprises India Ltd. financial update (Q4 FY26)

Financial performance

- Revenue grew 22.19% YoY to ₹12,186 crore in FY26, driven by strong demand across the consumer durables and electronics segments.

- EBITDA increased 16.85% YoY to ₹952 crore, supported by a growing scale of operations and expanding EMS business.

- EBITDA margin contracted slightly by 35 bps YoY to 7.81%, reflecting changes in the product mix and operational costs

- PAT declined by 9.96% YoY to ₹316 crore, primarily impacted by higher interest and depreciation expenses during the year.

- Return ratios stood at moderate levels, with ROE at 5.95% and ROCE at 10.2%, indicating ongoing capital investments and capacity building.

Business highlights

- The consumer durables and electronics businesses delivered strong growth, supported by demand across RACs, mobility, and industrial components.

- The electronics division emerged as a key growth engine, alongside a strategic focus on expanding export capabilities.

- Amber strengthened its operational reach through its extensive pan-India network of manufacturing facilities.

- The company continues to focus on backward integration, exports, and higher-margin electronics and railway segments.

Outlook

- Management expects robust volume growth in the RAC and components business, supported by low market penetration and rising summer temperatures.

- The company targets a higher revenue share from its non-RAC and EMS divisions to drive steady margin expansion over the coming years.

- Electronics and railway mobility revenues are expected to outpace core RAC growth, driven by PLI schemes, EV investments, and railway upgrades.

- Expansion into bare PCBs, smart meters, and defense cooling solutions is expected to increase addressable market opportunities and support profitability.

- Long-term growth remains supported by domestic manufacturing initiatives, import substitution, component export opportunities, and backward integration.

Recent Updates on Amber Enterprises India Ltd.

- Continued expansion of the electronics and non-RAC component portfolio.

- Strengthening manufacturing footprint through strategic joint ventures.

- Capacity additions in PCB and motor segments to support growing demand.

- Increased focus on backward integration and higher-margin EMS solutions.

- Expansion of export business across multiple global geographies.

Company valuation insights – Amber Enterprises India Ltd.

Amber Enterprises is currently trading at a TTM P/E of 118.6x and an EV/EBITDA of 27.1x. Despite near-term margin headwinds caused by commodity inflation, the stock reflects strong investor confidence, supported by its market leadership position and a dominant 26-27% market share in the room air-conditioner (RAC) industry

The investment case for Amber Enterprises is supported by its strong position as a leading RAC solution provider, its capability to manufacture 70% of the Bill of Materials (BoM) for RACs, and rising exposure to structural themes such as smart electronics, automotive, telecom, healthcare, and defence. The company continues to successfully diversify its revenue mix, with RAC completely built unit (CBU) contribution declining from 72% in FY18 to 47% in FY26. Its electronics business is expected to grow significantly faster than the overall industry, supported by management’s guidance of 40%+ revenue growth for FY27. Under its diversification strategy, management is targeting robust growth and steady margin expansion back to 8.5% by FY28, driven by key projects like Ascent Circuits (₹990 crore) and Korea Circuits (₹3,290 crore) for PCBs, alongside Sidwal and Yujin Machinery for railways. Additionally, the ongoing ₹1,800 to ₹2,000 crore capex program primarily focused on PCB and railway expansion projects provides multiple levers for sustainable earnings growth. Supported by a strong order book visibility of over ₹2,600 crore in the railways division and growing traction in data center cooling solutions, Amber remains well-positioned to benefit from India’s long-term manufacturing and infrastructure growth story.

From a valuation perspective, valuing the company at 47x P/E on FY28E EPS of ₹200, we arrive at a 12-month target price of ₹9,400, implying an upside potential of 24% from the current market price. Over the near term, we maintain a 3-month target of ₹8,050, representing an upside potential of 6%, with momentum expected to be supported by strong Q1FY27 industry demand driven by severe summer conditions, improving product mix towards double-digit margin electronics, operationalization of new greenfield facilities, and sustained growth across the railway and defense mobility sectors.

Major risk factors affecting Amber Enterprises India Ltd.

- Raw Material Risk: Volatility in commodity prices like copper-clad laminates and gold impacting margins

- Competition Risk: Intense competition from established industry players in the RAC and EMS space.

- Execution Risk: Delays in expanding new PCB and railway projects due to approvals or macro slowdowns.

- Seasonal & Weather Risk: Fluctuations in room air conditioner demand depending heavily on summer weather conditions.

- Policy Risk: Any restraint or adverse changes in government manufacturing support and PLI measures.

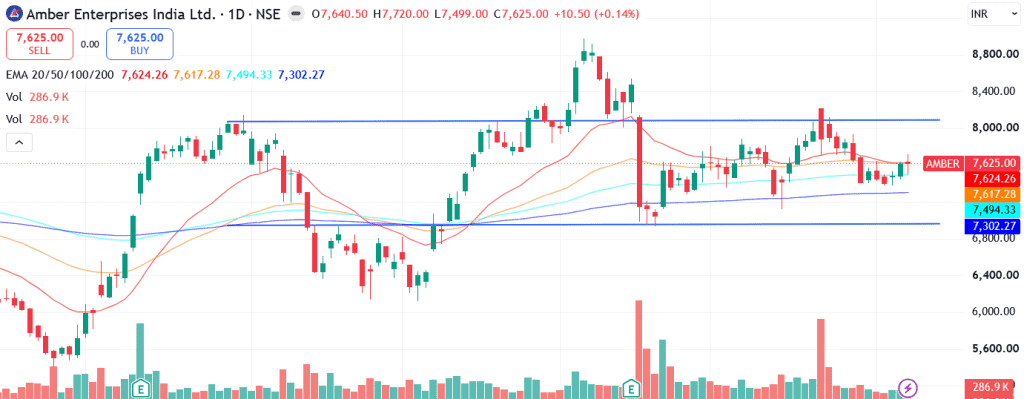

Technical analysis of Amber Enterprises India Ltd. share

Amber Enterprises is currently consolidating within a well-defined sideways channel after a strong prior uptrend, indicating a phase of healthy price absorption. The stock continues to trade above its 20-day, 50-day, 100-day and 200-day EMAs, highlighting that the broader long-term trend remains intact despite the recent consolidation. A decisive breakout above the upper trendline of the channel, near ₹8,050, could act as the next trigger for momentum-led buying and pave the way towards ₹9,400, in line with our 12-month fundamental target.

Momentum indicators suggest that the stock is approaching a favourable technical setup. The MACD at -39.59 remains in negative territory but is on the verge of crossing above its signal line, indicating that bearish momentum is fading and a bullish crossover could provide an attractive entry opportunity. The RSI at 49.61 reflects balanced price action with decent buying interest, leaving ample room for momentum to strengthen if a breakout materialises.

Trend strength remains subdued, with the ADX at 11.52 indicating a range-bound market and the absence of a strong directional trend. However, a breakout above the upper trendline, supported by a positive MACD crossover, could significantly improve trend strength and attract fresh buying interest. On the downside, ₹6,950 remains a key support level and serves as an important stop-loss level for the bullish view.

- RSI: 49.61 (Decent buying interest)

- ADX: 11.52 (Range-bound; crossover and breakout awaited)

- MACD: -39.59 (Negative; crossover awaited)

- Resistance: ₹8,050

- Support: ₹6,950

Amber Enterprises India Ltd. stock recommendation

Current Stance: Buy, with a 3-month target price of ₹8,050 (6% upside) and a 12-month target price of ₹9,400 (24% upside), based on a valuation of 47x FY28E EPS of ₹200.

Why buy now?

Strong demand across consumer durables, smart electronics, automotive, telecom, railways, and data center cooling provides long-term growth visibility for the diversified platform.

The company continues to command market leadership in the room air-conditioner (RAC) industry with a dominant 26-27% market share and ~70% BoM manufacturing capability.

Strategic diversification targets strong 40%+ revenue growth in electronics and margin expansion back to 8.5% by FY28 through higher-margin component business mix.

A planned ₹1,800 to ₹2,000 crore capex programme focused on PCB manufacturing and railway capacity expansion is expected to support future earnings growth.

Growing export opportunities, expansion into advanced HDI PCB solutions, operationalization of new greenfield facilities, and deep client relationships position the company to deliver sustainable earnings growth over the medium to long term.

Portfolio fit

Amber Enterprises provides exposure to India's manufacturing localization, electronic manufacturing services (EMS), and mobility infrastructure growth themes through its strong presence in room air conditioners, components, printed circuit boards, and railway subsystems. Backed by a growing pan-India manufacturing footprint, expanding global export capabilities, increasing share of higher-margin electronics and railway products, aggressive capacity expansion initiatives, and dominant market leadership, the company is well positioned to benefit from rising investments in consumer electronics, automotive components, defense cooling, and railway modernization, making it a suitable addition to growth-oriented portfolios.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebAmber Enterprises India Ltd.: Budget 2026-27 opportunities

- Consumer Durables: Increased demand for residential RACs and home appliances.

- Electronics Push: Stronger government support (like ECMS) accelerating PCB and advanced electronics manufacturing.

- Make in India: Policies promoting domestic value addition, import substitution, and backward integration.

- Capex Expansion: Strong central infrastructure spending supporting large-scale manufacturing capacity additions.

Final thoughts

Amber Enterprises India Ltd. stands at the intersection of several powerful long-term themes : domestic manufacturing localization, electronic manufacturing services (EMS) expansion, railway infrastructure modernization, and rising consumer durable penetration. With a dominant market leadership position, an extensive pan-India manufacturing footprint, a diversified B2B product portfolio, and a rapidly growing presence in advanced electronics and mobility subsystems, the company is well positioned to capitalize on India’s evolving manufacturing ecosystem.

For investors seeking exposure to India’s consumer durables, electronics, and infrastructure growth story through a highly scalable OEM/ODM platform, Amber Enterprises offers a compelling combination of market leadership, structural growth visibility, and long-term compounding potential.