The narrative of India’s maturing automotive and mobility landscape is evolving significantly, moving beyond a mere volume-led demand for basic, mechanical vehicle components. Today, the core opportunity resides in the aggressive electrification and premiumisation of vehicle systems, as modern automakers and consumers increasingly pivot toward intelligent, connected, and advanced safety solutions.

Against a backdrop of surging consumer preference for feature-rich vehicles, a structural industry shift favouring localised technology, and a definitive transition toward high-margin electronics, alloy wheels, and EV-specific systems, value-added component portfolios are rapidly capturing premium value share from conventional auto architectures. Within this high-growth vertical, UNO Minda has established itself as a formidable force in India’s auto ancillary ecosystem, spearheading strategic global joint ventures, aggressive capacity expansion, and a product diversification initiative to drive the modernisation of the country’s next-generation mobility landscape.

But does UNO Minda Ltd. offer a compelling case for long-term investors? Let’s delve deeper.

Stock overview

| Ticker | UNOMINDA |

| Industry/Sector | Auto Ancillary |

| CMP | 1126.00 |

| Market Cap (₹ Cr.) | 65,033 |

| P/E | 51.11 (Vs Industry P/E of 37.21) |

| 52 W High/Low | 1382.00 / 994.00 |

| EPS (TTM) | 20.24 |

| Dividend Yield | 0.23% |

About UNO Minda Ltd.

Operating from its corporate hub in Gurugram, Haryana, the company functions as a structural pillar of the global automotive architecture, securing its leadership as a formidable Tier-1 powerhouse within India’s high-growth smart mobility and advanced component ecosystem. Leveraging a massive manufacturing engine of over 70 state-of-the-art facilities and specialized R&D hubs, the group delivers an unparalleled portfolio of high-performance solutions, ranging from intelligent lighting and advanced switching systems to sophisticated acoustic architectures. Perfectly positioned to capitalize on powerful structural tailwinds, specifically the aggressive transition toward vehicle electrification and accelerating consumer premiumisation, the company anchors a resilient institutional pipeline across two-wheeler networks, passenger vehicle OEMs, and the rapidly evolving electric mobility landscape.

Key business segments

UNO Minda Ltd. operates primarily in the following key business segments:

- Advanced Automotive Lighting: Expanding into specialised LED and intelligent lighting systems to enhance vehicle safety, efficiency, and premiumisation.

- Smart Switching & Controls: Driving innovation through advanced mechatronics and intelligent steering switches for seamless vehicle integration.

- Premium Castings & Alloy Wheels: Strengthening lightweight vehicle platforms with high-quality alloy wheels and precision die-casting solutions.

- EV Infrastructure: Supporting electric mobility through Battery Management Systems (BMS) and telematics for reliable energy management.

- Acoustics & Aftermarket: Expanding OEM and aftermarket presence with acoustic solutions and replacement parts, benefiting from rising vehicle upgrade demand.

Primary growth factors for UNO Minda Ltd.

- Value-Added Growth: Benefiting from the shift towards electric, connected, and safer vehicles supported by stricter emission and safety norms.

- Portfolio Premiumisation: Expanding into high-margin products such as alloy wheels, LED lighting, and ADAS solutions.

- OEM & Ecosystem Strength: Leveraging strong OEM relationships, Tier-1 positioning, and localisation to drive operational efficiency and market share.

- EV Leadership: Strengthening its competitive edge through EV powertrain solutions and the integration of UnoMinda EV Systems.

- Capacity Expansion: Scaling manufacturing through greenfield projects, technology partnerships, and a wider pan-India footprint.

Detailed competition analysis for UNO Minda Ltd.

Key financial metrics – TTM;

| Company | Sales (₹ Cr.) | EBITDA (₹ Cr.) | EBITDA Margin (%) | PAT (₹ Cr.) | PAT Margin (%) | P/E |

| UNO Minda Ltd. | 19657.59 | 2251.23 | 11.45% | 1035.19 | 5.27% | 51.11 |

| Bosch Ltd. | 20034.70 | 2650.40 | 13.23% | 2770.00 | 13.83% | 44.82 |

| Tube Investments of India Ltd. | 22847.43 | 2257.91 | 9.88% | 1116.63 | 4.89% | 52.00 |

| Sona BLW Precision Forgings Ltd. | 4449.46 | 1081.17 | 24.30% | 629.19 | 14.14% | 65.96 |

| Endurance Technologies Ltd. | 14595.88 | 1965.64 | 13.47% | 951.71 | 6.52% | 39.12 |

Key insights on UNO Minda Ltd.

- Tier-1 Market Leadership: Leading in automotive switching, lighting, and alloy wheels with a strong position across OEMs.

- Manufacturing Scale: Expanding capacity through new facilities, including the Maharashtra alloy wheel plant, supported by a strong aftermarket network.

- EV & Safety Tailwinds: Well positioned to benefit from rising EV adoption, lightweight vehicles, and stricter safety regulations.

- Premium Product Mix: Driving margin expansion through LED lighting, IVI systems, ADAS, and other high-value automotive solutions.

- Strong OEM Relationships: Backed by long-standing OEM partnerships and a diversified order pipeline supporting sustainable growth.

- Capacity & EV Expansion: Investing in EV powertrain capabilities and strategic joint ventures to strengthen future growth.

- Sustainable Innovation: Advancing lightweight aluminium solutions and energy-efficient technologies for next-generation mobility.

Recent financial performance of UNO Minda Ltd. for Q4 FY26

| Metric | Q4 FY25 | Q3 FY26 | Q4 FY26 | QoQ Growth (%) | YoY Growth (%) |

| Sales (₹ Cr.) | 4528.32 | 5018.06 | 5336.41 | 6.34% | 17.85% |

| EBITDA (₹ Cr.) | 526.71 | 553.52 | 602.83 | 8.91% | 14.45% |

| EBITDA Margin (%) | 11.63% | 11.03% | 11.30% | 27 bps | -33 bps |

| PAT (₹ Cr.) | 234.57 | 226.48 | 287.52 | 26.95% | 22.57% |

| PAT Margin (%) | 5.18% | 4.51% | 5.39% | 88 bps | 21 bps |

| Adjusted EPS (₹) | 4.64 | 4.79 | 5.64 | 17.75% | 21.55% |

UNO Minda Ltd. financial update (Q4 FY26)

- Strong Revenue Growth: Q4 FY26 revenue rose 17.85% YoY and 6.34% QoQ to ₹5,336 crore, driven by higher content per vehicle and healthy OEM demand.

- Healthy Operating Performance: EBITDA increased to ₹603 crore, up 14.45% YoY and 8.91% QoQ, supported by premium products and localisation.

- Stable Margins: EBITDA margin stood at 11.30% (+27 bps QoQ), reflecting operational efficiency despite commodity cost pressures.

- Robust Profit Growth: PAT grew 21.80% YoY and 17.33% QoQ to ₹352 crore, highlighting strong earnings momentum.

- Higher EPS: EPS improved to ₹5.64 from ₹4.79 in the previous quarter, driven by higher profitability.

Business highlights

- Higher Content per Vehicle: Expanding high-value products such as alloy wheels, LED lighting, and ADAS solutions.

- EV Growth: Strengthening its EV portfolio through powertrain solutions, traction motors, and charging technologies.

- OEM & Aftermarket Strength: Leveraging strong OEM relationships and a wide aftermarket network to drive market share.

- Premium Product Mix: Scaling digital instrument clusters, smart switches, and sunroof systems to improve margins.

- Capacity Expansion: Investing in new manufacturing facilities to support long-term growth and operational efficiency.

Outlook

- Sustained Growth: Focused on long-term revenue growth, supported by rising EV adoption and expanding product offerings.

- Margin Improvement: Enhancing profitability through localisation, operational efficiencies, and better product mix.

- Premiumisation: Increasing exposure to connected, autonomous, and intelligent mobility solutions.

- Global Expansion: Strengthening its international presence through joint ventures, technology partnerships, and specialised products.

- Strong Order Pipeline: Healthy OEM order book and ongoing capacity expansion provide visibility for sustained long-term growth.

Recent Updates on UNO Minda Ltd.

- Portfolio Premiumisation: Expanding high-margin products including intelligent lighting, IVI systems, and advanced safety solutions.

- EV Expansion: Establishing a ₹550 crore facility in Chhatrapati Sambhaji Nagar for EV powertrains and hybrid transmission systems.

- Capacity Expansion: Investing ₹1,750 crore in FY27 to expand manufacturing across Bawal, Hosur, and Khed.

- Localisation: Increasing domestic manufacturing to reduce import dependence and improve cost efficiency.

- Operational Efficiency: Strengthening manufacturing capabilities to support rising OEM demand and long-term growth.

Company valuation insights – UNO Minda Ltd.

UNO Minda is currently trading at a TTM P/E of 51.11x, above the industry average of 37.21x, reflecting the market’s confidence in its long-term growth prospects and technology-led business model. The stock has delivered a 2.1% return over the last one year, outperforming the Nifty 50, which declined 4.4% during the same period.

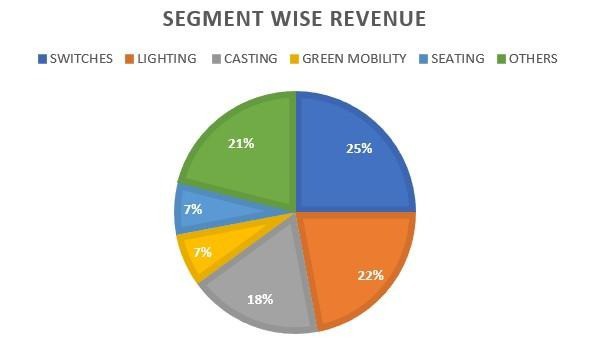

The investment case for UNO Minda is supported by its leadership in the domestic auto ancillary industry, a diversified product portfolio, and a consistent ability to increase content per vehicle through premiumisation and technology-led offerings. The company continues to gain market share across key segments including switches, lighting, alloy wheels, seating, and sensors, while expanding into high-growth areas such as EV powertrains, infotainment, sunroofs, and advanced automotive electronics. Its strong OEM relationships, aggressive capacity expansion, strategic acquisitions, and technology partnerships provide significant long-term growth visibility. With seven of its twelve ongoing projects expected to be commissioned in FY27, robust order wins across lighting, infotainment, displays and EV systems, and a rapidly expanding green mobility business, UNO Minda is well positioned to outpace the underlying automotive industry over the coming years. While near-term margins may remain under pressure from raw material and labour cost inflation, easing commodity prices and scale benefits are expected to support profitability over the medium term.

From a valuation perspective, we value the company at 40x FY28E EPS of ₹35, arriving at a 12-month target price of ₹1,400, implying an upside potential of 24% from the current market price. While the stock continues to trade at a premium to the industry, we believe the valuation is justified by its market leadership, strong execution capabilities, diversified product portfolio, and favourable positioning in the electric vehicle and premium automotive segments. For the near term, we maintain a 3-month technical target of ₹1,195, representing an upside potential of 6%, supported by healthy order visibility, continued capacity expansion, and improving long-term growth prospects.

Major risk factors affecting UNO Minda Ltd.

- Raw Material Risk: Fluctuations in commodity prices and supply chain disruptions could pressure margins and profitability.

- Competitive Pressure: Intense competition and OEM pricing pressure may limit margin expansion.

- Auto Industry Cyclicality: Demand remains sensitive to automotive industry cycles, inflation, and macroeconomic slowdowns.

- Technology Transition: Rapid EV adoption and evolving technologies require sustained R&D and capital investments.

- Execution Risk: Delays in capacity expansion or new project execution could impact growth and returns.

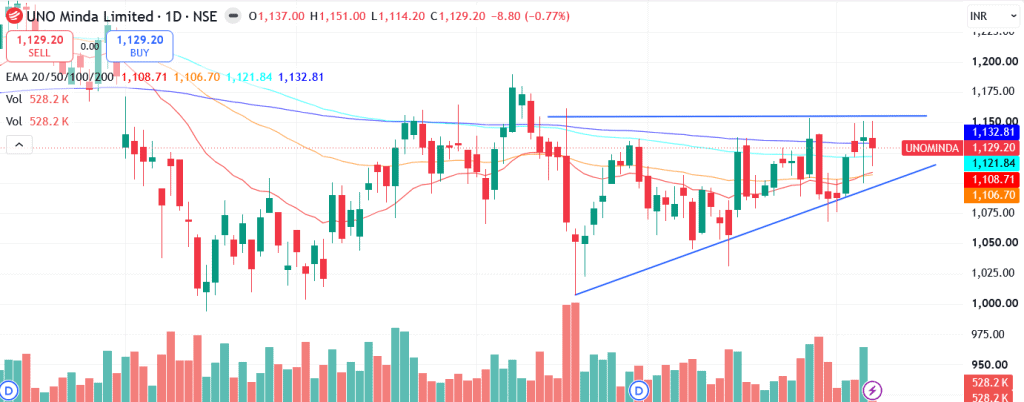

Technical analysis of UNO Minda Ltd.

UNO Minda is currently consolidating within an ascending triangle pattern, with the price trading close to the horizontal resistance level. The stock continues to trade above its 20-day, 50-day, 100-day and 200-day EMAs, indicating that the broader long-term trend remains positive despite the ongoing consolidation. A decisive breakout above ₹1,195 could act as the next trigger for momentum-led buying and pave the way towards ₹1,400, in line with our 12-month fundamental target.

Momentum indicators continue to support a constructive outlook. The MACD at 7.21 remains positive and is trading above its signal line, indicating strengthening bullish momentum and continued buying interest. The RSI at 55.21 reflects healthy buying interest while leaving sufficient room for further upside. Additionally, the Relative RSI over the 21-day and 55-day periods stands at 0.01, indicating slight outperformance against the broader benchmark and reinforcing the stock’s relative strength.

Trend strength remains subdued, with the ADX at 9.64 indicating a range-bound market and the absence of a strong directional trend. However, a sustained breakout above the horizontal resistance at ₹1,195 could significantly strengthen the trend, improve momentum, and attract fresh buying interest. On the downside, ₹1,050 remains a key support level and serves as an important stop-loss level for the bullish view.

- RSI: 55.21 (Good buying interest)

- ADX: 9.64 (Weak trend; breakout awaited)

- MACD: 7.21 (Positive; above signal)

- Resistance: ₹1,195

- Support: ₹1,050

UNO Minda Ltd. stock recommendation

Current Stance: Buy, with a 3-month target price of ₹1,195 (6% upside) and a 12-month target price of ₹1,400 (24% upside), based on a valuation of 40x FY28E EPS of ₹35.

Why buy now?

Strong market share gains across switches, lighting, alloy wheels, seating, and sensors, supported by increasing content per vehicle and a diversified product portfolio.

Well positioned to benefit from rising EV penetration through investments in EV powertrains, traction systems, infotainment, ADAS, and advanced automotive electronics.

Robust order wins across lighting, infotainment, displays, sunroofs, and EV systems, along with a healthy project pipeline, provide strong long-term revenue visibility.

Aggressive capacity expansion, strategic technology partnerships, and localisation initiatives are expected to support sustainable revenue growth and improve operating leverage over the medium term.

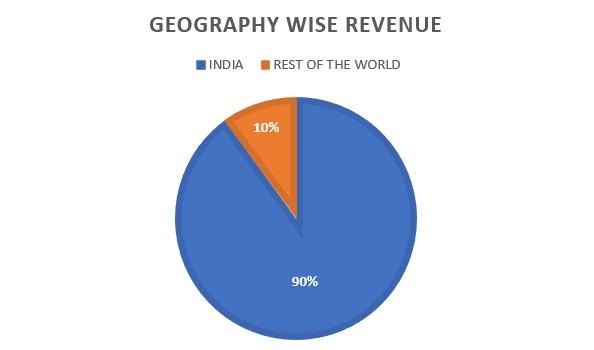

Strong OEM relationships, expanding exports, and a growing green mobility business position the company to deliver sustainable earnings growth over the long term.

Portfolio fit

UNO Minda provides exposure to India's automotive premiumisation and electric mobility themes through its leadership in automotive electronics, lighting, switches, alloy wheels, seating, and EV powertrain solutions. Backed by strong OEM relationships, a diversified product portfolio, expanding manufacturing capacity, technology partnerships, and a healthy order pipeline, the company is well positioned to benefit from rising vehicle content, increasing EV adoption, and long-term growth in the domestic and global automotive industry.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebUNO Minda Ltd.: Budget 2026-27 opportunities

- EV Push: Budget support for electric mobility and the PLI scheme strengthens long-term demand for UNO Minda’s EV components and powertrain solutions.

- Infrastructure Boost: Higher public capex on roads and logistics is expected to improve supply chain efficiency and support OEM production growth.

- Premiumisation Tailwinds: Rising focus on safer, connected, and premium vehicles will drive demand for ADAS, lighting, and automotive electronics.

- Localisation Benefits: Policy support for domestic battery and component manufacturing is expected to reduce import dependence and improve margins.

- Technology & R&D: Government support for electronics and semiconductor manufacturing aligns with UNO Minda’s focus on advanced automotive technologies.

Final Thoughts

UNO Minda Ltd. is well positioned to benefit from India’s long-term automotive premiumisation and electric mobility transition. With leadership across automotive switches, lighting, alloy wheels, and a rapidly expanding portfolio of EV components, the company continues to strengthen its market position through deep OEM relationships, technology partnerships, and a growing manufacturing footprint. Its focus on localisation, premium products, and capacity expansion supports sustainable long-term growth.

For long-term investors seeking exposure to India’s evolving automotive landscape, UNO Minda offers a compelling investment opportunity. Strong Q4 FY26 performance, a healthy order pipeline, aggressive capacity expansion, and increasing exposure to high-value automotive electronics and EV systems provide a solid foundation for sustainable earnings growth and long-term shareholder value creation.